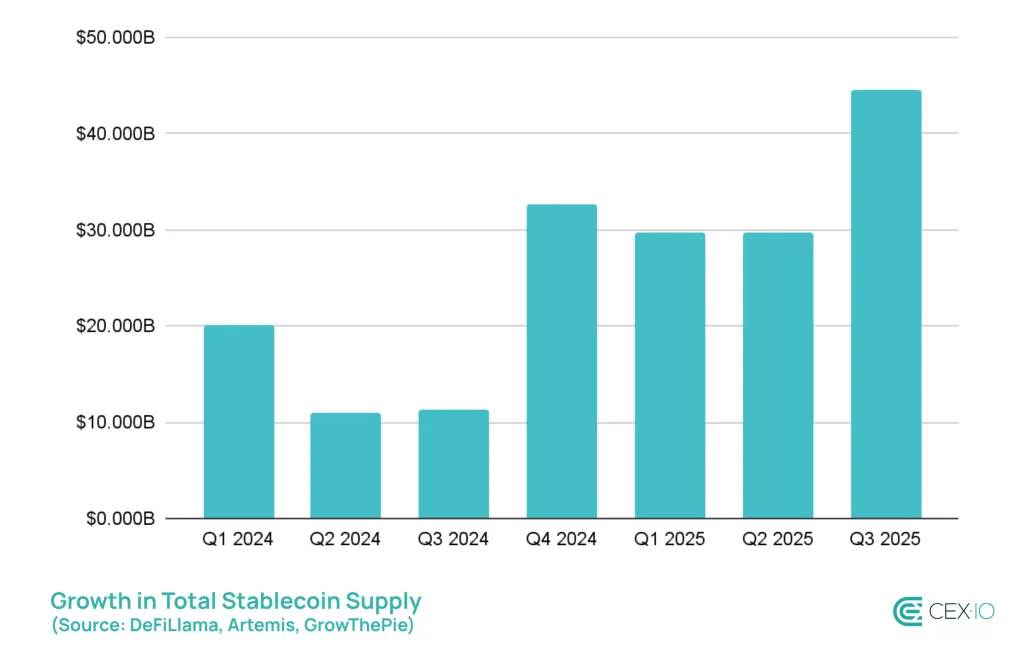

В III квартале общее предложение «стабильных монет» выросло более чем на $45 млрд — самый большой показатель за всю историю. Об этом говорится в отчете CEX.io.

Совокупный показатель превысил $300 млрд.

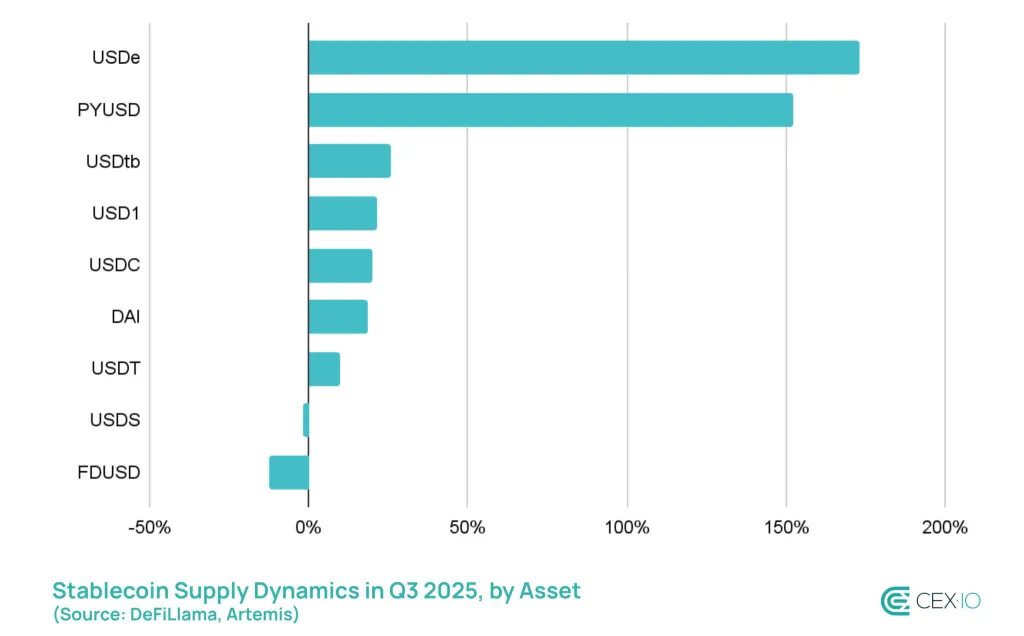

84% новой эмиссии за июль-сентябрь пришлось на USDT, USDC и USDe. При этом 69% от «напечатанного» объема выпущено в основной сети Ethereum.

