Author: David, Shencha TechFlow

When Silicon Valley VCs are finally willing to let ordinary people join the table, it usually means one thing.

The game is almost over.

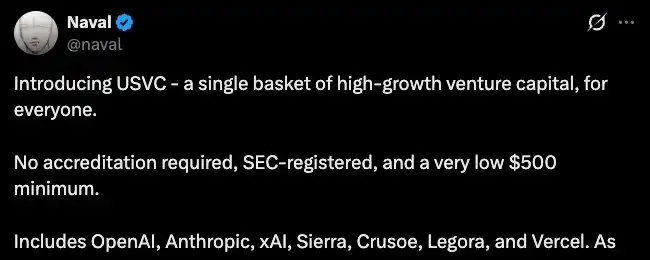

Yesterday, AngelList launched a fund product called USVC. AngelList is Silicon Valley's largest venture capital infrastructure platform. According to its official data, it manages over $125 billion in assets and has served more than 25,000 funds.

It has now opened a door to all US investors: a minimum investment of $500, no accredited investor certification required, directly allowing holders to own shares in seven AI companies, including OpenAI, Anthropic, and xAI.

Promoting this product is Naval, also a co-founder of AngelList. His book "The Almanack of Naval Ravikant" has made him one of the few figures in Silicon Valley with both a strong investment track record and significant public influence.

He posted a long thread on X promoting USVC, the gist being that early-stage tech investment is the "adventure capital" of our era, and ordinary people have always been locked out. By the time some great AI companies IPO, their growth is already over. USVC is here to open that door.

Within hours of the tweet, comments emerged asking an uncomfortable question that soured the mood:

These tech companies have been pushed to sky-high valuations, all the explosive growth happened in the private market. Now inviting retail investors to join, what's the difference from looking for exit liquidity?

USVC holds shares in seven companies, with the heaviest weighting in xAI. According to a Decrypt report, as of the end of March, about 44% of USVC's capital had been invested in these seven companies.

However, none of these companies are public. How did they get the shares?

According to the prospectus, USVC has three ways to acquire its targets: investing in emerging fund managers, participating in company growth-round financing, and purchasing secondary shares through AngelList's network.

The first two are straightforward. The third is the key.

Secondary shares mean that the company is not issuing new shares to sell to you; someone who already holds shares is transferring their portion to you. Who is transferring? Early angel investors, VC funds, early employees.

These people might have gotten on board when the company was valued at tens of millions of dollars. Now the company is worth tens or even hundreds of billions. They want to turn paper gains into real money before the IPO. But the private market isn't like a stock exchange; there's no ready queue of buyers waiting to take the other side.

USVC solves this problem perfectly. It raises funds from retail investors and uses that money to buy shares from insiders who want to exit.

AngelList does have a natural advantage for this. According to its website, there are over 4,500 active fund managers on the platform operating more than 25,000 funds, invested in over 13,000 startups.

This network is full of people and shares wanting to be sold, with AngelList sitting right in the middle. This is also the "exclusive access" USVC repeatedly emphasizes.

The access is indeed exclusive, but the direction of the trade doesn't seem to favor retail.

In this trade, the sellers are those who got in when the company was valued at tens of millions. The buyers are those getting in when it's valued at hundreds of billions. The sellers lock in returns of tens or even hundreds of times. The buyers are betting that these already fully-priced companies can still go higher.

Simultaneously, the terms retail investors are getting also say something.

According to the USVC prospectus, the fund is not listed on any exchange, does not anticipate a secondary trading market, may repurchase up to 5% of its net asset value per quarter (solely at the board's discretion, with no guarantees), and has an estimated total annual expense ratio of 3.61%—far higher than the prominently displayed 1% management fee, with the difference coming from layered fees of the underlying funds.

No ability to sell, exit dependent on queuing, and nearly 4% of principal eaten by fees annually. For a product with a $500 minimum investment aimed at ordinary people, this price isn't cheap.

So, the complete picture is likely this.

On one side are the insiders wanting to exit, getting liquidity, locking in profits. On the other side are the retail investors just entering, getting a share that can't be traded, has an exit reliant on queuing, and has an effective fee rate much higher than advertised. The direction of the funds, from start to finish, is only one way: from later arrivals to early arrivals.

The Equity Version of "Low Float, High FDV"

Breaking down the USVC model: insiders accumulate positions at low valuations. After asset prices are pushed high, a channel accessible to retail is packaged, allowing the funds of later arrivals to facilitate the exit of early arrivals.

The crypto industry ran a complete rehearsal of this logic between 2021 and 2024.

During those years, VC-backed token projects had a universal template: seed round valuation a few million, private round rising to tens of millions, and by the time the token listed on exchanges, the Fully Diluted Valuation (FDV) had skyrocketed to tens or even hundreds of billions. But only 2% to 5% of the total supply was in circulation, with the rest locked with VCs and the team, vesting on a schedule.

Low float, high FDV.

What USVC is doing is essentially almost identical to low float, high FDV. Insiders get in when the company is valued at tens of millions. After the company's valuation grows to hundreds of billions, they transfer their shares out through a product aimed at retail.

Naval's own trajectory is also interesting. Last October, he tweeted on X that "Bitcoin is insurance against fiat, Zcash is insurance against Bitcoin." This tweet caused ZEC to surge over 100% in a week. The community then dug up that, according to public reports, Naval had invested $715,000 in the development company behind Zcash as early as 2015 and had served on the Zcash Foundation's board.

The community's conclusion was simple: he was using his personal influence to shill his early investment. Naval did not respond to these质疑 (queries).

From Zcash to USVC, the model hasn't changed. A celebrity uses public credibility to open the demand side and uses a channel to direct that demand towards assets they have a position in.

Of course, in the case of USVC, there doesn't seem to be anything illegal.

USVC is a registered fund, the risk disclosures in the prospectus are ample, and the Zcash tweet didn't constitute investment advice.

But between legal and reasonable, there's always an ambiguous distance. A platform managing a trillion-dollar venture network, using the narrative of "letting ordinary people invest in the future" to raise retail funds, then using those funds to buy out insiders within its own network who want to exit...

Every single part of this is compliant. But all the parts put together easily trigger painful memories for retail investors.

And on the same day USVC launched, Robinhood also announced its fund spent $75 million to buy OpenAI shares, also open to ordinary investors. Two companies did the same thing in the same week: using their respective retail networks to build an exit channel for insiders in the private market.

Every time the financial industry suddenly starts caring about the investment rights of ordinary people, it's often not because the situation for ordinary people has improved, but because the exit channels for insiders have narrowed.

This was true in 2021 when the crypto industry opened its doors wide to retail, and it's true in 2026 when Silicon Valley opens its doors to retail. The timing of the door opening is never decided by those who want to enter.

For ordinary people, there's a simple way to judge if an investment opportunity is meant for you.

Look at the people who got in before you. Are they buying more or are they selling right now? If they are selling, and you are being invited to buy, then you need to think clearly about one question: are you bringing capital, or are you bringing liquidity?