The upcoming Ethereum merge will switch the network consensus system into “proof of stake.” Here’s why miners are worried about it.

Ethereum Miners Made $18 Billion In 2021, More Than Bitcoin Miners

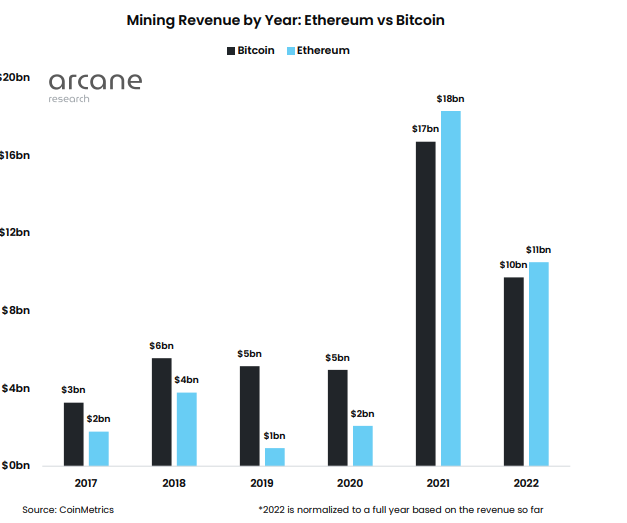

As per the latest weekly report from Arcane Research, ETH mining revenues totaled $18 billion in 2021, slightly more than Bitcoin miners’ $17 million earnings.

Even in the year 2022 so far, Ethereum miners have been leading the race in terms of revenues. Here is a chart that compares the mining revenues of the two largest cryptocurrencies in the market for the last few years:

As you can see in the above graph, the BTC mining revenues had been ahead of ETH’s until the year 2021, when the latter coin’s validator flew ahead.

With recent revenues being so high in the billions, Ethereum miners have invested a large amount of money into acquiring more graphics cards to improve their profits.

However, soon these revenues will instantly fade into nothing as the ETH transition to a proof-of-stake (PoS) mechanism is completed.

In the “proof-of-work” (PoW) consensus system, which the crypto currently utilizes, miners act as network validators and compete with each other by solving computing puzzles.

PoS, on the other hand, doesn’t involve any “miners.” Instead, here any investor can become a validator by locking in a specific amount of coins into the network “staking” contract, and they don’t require any substantial computing power either.

These validators, called the “stakers,” are randomly chosen to hash the next transaction into the chain. Though, stakers with larger amounts staked get better odds to be selected.

The advantage of PoS over PoW is that it massively reduces the amount of computing power involved in validating transactions. Because of this, it’s also a more environment-friendly mechanism.

The upcoming Ethereum merge will complete the switch to PoS, and that is very worrying for the miners as it means they will be turned obsolete.

There are hardly any options left for these miners to turn to as Bitcoin mining uses different chips than the GPUs ETH miners have and no other crypto is big enough to fill the revenue gap of ETH.

Something miners can try is to help other GPU-mineable coins to grow. One such potential crypto is Ethereum Classic, which saw a 155% uplift during the past month. However, as it is now, ETC’s mining revenues are just 3% of ETH’s.

If moving to another crypto doesn’t work out, their only choice left will be to dump their GPU stacks that they invested $15 billion on.

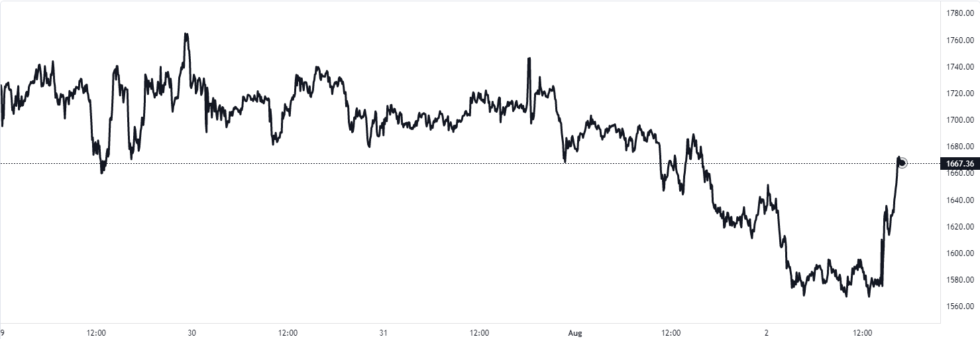

ETH Price

At the time of writing, Ethereum’s price floats around $1.6k, up 20% in the past week.