撰文:0xhhh

一、引言:信任的盲点

区块链是一场关于信任的革命,但它的信任是封闭的。

它相信数学,却不相信世界。

早期的区块链像一个逻辑主义者:它坚信推理,却拒绝感知。

比特币信任哈希,不信任人;以太坊信任代码,不信任输入。

于是,当一个合约想问出「ETH 的价格是多少?」时,它陷入了沉默。

这不是技术缺陷,而是哲学的边界。

区块链的确定性来自于与外部世界的切割。

信任的源头,是孤立。

但没有连接,就没有意义。

人类构建信任体系的历史,就是不断让「系统」重新看见「现实」的过程。

预言机(Oracle),便是这道裂缝里伸出的第一只手。

它既是连接,也是污染;

既是突破,也是危机的起点。

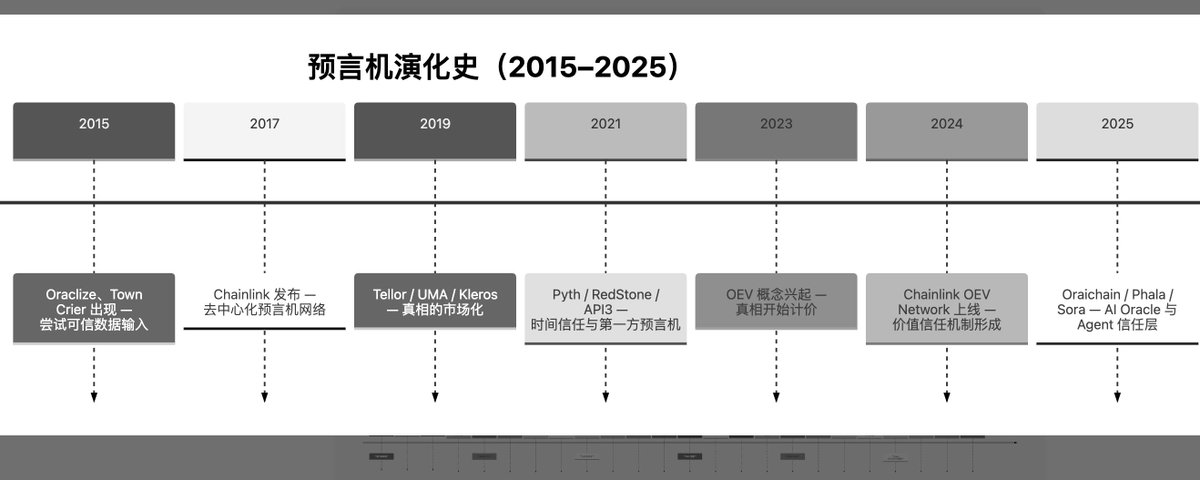

二、第一阶段:洞穴的裂缝(2015–2018)

背景:封闭智能的孤岛

2015 年,以太坊把「代码即法律」带入世界。

但法律需要证据,而区块链上没有「外部事实」。

一个「基于天气赔付」的合约,无法知道今天是否下雨;

一个「跟踪股价」的合成资产,无法看到 Nasdaq。

智能合约成了柏拉图洞穴中的囚徒,只能凝视链上影子。

区块链的纯净,也成了它的桎梏。

问题:如何「看见」而不被污染

如何让区块链看到外部世界,却不被它污染?

信任外部数据意味着引入主观性、中心化,而区块链的存在目的正是要消除这两者。

于是,「可信输入」成了去中心化信任体系的第一道悖论。

技术演进

-

Oraclize(Provable):通过 TLSNotary 证明数据确实来自特定源头。

-

Town Crier(Cornell):利用 Intel SGX 可信执行环境进行安全数据读取。

-

Chainlink(2017):提出去中心化预言机网络,节点抵押 LINK、聚合数据、形成加权共识。

信任的第一次呼吸

区块链让信任逻辑化;预言机让信任具象化。

机器第一次学会「相信」,而人类开始用算法定义真理。

三、第二阶段:真相的市场(2019–2021)

