麦肯锡最近发表了一份长达 77 页的综合报告,题为《在元宇宙中创造价值——虚拟世界的真实业务》。麦肯锡的7位合伙人被认为是该报告的作者,其中包括对13位资深“元宇宙专家”的访谈、麦肯锡技术委员会(McKinsey Technology Council) 60名成员的意见,以及对3400多名消费者的调查。

该报告的最终结论是,元宇宙是一个不容忽视的机会,对社会的影响很大,监管机构不得不采取行动。我认为这份报告对于任何支持元宇宙的人来说都是值得一读的。同时,该报告有77页,大多数人不会花时间去读它。以下是我提取出的8个亮点:

1. 元宇宙的定义将继续演变

虽然定义仍然是不固定的,但麦肯锡认为元宇宙是互联网的下一个迭代,它将让我们沉浸其中,而不仅仅是看到而已。

不管人们对元宇宙的确切定义是什么,它都有以下几个基本特征:

沉浸感

实时交互性

用户代理

引用扎克伯格去年11月的话:“元宇宙将成为移动互联网的接班人。我们将能够感受到真实感——就像我们就在那里,不管我们实际上相距多远。”

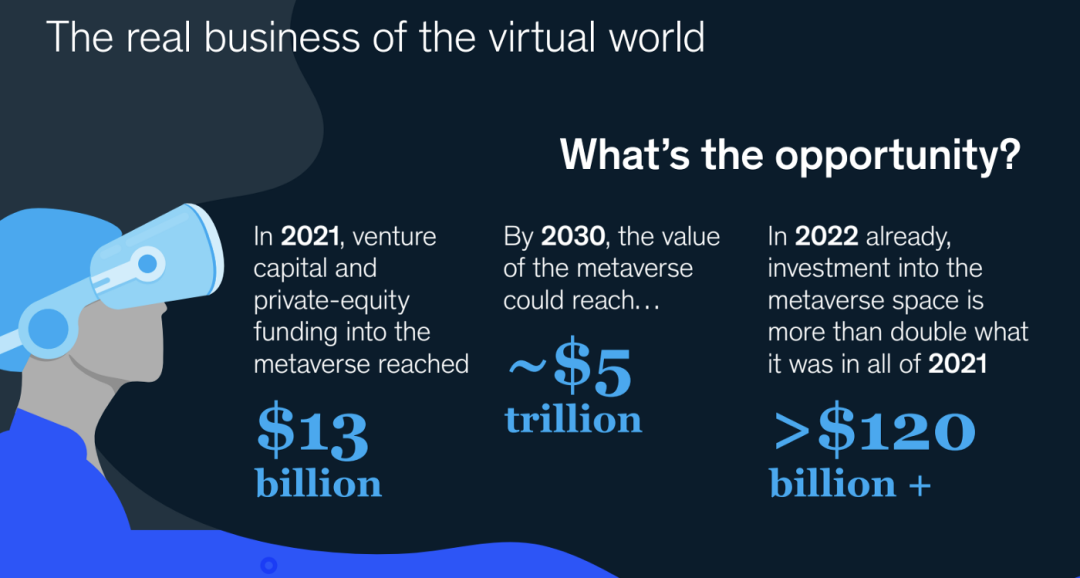

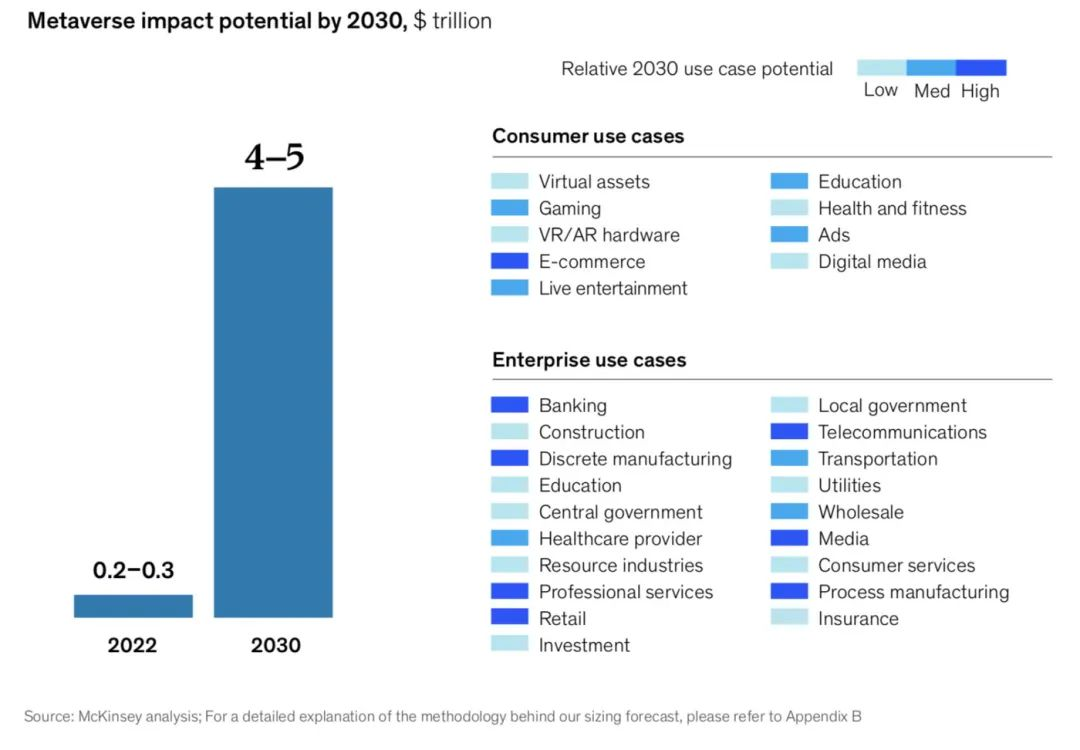

