原创 | Odaily 星球日报(@OdailyChina)

作者|Azuma(@azuma_eth)

本栏目旨在覆盖当前市场上以稳定币(及其衍生代币)为主体的低风险收益策略(Odaily 注:代码风险永远无法排除),以帮助那些希望通过 U 本位理财来逐渐放大资金量级的用户寻找较为理想的生息机会。

往期记录

懒人理财攻略|Katana、Agora 一鱼双吃;Huma 2.0 再次开门(7 月 16 日);

懒人理财攻略|Ethena 启动 USDe、sUSDe 循环贷激励;Falcon Finance 新增 60 倍积分加速渠道(8 月 4 日);

懒人理财攻略|币安推出核弹级 USDC 补贴计划;Kamino 第四季激励活动启动(8 月 12 日);

懒人理财攻略|币安加码 USDC 补贴;融资 1300 万美元的“AI 稳定币”要开挖了(8 月 18 日);

懒人理财攻略|币安 Plasma USDT 存款活动仍有额度;USD.AI 收益及积分两手抓(8 月 27 日);

新增机会

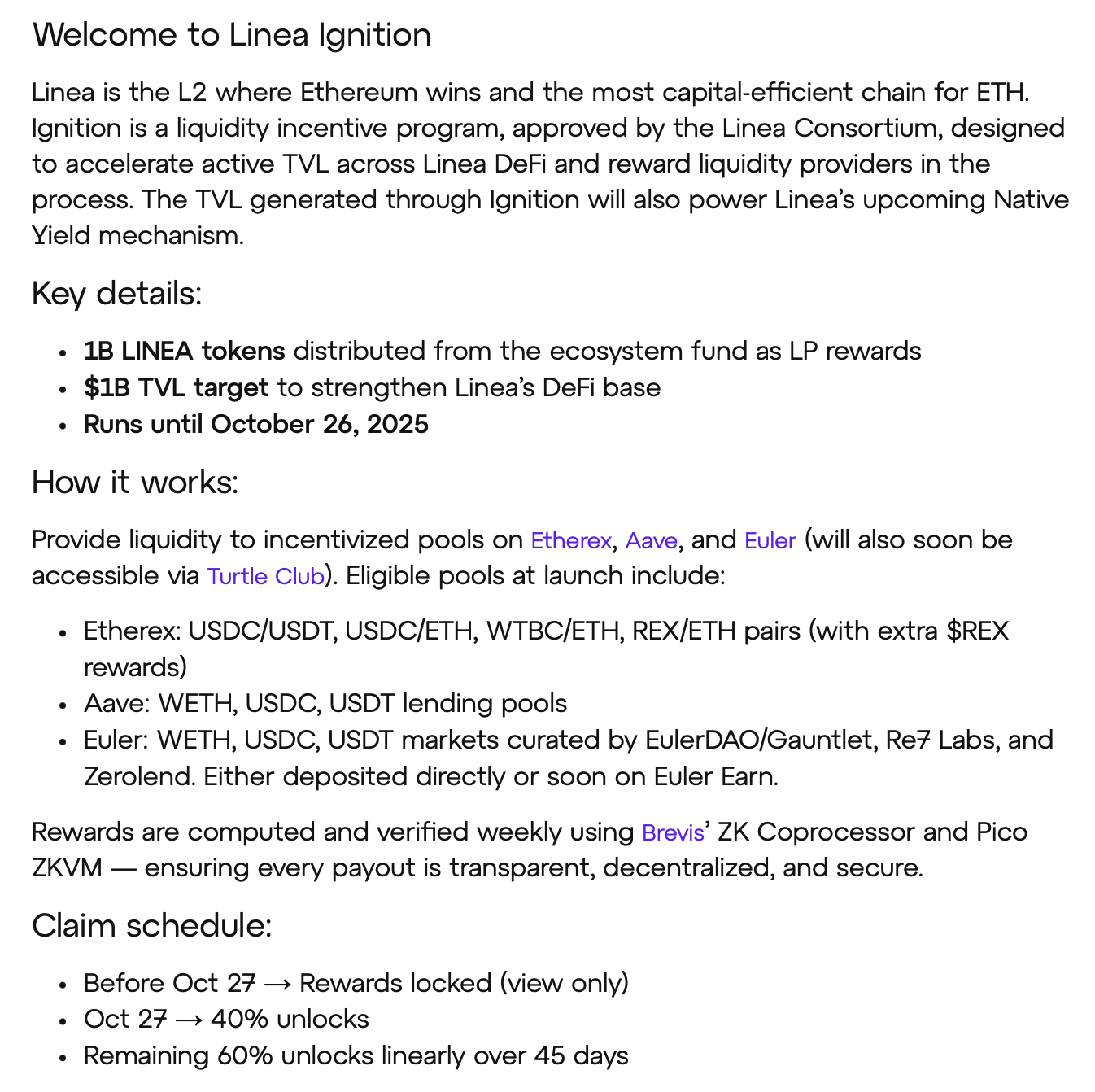

Linea 启动流动性激励计划

昨日晚间,Linea 官方宣布将启动流动性激励计划 Linea Ignition,计划分发 10 亿 LINEA 代币作为激励,以为 Linea 额外吸引 10 亿美元 TVL。

活动将持续至 2025 年 10 月 26 日,启动阶段符合资格的合作协议包括 Etherex、Aave、Euler(后续预计还将增加 Turtle Club),可参与的流动性池包括:

- Etherex:USDC/USDT、USDC/ETH、WTBC/ETH、REX/ETH 交易对(含额外 REX 奖励)

- Aave:WETH、USDC、USDT 借贷池;

- Euler:由 EulerDAO/Gauntlet、Re7 Labs 和 Zerolend 管理的 WETH、USDC、USDT 池,可直接存款或通过 Euler Earn 参与(即将开放)。

奖励方面,激励代币中的 40% 将在 10 月 27 日解锁,剩余 60% 在 45 天内线性解锁。

截至发文,LINEA 在币安盘前市场暂报 0.033 美元,以该价格静态计算,10 亿枚代币即对应约 3300 万美元的总奖池,考虑到整个活动周期并不长,代币虽有一定的锁仓限制,但解锁周期也很短,所以还是蛮有参与性价比的 —— 建议无脑存 Aave,可以考虑适当上一些循环贷。