По приросту предложения лидируют USDe и PYUSD (+173% и +152% соответственно), несмотря на закон GENIUS Act, запрещающий доходные стейблкоины в США.

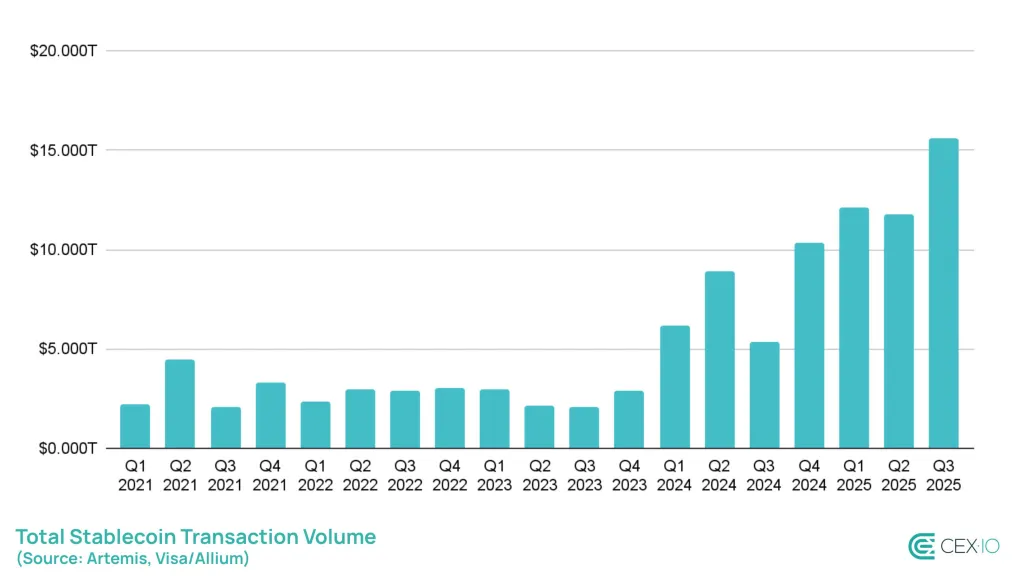

Общий объем торгов «стабильными монетами» в III квартале достиг $10,3 трлн, что сделало его самым активным с первой половины 2021 года. Среднесуточный показатель вырос до $124 млрд — он более чем вдвое превышает значения августа-июня.

«Первоначально отскок был обусловлен возросшей активностью на более широких рынках криптовалют, но позднее в том же квартале стейблкоины также стали ключевым инструментом оборота капитала, поскольку осторожность начала расти», — объяснили авторы отчета.

