撰文:Alex Liu,Foresight News

DWF 联创说:「能以任意资产进入,得到收益,再以任意资产退出到任意地方的协议,就是 Falcon Finance。」

这是一个宏大的的愿景,听上去并不像是在描述一个稳定币项目,而这正是 USDf 的独特之处 —— 现在市面上有太多的稳定币,有时甚至感觉「千篇一律」,难以发现差异,但最后赢家总会是与众不同的那个。

与众不同不代表「对」,Falcon 不同在哪里,它会不会是赢家?

出身不同

USDf (Falcon Finance)的出身就不同。

Falcon Finance 的创始人和团队来自 DWF Labs,其联合创始人 Andrei Grachev 同时担任 Falcon 的管理合伙人。

DWF Labs 和 DWF Ventures 是业内资深做市商与投资机构,曾参与多种主流山寨币和知名 Meme 币的做市,在本轮周期中可谓是战绩斐然。做市商下场做稳定币,尚属首例。

Falcon Finance 底层的收益策略依赖大量的对冲交易,类似于 Ethena,是将交易收益分发给用户,披着生息稳定币外壳的交易公司。(详见:稳定币外衣之下,ENA 是模式创新还是估值骗局)

而做市商的身份让其在交易与收益策略的执行上具有天然的优势。

资本不同

支持 Falcon Finance 的资本也不同。

Falcon Finance 本身由 DWF Labs 支持。DWF Labs 在今年 4 月以 0.1 美元均价向特朗普家族加密项目 World Liberty Financial(简称 WLFI)投资了 2500 万美元,并表示将支持其稳定币 USD1 的流动性。(市场同时默认 DWF Labs 将会成为 WLFI 代币的做市商。)

2025 年 7 月 30 日,Falcon Finance 宣布 WLFI 向其投资 1000 万美元。这是 WLFI 在稳定币领域的首笔投资,而 WLFI 拥有自己的美元稳定币 USD1(以美国国债和现金等实物资产为抵押)。双方表示融资将用于加速 Falcon 跨链兼容性、USDf 与 USD1 之间互操作性等技术集成。

Falcon 官方表示,USD1 已被纳入 Falcon 的抵押品列表,未来将推出 USDf/USD1 的跨链转换工具,从而为两者形成互补格局。

WLFI 代币已在币安盘前合约市场上线,完全流通市值(FDV)超 200 亿美元,相关概念币(如 DOLO 等)均在近期表现不俗。资本不同带给 Falcon 的「WLFI 概念」加成,大概率是积极的。

模式不同

Falcon 的模式(收益来源、铸造机制等)也不同。

市场上有其他的以对冲交易利润为收益来源的稳定币项目,例如 Ethena 协议的 USDe/sUSDe。与以法币为完全抵押的传统稳定币不同,Ethena 的 USDe 同样是合成美元,但模式是以 BTC、ETH、SOL 等加密资产配合永续合约持仓进行对冲(delta-hedging),并持有一定量的主流稳定币来稳定机制。

而 Falcon 的收益来源如下,加上跨所价格套利等「做市商专长」后,更加多样与复杂。

与多数稳定币不同,USDf 并非由单一资产担保,而是采用多资产超额抵押加上对冲策略:所有发行的 USDf 都需要有超过 1 美元价值的抵押品支撑,协议当前的抵押率在 110%~116% 之间。

Falcon 的设计允许用户以多种资产铸造 USDf:既支持主流稳定币(如 USDT、USDC、DAI),也支持主流加密货币(如 BTC、ETH、SOL)及其他精选山寨币。官方表示,未来还将接入更多资产类型,包括代币化的现实世界资产(RWA)等。

用户可以通过两种方式获得 USDf:一是在 Falcon 官方应用上铸造 USDf(需通过 KYC 审核并满足最低金额要求),铸造时可选择「传统模式」或「创新模式」(一种低层为期权的包装玩法)进行抵押;二是直接在去中心化交易所(如 Uniswap、Curve 等)购买 USDf,无需 KYC 或最低额限制。无论哪种方式,都可享受平台的积分激励「Falcon Miles」,不过直接铸造抵押非稳定币可获得更高的积分倍率。

在 USDf 获取之后,用户可以通过多种途径参与生态并获得收益。

-

持币收益 —— 简单持有 USDf 可每天获得 6 倍积分奖励;

-

质押收益 —— 用户可将 USDf 质押成 sUSDf 来赚取利息,支持无锁定(基础收益)和定期锁定(更高收益)两种模式;