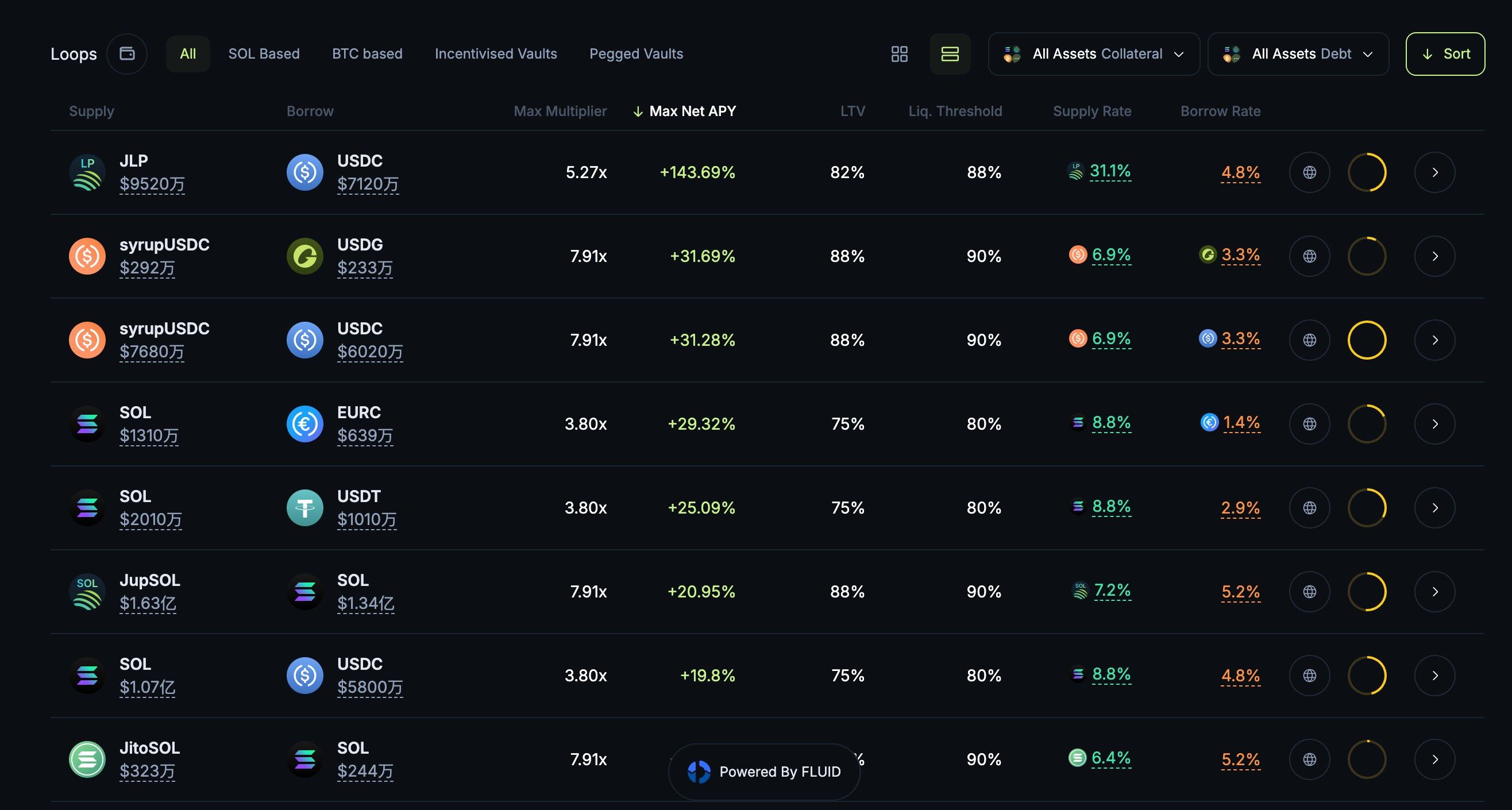

Jupiter Lend 正式上线

Jupiter 与 Fluid 合作推出的借贷产品 Jupiter Lend 上周正式上线,且很快就成为了 Solana 生态势头最猛的借贷协议之一。

目前在 Jupiter 直接存入 USDC、USDT、USDS 等稳定币,年化基本都在略低于 10% 的水平,虽然并不算高,但胜在 Jupiter 与 Fluid 的安全背书,且奖励会以相应稳定币的形式发放(收益相对较高的 Kamino,部分收益会以 KMNO 行形式发放)。

此外,Jupiter Lend 自带的一键循环贷功能(Multiply)还比较好用,有过相关操作经验的用户可以适当上一些杠杆来放大收益率 —— 这里最推荐的其实是 SOL 持仓用户,JupSOL/SOL 的循环贷风险更可控,收益在所有 SOL 生息产品中也相对可观。

Cap 进一步集成 Pendle

前一周提到过的生息稳定币 Cap 已完成了与 Pendle 的进一步集成 —— 此前仅支持生息资产 stcUSD,现在新增支持了积分资产 cUSD。