2. 到2030年,元宇宙的价值可能达到5万亿美元

虽然其他人认为这是一个更大的市场(例如,花旗公司认为2030年的元宇宙市场规模为8-13万亿美元),但麦肯锡估计2030年的元宇宙市场规模为4-5万亿美元:

麦肯锡认为,元宇宙代表着多个行业的最大增长机会,包括电子商务(2-2.6万亿美元)、网上学习(1440 - 2060亿美元)和广告市场(1080 - 1250亿美元)。

3. 实现元宇宙潜力所需的技术还不存在

该报告强调了跨多种技术所需的重大技术进步,包括计算基础设施、网络基础设施和设备,以实现元宇宙的潜力。

例如,今天的并发限制一定程度上阻碍了游戏平台上的玩家数量的增长。但是要实现元宇宙,需要有更多的用户能够同时在线。

在网络基础设施方面,高延迟“滞后”会给需要高帧/秒速率的元宇宙应用程序造成视频和/或音频缓慢的感觉。

最后,今天的元宇宙在很大程度上是需要通过带有平面屏幕的设备(即电视、个人电脑和智能手机)进行访问的。虽然麦肯锡预计平板显示器还将在未来五年继续占据主导地位,但元宇宙需要AR/VR和最终的扩展现实(XR)来实现越来越沉浸式的体验。然而,要实现深度沉浸,需要在 AR/VR 方面取得重大进展。而像隐形眼镜和脑机接口(比如Neuralink)这样的XR设备至少还需要十年的时间。