-

流动性挖矿——USDf 可在主流 DEX(Uniswap、Curve、PancakeSwap 等)或聚合器(Convex、StakeDAO 等)中提供流动性,获取交易手续费并同时赚取积分(最高 40 倍);

-

借贷与杠杆——Falcon 已接入像 Morpho、Euler、Silo 等借贷市场,支持将 USDf 或 sUSDf 作为抵押借贷和循环挖矿;

-

收益(Yield Tokenization)协议(如 Pendle)也可以使用 USDf,通过分离未来收益流(铸造「SY/YT」代币)让用户进一步投机积分或锁定固定收益。推荐阅读:Pendle 难懂,但不懂它是你的损失

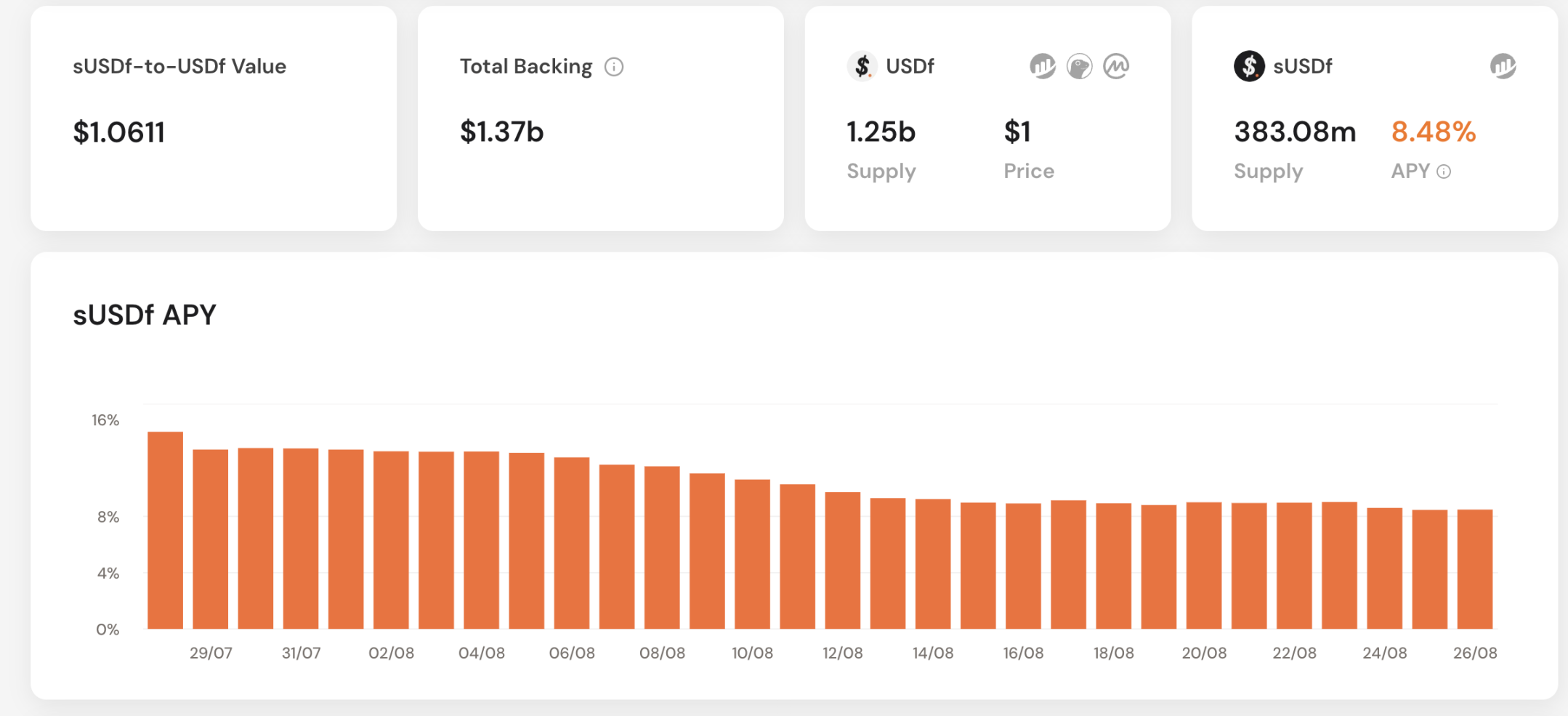

截止今天(8 月 26 日),USDf 的流通供应量为 12.5 亿美元,作为新兴协议位居所有稳定币发行量前 10。生息版本 sUSDf 供应量为 3.83 亿枚,提供 8.48% 的年化收益率。

