Author: Bright Company

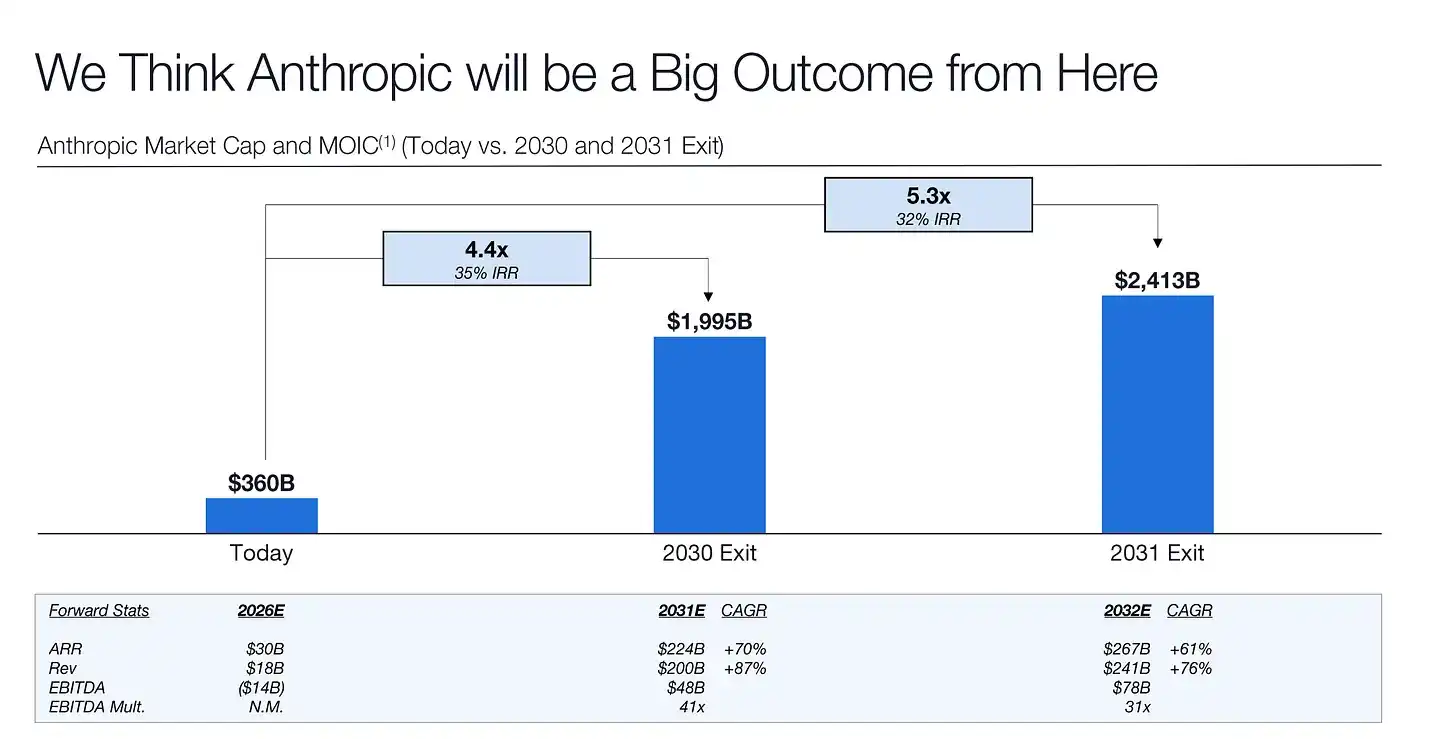

According to the Substack account Newcomer, renowned investment firm Coatue Management predicted in an internal investor presentation from January that Anthropic's valuation would soar to $1.995 trillion by 2030.

Based on the Coatue PPT released by Newcomer, Anthropic is projected to achieve revenue of $18 billion in 2026, but with an EBITDA loss of $14 billion, and its ARR is expected to reach $30 billion by the end of the year.

By 2031, the company's revenue is anticipated to jump to $200 billion, with an EBITDA profit of $48 billion, and ARR further climbing to $224 billion.

Using this as a basis, Coatue applied a 41x forward EBITDA multiple to derive a valuation of $1.995 trillion for 2030, suggesting it could potentially rise to $2.413 trillion in 2031.

In February of this year, Anthropic just completed a new round of financing. Coatue and Singapore's sovereign wealth fund GIC co-led Anthropic's $30 billion Series G funding round, resulting in a post-money valuation of $380 billion. This round of financing is among the largest in the history of the AI field, with participation from other top-tier institutions including D.E. Shaw Ventures and Founders Fund. Coatue founder Philippe Laffont stated at the time that the firm is highly confident in Anthropic's positioning in enterprise AI and Agent Coding.

However, Anthropic's actual growth rate has already partially exceeded Coatue's optimistic expectations. By early March, the company's ARR had approached $20 billion, doubling from $9 billion at the end of 2025, with particularly significant growth in February alone. Anthropic CEO Dario Amodei confirmed at a Morgan Stanley conference that products like Claude Code have made outstanding contributions, with enterprise customers accounting for as much as 80% of the business, and consumption-based billing models further amplifying revenue elasticity.

As a major competitor to OpenAI, Anthropic is known for its "safe and reliable" AI philosophy, and its Claude series of models are rapidly penetrating the coding and enterprise application markets. Since 2025, weekly active users of Claude Code have doubled, and the proportion of code generated by it on GitHub has significantly increased. The company achieved the leap from zero to tens of billions in revenue in less than three years, a growth rate far surpassing that of early cloud computing giants. The generative AI market is in a period of explosion, driven by data centers, computing power demands, and enterprise digital transformation, collectively fueling expectations of trillion-dollar growth.