Written by: Thejaswini M A

Compiled by: Luffy, Foresight News

Operating illegal private gambling in barbershops has been against the law for a hundred years. But once run by the state, it becomes a legal lottery. How can one monetize a product that is legally prohibited from direct sale? Capital always flows towards channels that exploit loopholes in the rules.

Last week, Robinhood CEO Vlad Tenev officially launched the company's public chain and stock tokens at a release event themed "The World is Flat." The theme sounds clever, but the so-called stock assets users buy are essentially "castles in the air."

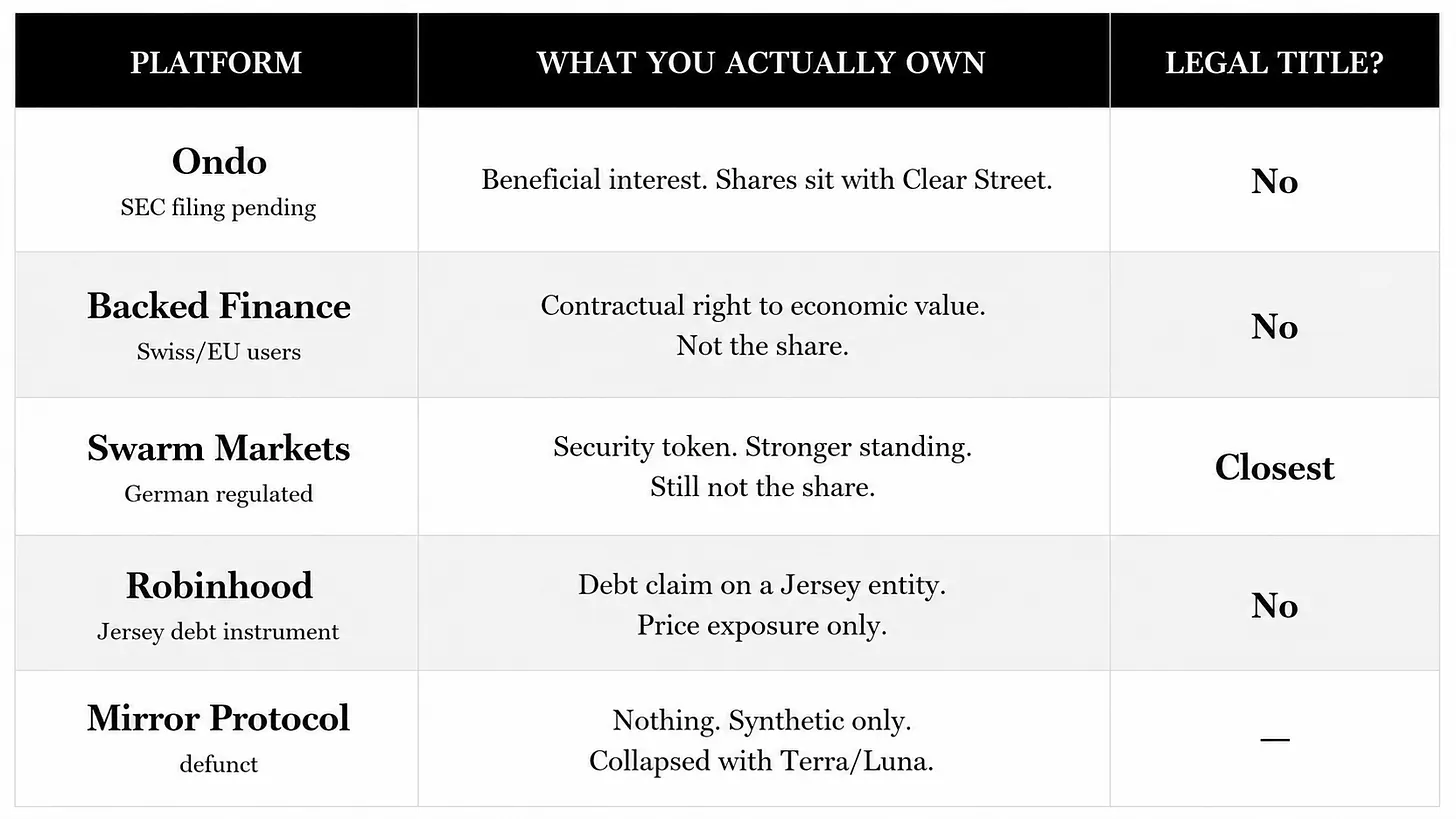

When you buy an Nvidia stock token, you can only track the price fluctuation of Nvidia stock, without enjoying any shareholder legal rights. Once Nvidia collapses operationally, you have no claim on the company's assets. The tokenization model inherently carries such risks. Ondo has already submitted relevant filings to the U.S. SEC, but related regulatory plans remain unresolved.

The truth about Robinhood's product is: what you are buying is not equity, but debt securities.

These debt securities are issued by Robinhood Assets (Jersey) Limited. Users are essentially lending money to this shell company located on the tax haven island in the English Channel. This shell company then pays you returns based on the rise and fall of the corresponding stock price.