愿景不同

正如开头所讲,Falcon 的愿景也不同,不局限于「稳定币」的范畴。

Falcon Finance 定位为一个 「通用抵押基础设施」,旨在将各种可托管资产(包括加密代币、法币挂钩代币,以及代币化的现实资产)转化为与美元挂钩的链上合成流动性。

Falcon 不仅是想发行一种新稳定币,而是打造一个可容纳多种资产、多种市场的金融连接层 —— 以任意资产进入,得到收益,再以任意资产退出到任意地方。

联创 Andrei Grachev 多次强调,USDf 的设计目标是让诸如美国国债、股票等传统金融资产能够上链并产生流动性与收益。

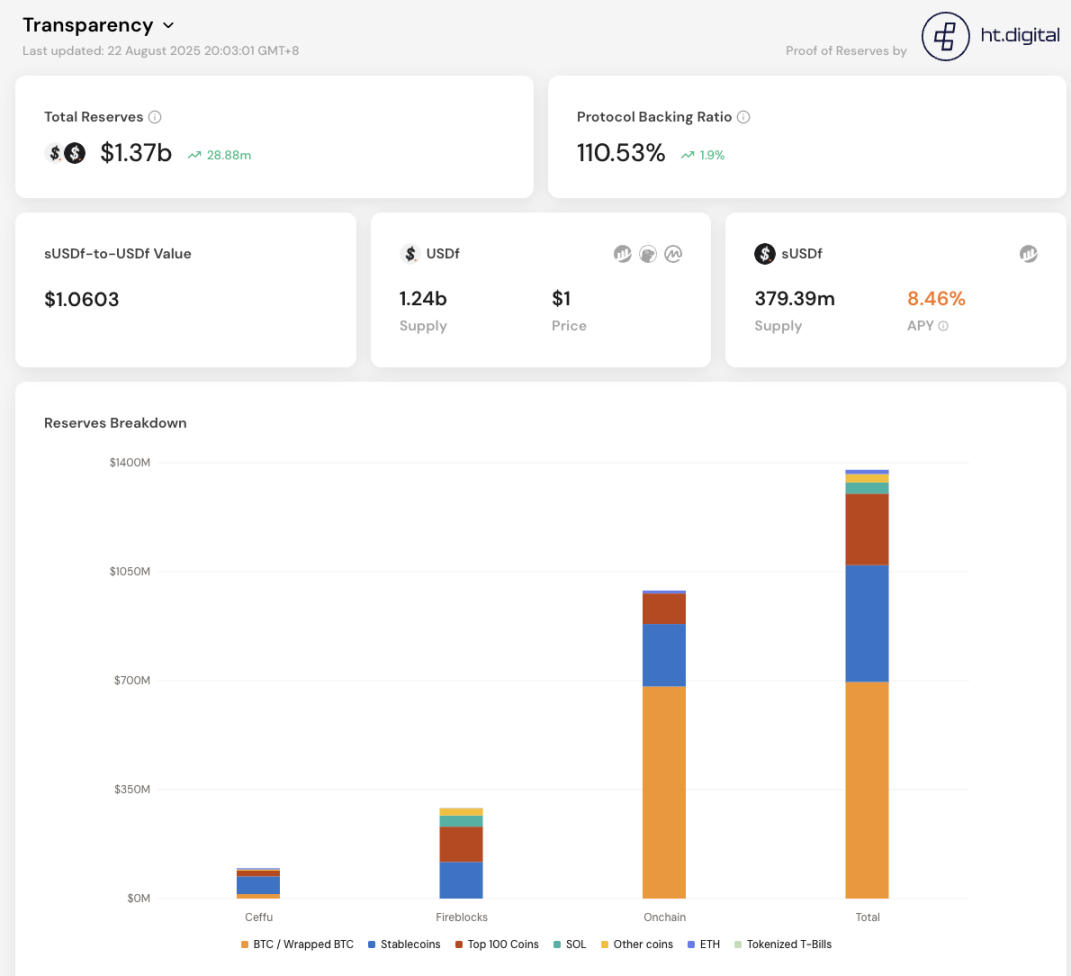

Falcon 实现这一目标的方式,是将真实世界资产与 DeFi 生态(交易、借贷、做市等)通过协议逻辑进行高效串联,并且以透明的风控和高等级的合规性为基础。官方还设计了包括审计、透明度报告面板等机制来增强信任:例如最新上线的透明度仪表盘公开展示了 USDf 背后有超过 110% 的备付金,并且采用第三方审计验证。Falcon 的产品团队还计划定期发布更详细的储备证明和审计报告,以满足机构用户对于安全和合规的要求。

