0. 更多的 Rollup,更多的链

在 Rollup 的叙事越来越吸引目光,同时整个行业对 App-chain 性能、主权、部署的要求越来越高的过程中,StarkEx 的 App-rollup 服务、 Celestia 的可复用 Layer1 安全层、与其他高性能 DA 方案成为了搭建 App-chain 中的主流选择。

过去 App-chain = App as an L1: 之前,一个应用要自己做一条链,需要耗费很大的开发成本,如果是 PoS 机制,那么还得有额外的资本支出用于启动初始的节点。虽然有各种 SDK 和共识引擎的存在,做一条链依旧是一个非常麻烦的事情。

现在与未来 App-chain = App as an L1 + App as a Rollup + App as a Validium......:光是基于以太坊的 Layer2 就有 25 个,其中包括了一半应用链(或者叫 App-rollup, 比如以前的 dYdX)和通用 Layer2 Rollup(比如 Arbitrum),在 Celestia 等项目的成熟过程中, 我认为未来会有好几倍的新 Rollup 被构建出来。

除此之外,Cosmos 上的 App-L1,Avalanche 上的 Subnet 也会层出不穷。

无论是现有的应用协议转变成 App-chain(类似 Uniswap 可以直接变成 Unichain),还是应用直接以 App-chain 的形式启动(dYdX 以 App-rollup 启动,转变成 App-L1),最终都意味着未来一两年内可能会有几十个新的链(L1,App-chain,App-rollup,Subnet)。

1. 应用链 > 链上应用

最近,Dan Elitzer 以 Uniswap 为例,分析了 Uniswap 为什么一定会转变成一条单独的应用链。

Uniswap 协议收取的七日平均费用仅次于以太坊主网,是 BNB Chain、Aave、Bitcoin、GMX 的总和。

作为这么一个拥有稳定收益、运行良好、人人使用的 AMM 协议,Uniswap 为什么可能会从链上 Protocol 变成 App-chain 呢?

对于 Uniswap 来说主要有四个好处:

a) 代币价值捕获

UNI 代币本质上是个 Meme Coin,目前只能用于治理。这对 UNI 持有者来说,极大程度上 UNI 的价值无法直接捕获 Uniswap 协议和生态的增长和收益。

根本原因我认为主要还是监管的问题,由于产品本身的功能比较敏感,为了合规,Uniswap 的组织架构也比较特殊。

Uniswap V2 和 V3 都有 Protocol Fee 的概念,但现在这个 Fee Switch 没有被通过治理方式来打开。如果打开,那么直观来说,一年可以直接给 UNI 持有者带来几亿美元的收益(不考虑对 LP 收益和流动性的副作用),这对 UNI 代币的价值来说是一个巨大的加成。

同时 Uniswap 如果变成一条 PoS 的链,那么 UNI 代币可以作为质押代币与 Gas 代币,对 UNI 的价值捕获可以起非常积极的作用。

b) 协议经济机制

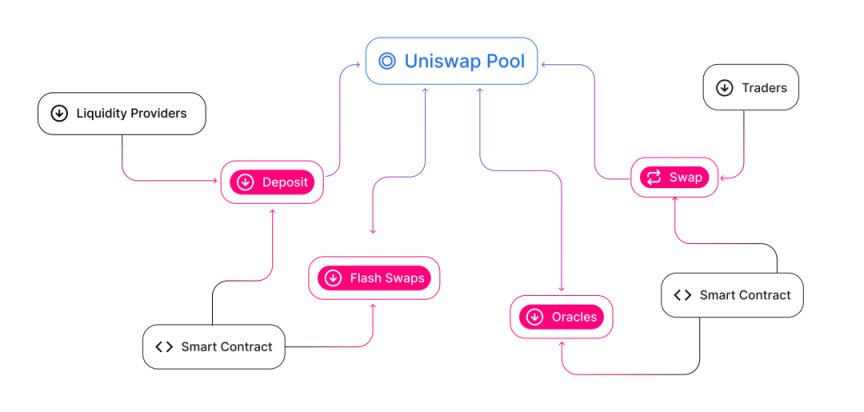

对于一个 Uniswap Pool 来说,最直观的两个参与者就是用户和 LP,但是对于整个协议的使用来说,参与者还包括网络节点以及 MEV Bots。

对于一个用户来说,进行一笔 Swap 需要很多方面透明与不透明的手续费:

Swap Fee:付给 Liquidity Provider ~0.171%;

Gas Fee:付给以太坊网络节点 ~0.235%;

MEV Tax:付给 MEV Bots 与以太坊网络节点(上图中 50% 以上的交易量都是 MEV Bot,他们偷偷搜刮用户的收益)~0.254%;

这些费用加在一起与中心化交易所对比,是很高的。

对于这三个 Fee 来说,Uniswap 目前其实是没有办法直接调控的。

但是如果 Uniswap 转变成 App-chain,那么就可以直接对 Gas Fee 与 MEV Tax 进行优化:

Gas Fee:付给 UNI 网络节点 < 0.235%;

MEV Tax:付给 MEV Bots 与 UNI 网络节点,同时可以通过新的机制来减少 MEV Tax 总和 < 0.254%;

这样之后,Uniswap 可以掌握对手续费和协议经济机制的主动权,通过治理等手段来对经济机制进行主动调控。

c) 交易体验

如果作为一条独立的 App-chain,那么 Uniswap 完全可以通过新的技术来进行协议的构建,而不需要考虑 EVM 兼容、通用合约部署等技术维度。所有的链上体验都直接赋能给协议的功能与协议周边生态的构建。

对于用户来说,可以体验到:

更高的 TPS:链可以专门对交易等操作进行优化;

更低的手续费:更低的 MEV Tax + 更低甚至像未来的 dYdX 一样为 0 的 Gas Fee;

更好的整体系统:生态会更加垂直地被构建, 一切都为了链与 Uniswap 本身;

d) 应用主权

就像 dYdX 从 StarkEx 出逃一样,Uniswap 如果变成一条 App-chain,那么就可以聚集以上的优点,对自己的代币、整个协议的功能与升级、整个网络与协议的治理、整个生态的构建与基础设施掌握更多的主动权。

e) App-Rollup 的附加特性

如果 Uniswap 变成一个基于以太坊的 App-rollup,那么就有更多的优点了,比如性能可以更大程度地提高,整个链的构建更加快捷与轻量级,且也不会与以太坊的生态离得太远。

但是对以上其他几个优点可能有削弱,比如还是需要把大部分的价值(占 L2 总 Cost 的 ~60%)都作为 DA Fee 返还给 Layer1,Gas Fee 的支出没有办法更加显著地减少,如果单 Sequencer 的情况下,那么就意味着大部分的 MEV Tax 都被它捕捉了。

2. 应用链的缺点

尽管应用链形态这么多优点,但是相比链上应用形态也有几个小缺点,也可以引出了我们下一节中想要讨论的互通性问题:

a) 共识与生态

一个链必须要有 Social Consensus。而目前的状况下,一个应用如果横空出世,直接以链的形式上线,很难有共识,因此非常多的应用才以协议或者 Rollup 的形式登陆到以太坊网络上,借助以太坊已有的安全性和社会共识。

以 Uniswap 为例,作为 Vitalik 亲自取名的应用,它与以太坊绑定地非常深,如果从以太坊主网内 「逃离」,那么必然受到很多以太坊方面与用户的阻力。

同时,Uniswap 最大的价值是在一个全球性的无需许可的最大的去中心化网络 ( 以太坊 ) 无需许可地发行资产(ERC-20),如果它变成是在自己的链上发行资产的话,吸引力会稍微小一些。相比之下,dYdX 这种专用的 Trading Platform 做应用链的意义更大一些。

b) 互通性

回到我们一开始所说的观点,之后会有几十条新的 App-L1,App-rollup,App-subnet。如果都变成链,形成自己的网络,那么和 Web2 的网络的区别就更小了......