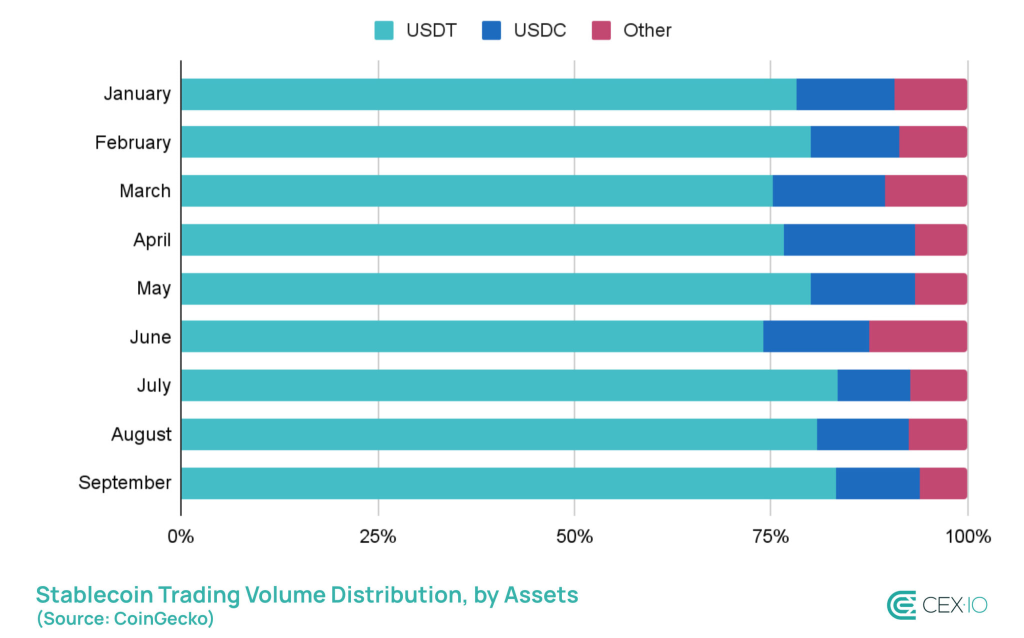

USDT удалось укрепить доминирование по объему торгов. Его доля в квартальном выражении выросла с 77,2% до 82,5%, в то время как у USDC снизилась с 14,5% до 10,5% . Другие монеты тоже потеряли позиции.

Стейблкоин Tether обогнал монету от Circle по обороту на DEX, впервые превысив месячный показатель в $100 млрд. Это свидетельствует о том, что доминирование USDT все больше распространяется на децентрализованные биржи, потенциально подрывая позиции USDC в DeFi, отметили в CEX.io.

Рекордный оборот и боты

За прошедшие три месяца совокупный объем транзакций со «стабильными монетами» вырос до исторического максимума в $15,6 трлн. Доля органических переводов выросла более чем на 30%, достигнув нового рекорда в $2,9 млрд.

Однако боты продолжают доминировать, составляя 71% всех ончейн-транзакций со стейблкоинами.

«Рост количества автоматизированных переводов был наиболее заметен в августе и оставался высоким до сентября, несмотря на некоторое охлаждение рынка. Всплеск активности ботов и немаркированных высокочастотных транзакции может вызвать вопросы о возможном распространении фиктивной торговли и не имеющих экономической ценности операций», — отметили исследователи.

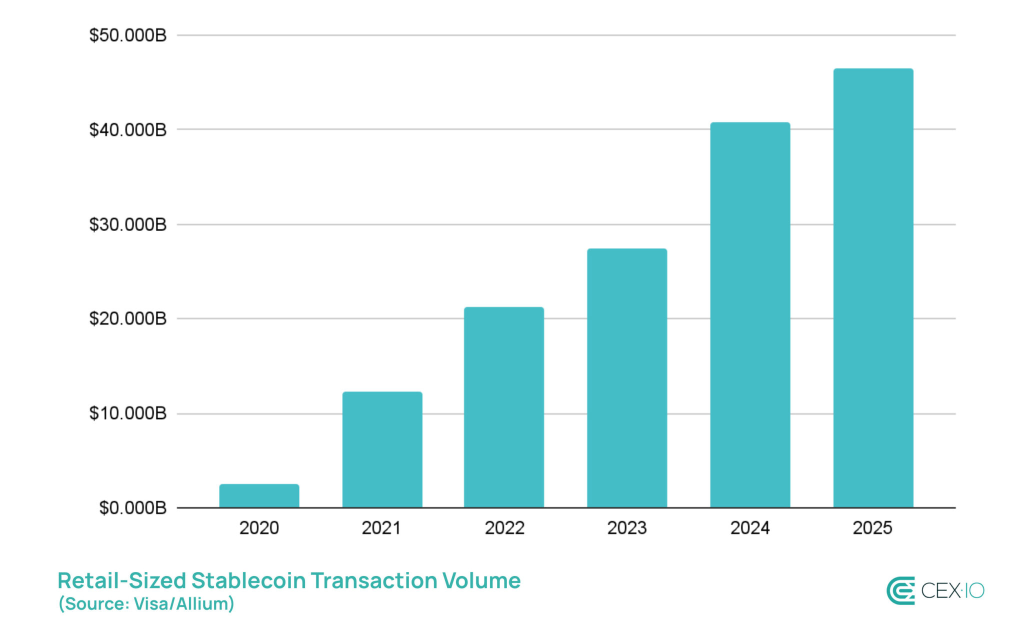

Среди органический переводов наиболее сильно выделился ритейл (транзакции на сумму менее $250). Показатель достиг нового исторического максимума, что помогло 2025 году стать «самым активным годом в истории розничного использования стейблкоинов».

«III квартал подтвердил, что стейблкоины больше не являются просто вспомогательным инструментом для криптовалютных рынков — они становятся ядром расчетов и даже шлюзом для розничного внедрения. Заглядывая в IV квартал, можно сказать, что эта динамика, вероятно, сохранится», — заключили эксперты.

Напомним, в сентябре аналитики Moody’s указали на риски бума «стабильных монет» для денежного суверенитета и финансовой стабильности.