背景:DeFi 的信任饥荒

DeFi 的爆发让喂价成为系统生命线。

清算、衍生品、稳定币、合成资产,都依赖外部价格。

但价格操纵一次,就可能掀起连锁反应。

真相,变成可套利的资源。

技术演进

-

Tellor(TRB):以抵押与质疑机制让真相在博弈中产生。

-

UMA(Optimistic Oracle):默认信任,直到被质疑。

-

Kleros(PNK):去中心化陪审团裁决事实争议。

-

Band Protocol / DIA:引入 API 层折中方案,平衡速度与可信度。

信任的博弈时代

Tellor 让真相成为博弈均衡,

UMA 让真相成为默认状态,

Kleros 让真相成为社会契约。

信任不再是名单,而是博弈的结果。

真相第一次被「市场化」。

四、第三阶段:时间的战争(2021–2023)

背景:真相的时延危机

在高频交易和清算的时代,延迟就是风险。

当真相比谎言慢,系统将惩罚真相。

技术演进

-

Pyth Network(PYTH):由交易所直接签名报价,源头即节点。

-

RedStone(RED):按需拉取喂价,执行即验证。

-

API3:第一方预言机,数据源自己签名自己发布。

-

Band Protocol:在 Cosmos 上实现跨链数据层。

当时间成为真理的形状

信任从「正确」转向「及时」。

预言机成为「时间的仲裁者」。

延迟,成为新的信任维度。

🔹 信任开始有价格:OEV 的觉醒(2023–2024)

OEV(Oracle Extractable Value)

—— 真相与时间之间的套利差。

价格更新的瞬间不仅是信息事件,更是价值事件。

真相的传播顺序开始决定财富的分配。

问题不再是「真不真」,而是「谁因真相得利」。

技术与机制演化

-

Chainlink OEV Network(2024):创建 OEV 拍卖市场,让优先更新权可竞价。

-

Pyth / SEDA:通过时间戳签名与随机委员会抑制内部套利。

-

RedStone Pull 模式:天然消除时间差,不留套利窗口。

真相开始计价

OEV 让信任有了经济重量。

过去我们讨论「谁在说真话」,

现在要讨论「谁因真话获利」。

信任从事实验证扩展到价值治理。

五、第四阶段:智能与隐私的碰撞(2023–2025)

背景:AI 进入信任体系

AI 模型能判断市场、分析新闻,但它的「真伪」不可验证。

当机器开始判断真相,我们该如何判断机器?

技术演进

-

Oraichain(ORAI):可验证 AI 推理(Proof of Execution)。

-

Phala / iExec:用 TEE 可信硬件生成远程证明。

-

SEDA / Supra / Entangle:融合 AI 验证与跨链同步。

理智的验证

当我们要求机器证明自己的理智,

Oracle 从「验证世界」变成「验证智能」。

信任扩展到判断层。

六、第五阶段:Agent 时代的信任重建(2025 →)

背景:AI Agent 崛起

AI Agents 已具备经济行为能力。

它们签合约、谈合作、执行交易。

但算法没有道德,只有输入。

当智能体互相交易,谁保证它们看到的是同一个世界?

技术演进

-

Sora Oracle(SORA):AI Oracle + 支付协议 + 预测市场,形成认知自校体系。

-

Flux / OptionRoom:嵌入预测市场进行事实验证。

-

Orochi Network:构建机器身份体系,使判断可溯源。

信任的再造

当智能体成为社会主体,

人类从「信任承担者」变成「信任设计者」。

机器之间的信任,不是情感,而是协议。

Oracle 从数据接口,蜕变为文明结构。

七、尾声:从数据桥到智能信任层

十年演化,Oracle 的每次升级

都源自一次信任危机,也开拓了新的边界。

区块链让信任可计算;Oracle 让现实可计算;AI Oracle,让智能可计算。

Oracle 不再只是桥梁,

而是智能文明的信任层。

写在最后

如果区块链是文明的记忆层,Oracle 就是文明的感官层。

我们正在教机器一件前所未有的事:

如何诚实地感知。

当智能社会真正到来,Oracle 将不只是传递数据,而是传递真理的形式。