路线不同

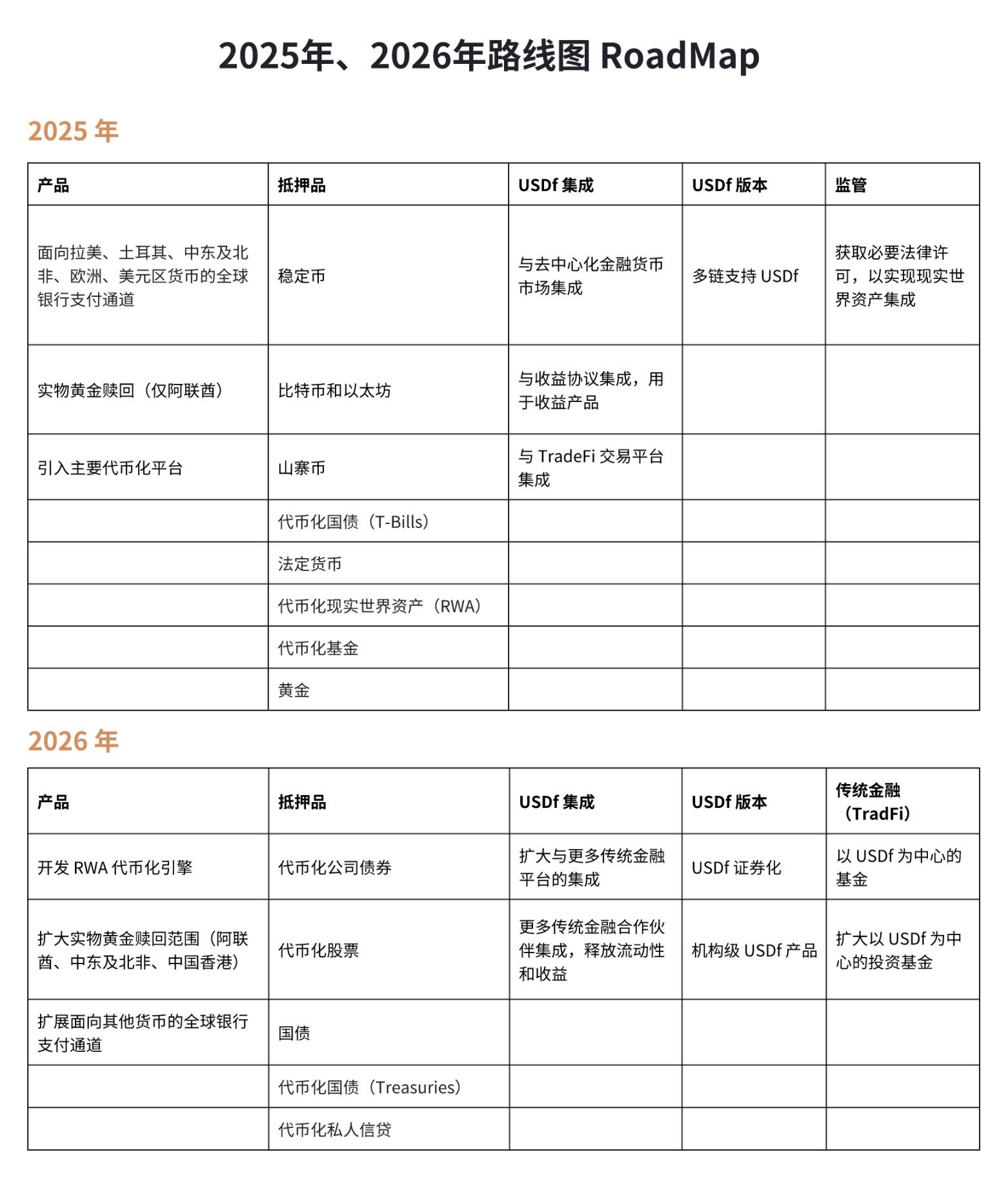

由于上述区别,Falcon 的项目路线图也与常规的稳定币项目大为不同。

据官方路线,2025 年底前,Falcon 将重点扩展美元流动性的「法币通道」并实现多链部署:计划在拉美、土耳其、欧元区等主要市场开通受监管的法币入金渠道,提供 24/7 实时结算,并将 USDf 推向包括以太坊 L2 和其他公链的 Layer1/Layer2,以提升跨链资本效率。

团队还在推进与持牌托管机构和支付机构合作,推出类似银行级的 USDf 产品,如资金隔夜收益管理和货币市场基金通道,并考虑在全球主要金融中心(如中东、香港等)增加实物黄金的链上兑换服务。到 2026 年,Falcon 计划构建「现实资产引擎」,支持公司债、私募信贷等资产代币化接入,并推出 USDf 投资工具和结构化证券产品,以适应更大规模的机构需求。