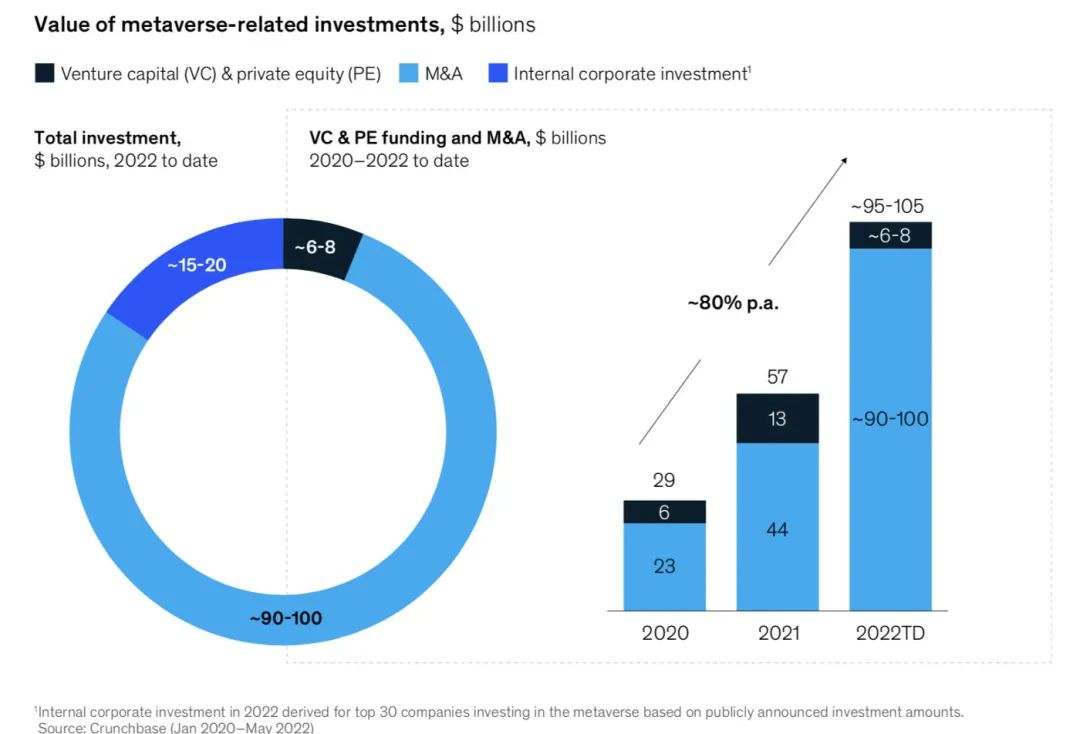

4. 非技术相关公司已经加入了科技公司和风投公司的行列,在元宇宙中进行大量投资

虽然Facebook仍是进军元宇宙领域的最知名的大型科技公司,但微软(Microsoft)、英伟达(Nvidia)、苹果(Apple)、索尼(Sony)和Alphabet等公司也在这个领域投入了大量资金。

包括安德森·霍洛维茨(Andreesen Horowitz)、Paradigm、Coatue和软银(Softbank)在内的风投公司已经向Open Sea、 Sandbox 、Yuga Labs/Bored Ape Yacht Club 等元宇宙项目投入了数十亿美元。

现在,科技之外的许多行业的公司都在组建团队,来实现他们的元宇宙计划。从迪士尼(Disney)这样的媒体公司,到巴黎世家(Balenciaga)这样的时尚品牌,越来越多的非科技品牌已经将元宇宙视为有待开发和需要发展的主要增长机会之一。

5. 公共部门活动也在元宇宙中进行

麦肯锡指出,迪拜虚拟资产监管局(Virtual Assets Regulatory Authority)今年早些时候在Sandbox上建立了元宇宙总部,成为第一个在元宇宙中开展业务的监管机构。