Looking back to the June 2025 event in Cannes, Robinhood, to promote the product, distributed free private company stock tokens for OpenAI and SpaceX to European users to attract traffic. Equity in these companies is not publicly available, and ordinary investors have no normal channels to subscribe. After seeing tokens misusing its name, OpenAI publicly issued a risk warning, stating it never authorized the circulation of such assets; OpenAI co-founder Elon Musk directly called such tokens fakes. At that time, Robinhood CEO Tenev also personally admitted that such tokens are, strictly speaking, not equity; they only allow users to gain price exposure.

Since direct equity tokens are possible, why package them as debt and issue them through a Jersey Island shell company? The answer lies within the regulatory rules of the U.S. SEC. Equity represents ownership in a company, enjoying shareholder rights such as voting, dividends, and claims on assets in liquidation. Debt is an obligation the company owes you, where creditors do not possess ownership of the company.

Robinhood stock tokens are "equity-like debt instruments." Holders are not the legal shareholders of the listed company. Even if you buy an Nvidia token, Nvidia itself is completely unaware of your existence.

What you actually hold is a debt certificate issued by the Jersey shell company, which promises to settle returns with you based on, say, Apple's stock price. If Apple's stock price rises 20%, the company pays a corresponding 20% return. However, if this Jersey shell company goes bankrupt, you become merely an ordinary creditor, waiting in line for liquidation repayments. The real Apple stock held by the shell company might cover your claim, or it might be insufficient, ultimately resulting in a total loss of principal, all depending on the complex bankruptcy liquidation process.

If Apple itself declares bankruptcy, your situation becomes even more passive: you don't hold Apple stock; you only hold a debt instrument pegged to Apple's stock price. The underlying asset's value drops to zero, rendering the debt worthless.

The root of Robinhood's effort to design this complex structure can be traced back to the company's most devastating crisis: the January 2021 GameStop short squeeze. A large number of retail investors rushed to buy the stock, but Robinhood directly shut down the buy button. The U.S. stock market's T+2 settlement mechanism caused the platform to face a margin shortfall of tens of billions of dollars, unable to meet clearing guarantee requirements, forcing an emergency trading restriction. Many retail investors felt abandoned by the platform. Congress specifically subpoenaed Tenev for questioning, and the brand's trust has never fully recovered since.

Five years later, this token product is seen as Tenev's solution: blockchain enables second-level settlement, completely abolishing the T+2 settlement cycle, no longer generating huge margin call demands, and theoretically never needing to shut down the buy button again. Since early 2026, he has continuously promoted this logic externally. Robinhood also submitted a 42-page token asset regulatory proposal to the SEC back in 2025, advocating for dedicated industry rules.

In January 2026, three divisions of the SEC jointly issued guidance on the classification of token securities, categorizing such products into two types. First, Native Equity Tokens: Companies directly tokenize their own stock on-chain, and holders possess full shareholder rights. Second, Linked Securities: Third parties issue tokens that simulate stock prices, without carrying any shareholder legal rights or responsibilities. The SEC explicitly stated that such products can be packaged as structured notes (debt products), where holders bear counterparty risks that ordinary shareholders do not face. If the issuer goes bankrupt, all losses are borne by the investors themselves.

In March of the same year, the SEC and the U.S. Commodity Futures Trading Commission (CFTC) jointly announced maintaining the classification and regulatory framework issued in January unchanged. Robinhood deliberately chose to issue the second type—Linked Securities—from Jersey Island, precisely to sidestep regulatory red lines.

The regulatory document also mentioned a similar product: security-based swap contracts, which are essentially over-the-counter bets on stock prices. However, federal regulations strictly limit participation to qualified institutions and high-net-worth professional investors; ordinary retail investors cannot purchase them.

Debt-based structured notes have no investor threshold restrictions, allowing even a 19-year-old with only $10 to participate. Robinhood ultimately chose this packaging model with the broadest audience and the least regulatory resistance.

At the same time, U.S. domestic users are completely excluded. The stock tokens are open to over 120 countries worldwide, with the United States, Canada, the United Kingdom, Switzerland, and the UAE not within the service scope.

The European market adopts a different compliance structure. The classic stock tokens launched in Cannes in 2025 comply with EU MiFID II regulations, issued by Robinhood's European entity, with tokens backed 1:1 by real stocks held in custody. The number of underlying assets has now expanded from 200 to over 2,000, with entry possible with as little as 1 Euro. This means Robinhood can indeed offer compliant real-stock tokens in Europe; the Jersey debt structure is an active choice.

This model heavily relies on the transparent pricing logic of public markets. Only publicly traded companies like U.S. stocks with real-time trading have fair market prices. For private, unlisted companies like Anthropic and OpenAI, there is no publicly traded price. Token valuation can only rely on subjective institutional estimates, with no obligation for the companies to disclose externally, making risks entirely uncontrollable.