上周推荐时 Cap 尚处于 Epoch1 的阶段,静态持有 cUSD 可获得 20 倍积分加成,但不会有任何年化收益。本周 Epoch2 正式启动,静态持有 cUSD 的积分倍率下调为 10 倍,同时仍不会有任何年化收益,但选择在 Pendle 内投入 cUSD 的 LP,即可继续获取 20 倍的积分增幅,同时也可吃到 8.3% 的 APY,没有不挪的道理。

其他观望协议:USD.AI、Reflect

USD.AI 上周也曾推荐过,但万万没想到这项目进度如此迅猛,先是融资 1300 万美元,之后又拿了币安(YZi Labs)的钱,再然后又是和大热稳定币公链 Plasma 搭上了线,以至于初始存款限额快速被打满。USD.AI 此前已预告后续会对 USDT 开放更多存款限额,建议保持关注,有机会的尽早占坑。

Reflect 今早宣布完成 375 万美元种子轮融资,由 a16z crypto 旗下 CSX 加速器领投,Solana Ventures、Equilibrium、BigBrain Holdings 与 Colosseum 等参投。Reflect 计划构建“软件即稳定币”基础设施,使应用无需锁定资金即可发行可生息的美元稳定币,该项目预计将于 9 月初上线主网,首批支持 Solana 上的 USDC,到时候可以看看收益率情况。