来源:NBC News

编译及整理:比推 BitpushNews

当地时间周四, 200 多位富有的、大多数匿名的加密人士将前往华盛顿与美国总统唐纳德·特朗普共进晚餐。

据区块链分析公司 Nansen 的数据分析,此次入场券的代价不菲,这些「赢家」在特朗普官方加密货币代币 $TRUMP 上的花费从 5.5 万美元到 3770 万美元不等。

晚宴组织者通过在特定时间点持有 $TRUMP 代币的多少来决定获得席位的资格。Nansen 发现,这些「赢家」总计在特朗普的官方加密货币上花费了 3.94 亿美元,尽管其中一些人在竞赛结束后已出售了部分或全部持仓。当然,花费差异巨大:前七名每人花费超过 1000 万美元,而末尾 24 名每人花费不足 10 万美元。

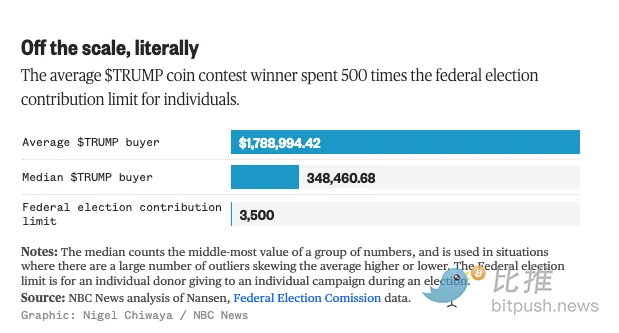

研究显示,有三分之一(67 人)的「赢家」花费超过 100 万美元,平均到每位「赢家」的花费为 1, 788, 994.42 美元。

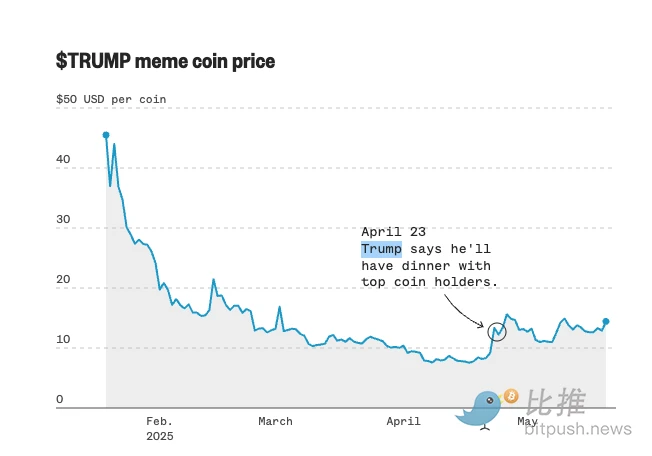

据追踪加密货币价格的 CoinMarketCap 显示,与许多 Meme 币类似,$TRUMP 的价值波动剧烈,Nansen 追踪了每位「竞标者」在购买 $TRUMP 时的花费。

这 220 名买家受邀参加在特朗普国家高尔夫俱乐部(华盛顿特区)举办的晚宴,尽管竞赛网站声称特朗普「作为嘉宾出席晚宴,不为此募集资金」,但其同时指出,$TRUMP 代币项目 80% 的所有权归两家与特朗普相关的公司——CIC Digital 和 Fight Fight Fight LLC 所有。

这场于上周一结束的个人加密货币及相关竞标活动,为特朗普看似利用总统职位谋取私利的行为又添一例。

他的商业利益由其子小唐纳德·特朗普控制的信托基金持有,而且他将许多家族企业与其总统活动交织在一起,包括在他的社交俱乐部(如这次加密货币晚宴)举办活动,以及在其社交媒体应用 Truth Social 上发布独家政治声明。

特朗普的加密货币也通过交易为其关联公司带来收益。每笔 $TRUMP 代币交易都会产生一笔交易费。另一家加密货币研究公司 Chainalysis 估计,在竞赛宣布后的头两天内,$TRUMP 代币就产生了近 90 万美元的交易费。

布伦南司法中心(Brennan Center for Justice)选举和政府项目主任 Dan Weiner 告诉 NBC News,虽然大多数联邦雇员被法律禁止利用职务谋取经济利益,但总统却在很大程度上获得豁免。

Dan Weiner 表示:「总统不受制于几乎所有其他联邦政府工作人员都适用的广泛利益冲突禁令。」他说:「总体而言,即使按照第一届特朗普政府的标准来看,这都相当疯狂,那时各种人都在总统的酒店做生意。现在这远远超出了那个范畴,但这并不一定意味着他违法。」

白宫发言人安娜·凯利(Anna Kelly)在一份声明中表示:「总统正在努力为美国人民争取更好的协议,而不是为他自己。特朗普总统只为美国公众的最佳利益行事——这就是为什么他们尽管面临多年来自虚假新闻媒体对他及其企业的谎言和虚假指控,仍然绝大多数地再次选举他担任此职务。」

即便排名垫底的赢家,其花费也远超美国公民直接捐赠给政治候选人的合法上限— 3500 美元。

本周二,最高花费者公布身份为加密企业家孙宇晨(Justin Sun),他曾于 3 月告诉福布斯,他已成为加勒比小岛国圣基茨和尼维斯(St. Kitts and Nevis)的公民。孙宇晨曾被美国证券交易委员会(SEC)起诉,但在特朗普执政期间,此案已被暂停。

大多数其他竞赛赢家的身份仍未公开,仅通过其化名和加密货币钱包地址为人所知。然而,据独立加密研究员 Molly White 分析,大多数与会者似乎是外国国民。Molly White 追踪了每个获胜钱包在不同加密货币交易所的交易,并注意到持有者似乎使用了法律上不允许美国公民使用的交易所。

Molly White 告诉 NBC News,在 220 个与竞标获胜者相关的钱包中,有 158 个(占 72% )似乎是外国钱包。

《纽约时报》的一项调查报道称,获胜者榜单中包括来自新加坡和澳大利亚的加密货币企业代表。

Dan Weiner 指出,竞标获胜者中,非美国公民的比例很高值得注意,因为非美国公民向美国政治候选人捐款通常是非法的。

他说:「这是一个令人难以置信的对比。我们有非常严格的法律禁止外国国民进行竞选捐款。所以,这里的巨大讽刺在于,许多购买这种货币的人本无资格向总统竞选捐款 100 美元。我们有一系列旨在防止这些发生的法律,这实际上是两党都同意应该避免的合法事情。然而,这种情况却正在上演。」