如何参与

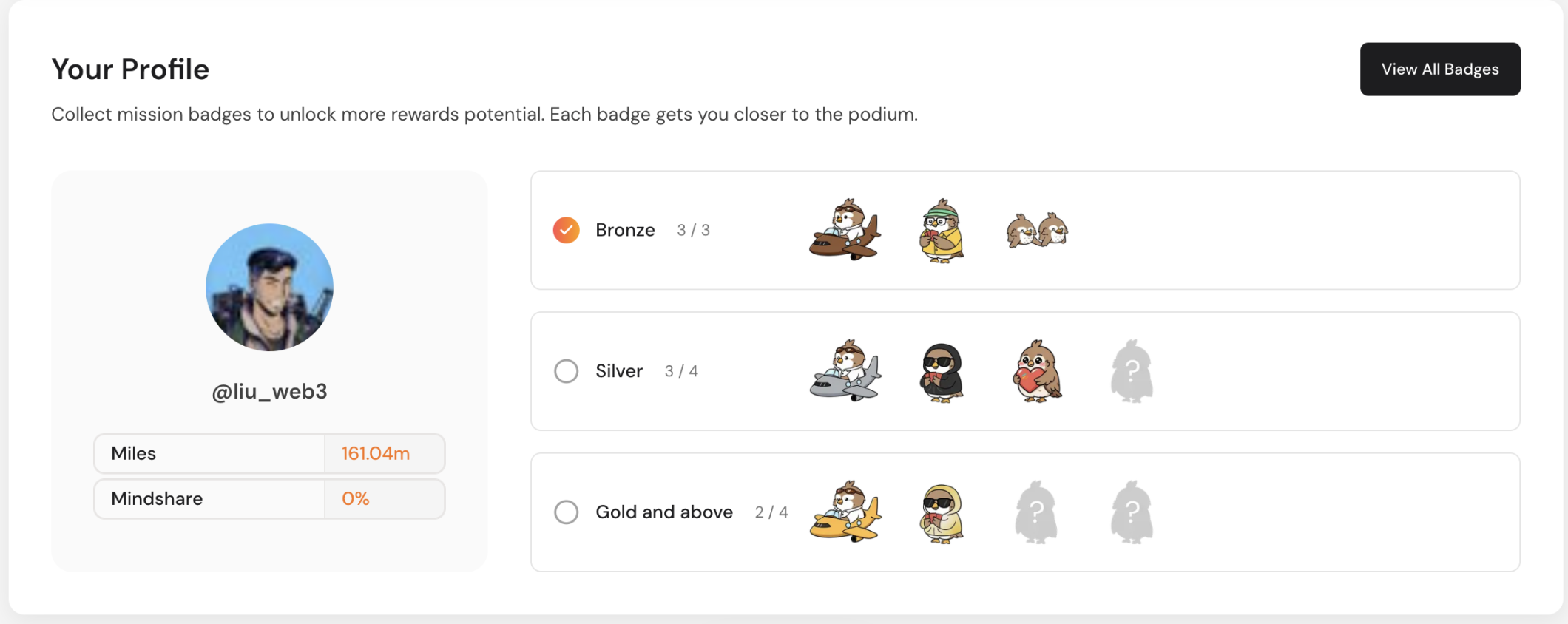

在社区层面,Falcon 也推出了一系列激励活动以扩大生态参与度,包括 Falcon Miles 积分和 Yap2Fly 社交排行榜。

Falcon Miles 即项目的积分体系,往往会和之后项目的空投直接挂钩,获取方式上文中已有提到。

Yap2Fly 是 Falcon 与 Kaito 合作推出的活动,将综合计算用户的 Falcon Miles 和在社交媒体上发帖 Yap 获得的「Mindshare」产生排名。每月会将约 5 万美金的 USDf 奖励池分发给排名前 50 的用户,徽章系统除用于解锁奖励比例外,还可能会有额外奖励。

综合而言,Falcon Finance 目前拥有超过 10 亿美元的 USDf 流通量和总锁仓量,在合成美元协议中规模领先。

其独特之处在于「用大规模资产做抵押来创造链上流动性,并且让这些资产本身继续产生收益」。项目团队强调通过严谨的风控、合规规划与多元化资产接入来吸引机构级用户,而不仅仅是面向普通 DeFi 用户。

在未来的发展中,Falcon Finance 有望通过扩展多样化资产种类和多链部署,继续探索 DeFi 与传统金融之间的融合路径。

声明:本文作者持有 sUSDf YT,价值达到披露标准。