首尔市最近公布了一项为期五年的“元宇宙首尔基本计划”,其中包括虚拟首尔市政厅、广场和公务员中心,其目标是“提供公民自由参与和交流的机会”。

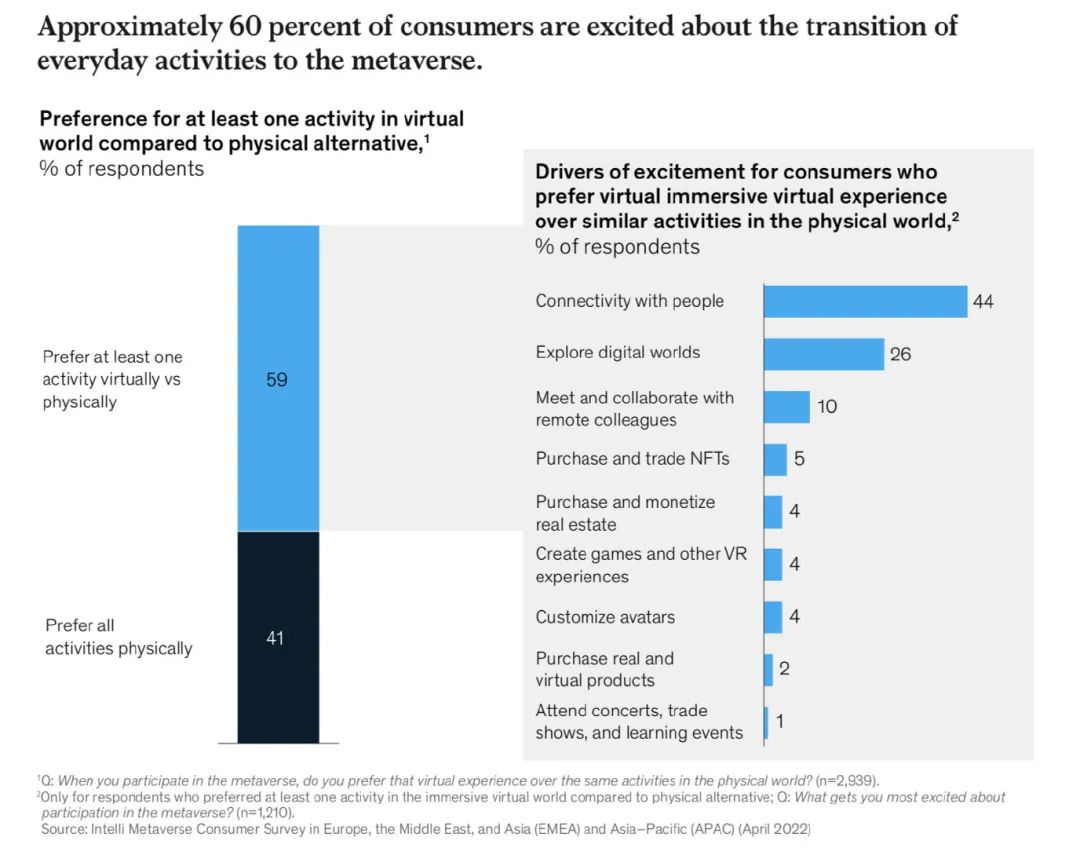

6. 消费者对把日常活动转向元宇宙的事情,感到越来越兴奋

当麦肯锡询问消费者在未来五年内希望在元宇宙做什么时,与家人和朋友的社交和沟通排名最高:

7. 关于元宇宙,人们对其有许多误解

最值得注意的是,元宇宙不会取代现实生活。相反,元宇宙将更深入地融入现实生活,使所有真实的东西都能进行数字化扩展。

报告中列出的其他观点包括多重元宇宙的概念,元宇宙是AR/VR,元宇宙是Web3,元宇宙只是为了游戏等,

8. 高管和政策制定者需要从今天开始采取行动

麦肯锡相信元宇宙是一个不可忽略的机会。元宇宙将改变一切,从企业与客户的互动方式到公司的运营方式。因此,高管们需要开始学习和尝试。高管需要玩Roblox、Fortnite、Minecraft。他们需要探索Sandbox 和 Decentraland。但如果高管们等上一两年才开始学习,开始检验假设,那可能就太晚了。

对政策制定者来说,关键议题的数量很多,而且还在增加。它们需要解决开放访问、竞争和知识产权问题,以及多样性、公平性、包容性、用户安全和数据隐私问题。麦肯锡认为,尽早开始制定详细的监管框架来治理元宇宙的漫长旅程,对政策制定者有利。

考虑到我们的商业和个人生活即将受到的巨大影响,麦肯锡建议每个人,从高管、政策制定者到消费者,尽可能多地探索和理解元宇宙、基础技术,以及其对我们的经济和更广泛的社会的影响。