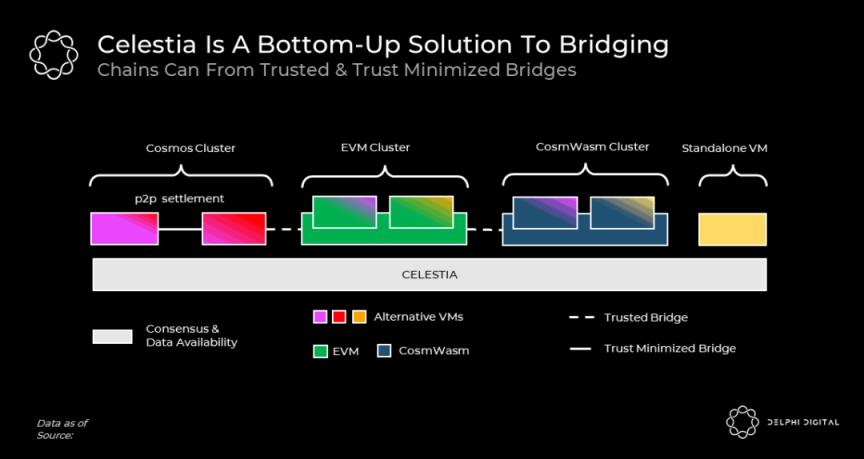

同时我认为这些 App-chain 中的 App-rollup 很多都会变成 Sovereign Rollup。那么它们就没有了以同一个 Layer1 底层搭建自带的 Trust-minimized 桥梁,从而以其作为互通层。

它们需要通过 Cevmos 等架构来通过 Trusted Bridge 与其他 Cluster 或者带 IBC 网络实现互通,架构上没那么简洁,同时概念也比较新。

这个事情我认为确实看上去非常好,但是真正工程实现上来说会非常麻烦。本身以太坊上的 Secured Rollup 就只需要构建自带的 L1- L2 Bridge 就可以,但是现在却需要 Evmos Settlement Layer 与其他网络(或者几个 Evmos 之间互相)构建桥梁。

3. 应用链与多链时代的互通性解决方案

互通性问题的例子,以 Uniswap 为例,极端情况下,如果它的主体变成链,大家要获取最佳的报价可能得在 Swap 的时候先跨链到它上面再 Swap 再跨回来。

对于应用链 + 多链时代的互通性的解决方案,我想到的最有效果几个方案:

a) 复制粘贴

1. 每个链上都主动 Fork 重点协议

也就是延续现在 Uniswap 所采用的方案,在每个链上依旧部署一个新的 Uniswap 协议。自己的 App-chain 则作为一个专用于交易的 Add-on,这其实也是类似 USDT、USDC 等资产的做法。

这个做法其实可以说是没解决问题,没解决互通性,只是把自己克隆了好几份,每一个协议都拥有割裂的流动性和交易活动,它们只是都以 Uniswap 的名字来运行。

然而,这个方案其实我是比较赞同的,并不反对。因为 Web2 系统中流动性也是一样分散的,或者说麦当劳也是在各个城市 Fork(虽然它肯定没必要做自己的「App-chain」)。

b) 创建链接

1. 每个链都接入 IBC

每个应用链(和链)都接入 IBC 是一个非常简单粗暴的方案,可以直接地解决互通性问题。

这个方案的缺点就是:

现有的链不一定能直接连(比如以太坊要连接 IBC 的话就需要 ZK),Cosmos 链性能不一定够(所以 App-rollup);

用户体验实际上还不如前一个方案(虽然 IBC 很快, 但是来来去去还是要十几秒, 所以两种方法可能需要结合);

2. 每个链上都有 Trust-minimized Bridge

我们直接忽略并非 Trust-minimized Bridge 的互通方案,要做到互通且安全,那么就需要 Light Client Bridge(本质上原理和 IBC 一致),或者 L3 之间的 Trustless Bridge。

这个方案的难点主要是各种验证 (Validator、Signatures) 的开销太大,没法链上 (EVM) 进行。但是验证 ZKP 的开销更小,因此最近有很多家在做 ZK Light Client。

对这个方向我非常认同,但是实现难度比上一个还要大,是很长久的解决方案。

4. 总结

链上应用转变为应用链绝对是大势所趋,能带来更好的主权、代币价值捕获、链内的体验提升。

然而,几十条新增的链会创造流动性割裂和互通性问题,要想解决这个问题,要么通过 Fork 基础设施到不同链上,要么接入可信互通协议。