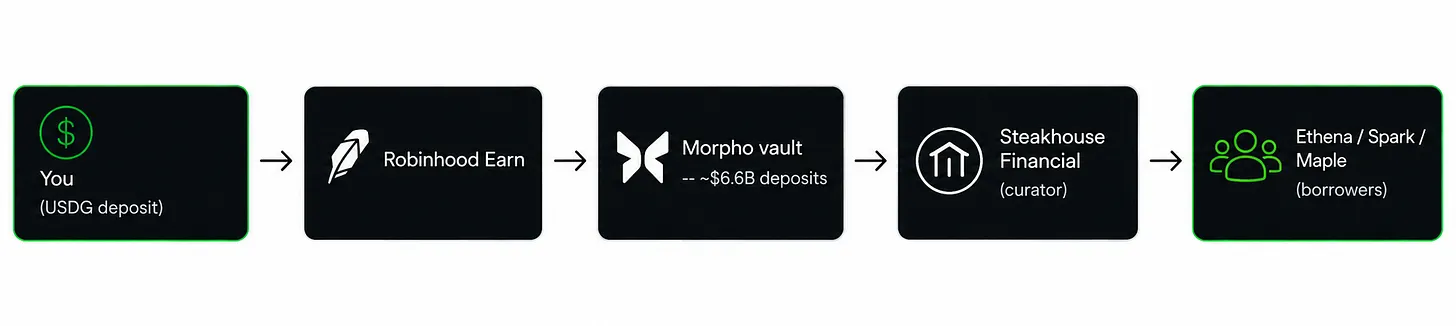

Additionally, Robinhood's separate Robinhood Earn product independently offers a 7% annualized yield, available only to U.S. users. Users lend the stablecoin USDG, with funds first flowing into a Morpho lending vault operated by Steakhouse Financial, then distributed to various DeFi protocols like Ethena and Maple. The Morpho vault deposit size is about $6.6 billion, with yields floating based on market lending demand.

Robinhood has insured smart contract theft with London's Lloyd's, but the policy does not cover the risk of yield dropping to zero. When market lending demand shrinks, yields will decline alongside money market fund rates. User funds pass through multiple intermediaries: Robinhood, Steakhouse, Morpho. Once USDG depegs or a large-scale borrower default occurs, insurance cannot cover it at all. These are common causes of principal loss in such products.

Tokens are stored on-chain and support staking and lending, seemingly convenient. However, smart contracts cannot directly read stock prices and must rely on oracles for price feeds. If an oracle feeds false prices, the contract will incorrectly liquidate user assets or issue loans improperly. From 2024 to 2025, oracle price manipulation was a core method for large DeFi thefts, causing losses of tens of millions of dollars for numerous projects.

Within the entire product ecosystem, the only orthodox, full-voting-right equity is Robinhood's own stock, HOOD, traded on traditional Nasdaq channels. The platform keeps the real equity for itself.

The underlying business logic is clear. Robinhood earns a spread on every token transaction; the public chain belongs to itself. The overseas new business can continuously beautify the financial reports of the listed company, all without being constrained by U.S. domestic regulations. A token business without actual equity has lower regulatory costs and cleaner profits.

The Robinhood Chain is built on the Arbitrum Orbit network, using ETH to pay Gas fees. It has not issued a native platform token, avoiding token speculation risks, and the platform does not need to profit from a native token. The company's long-term plan is to build a one-stop settlement channel, enabling 7x24 on-chain trading for stocks, ETFs, stablecoins, commodity perpetual contracts, and future private equity. Robinhood was originally just an order routing intermediary. If the plan materializes, it will combine the functions of an exchange and a clearinghouse.

Objectively speaking, current regulatory rules are rapidly evolving. The new SEC Chairman Atkins has overturned the previous "sue first, regulate later" approach and is drafting an innovative regulatory sandbox exemption bill. The "CLARITY Act" has been submitted to the Senate for review since June. Once enacted, the regulatory gray area Robinhood currently occupies will continue to narrow.

This playbook is already familiar in the industry. Coinbase and Kraken expanded their businesses early in regulatory gaps, then strengthened compliance qualifications after regulations detailed and industry demand was validated. The current Jersey debt tokens are more like a transitional, semi-finished product for Robinhood.

Just two days before Robinhood's stock token launch, on July 2nd, Ondo launched compliant tokenized stocks on Ethereum, issued through an SEC-registered transfer agent. The tokens are fully backed by real stocks held in custody, with holders enjoying on-chain voting rights, covering over 250 companies. Coinbase simultaneously listed the product, allowing U.S. users to trade legally, with dividends distributed directly to user accounts.

Operating a fully compliant model in the U.S. costs more and is subject to regulatory constraints throughout. Robinhood already bears these compliance costs in Europe. Therefore, the Jersey Island debt structure is a choice by Robinhood. In the future, either regulations will force a product upgrade, or competitors will launch U.S.-compliant real-stock tokens to steal customers.

First capture the market, then wait for regulations to mature—this is Robinhood's strategy.