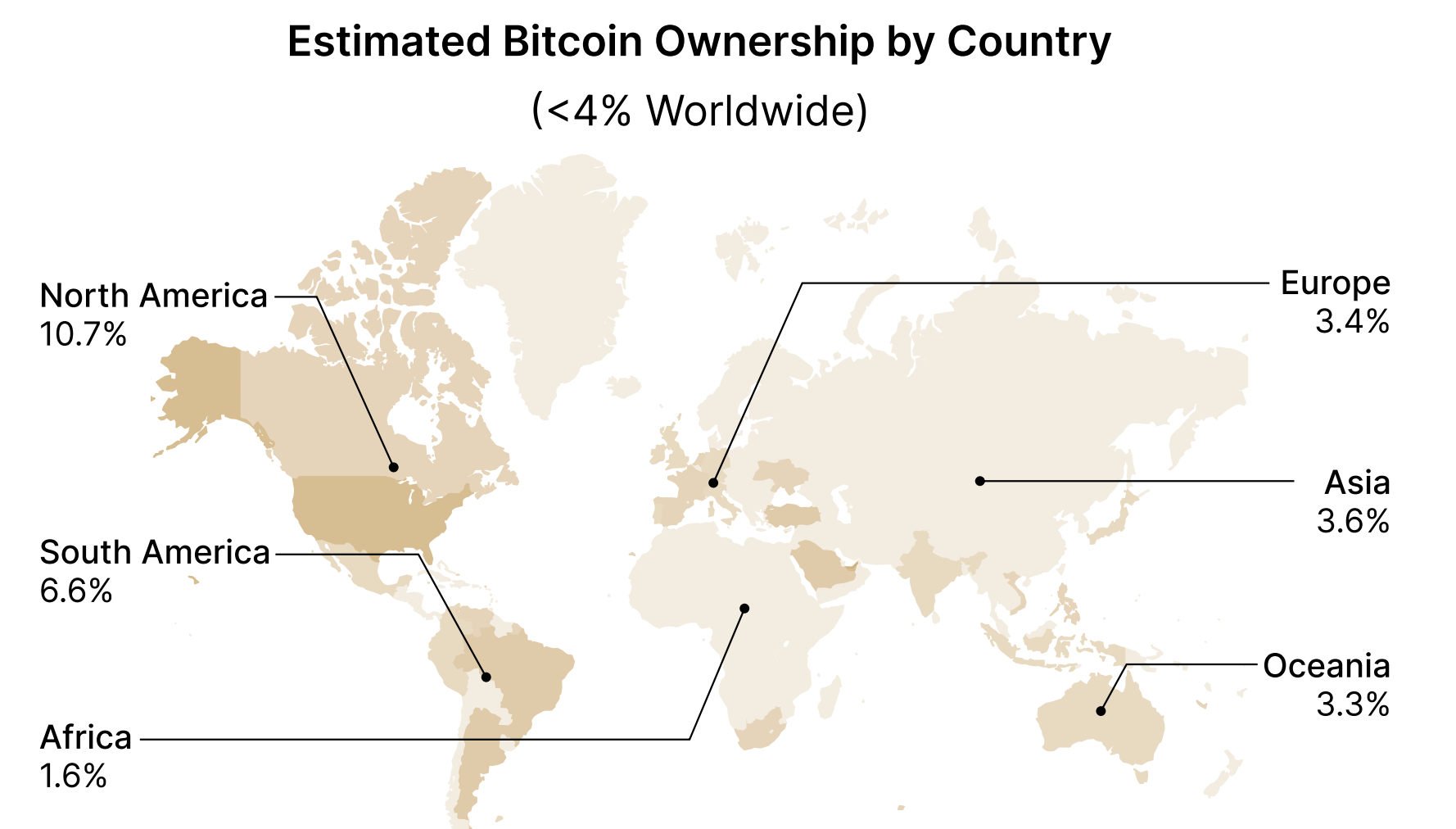

В настоящее время биткоинами владеют только 4% населения мира, при этом самая высокая концентрация владения приходится на Соединенные Штаты, где, по оценкам, 14% людей владеют BTC.

Согласно исследовательскому отчету River, компании по финансовым услугам BTC, Северная Америка остается континентом с самым высоким уровнем принятия среди частных лиц и учреждений, в то время как Африка в настоящее время имеет самый низкий показатель — всего 1,6%.

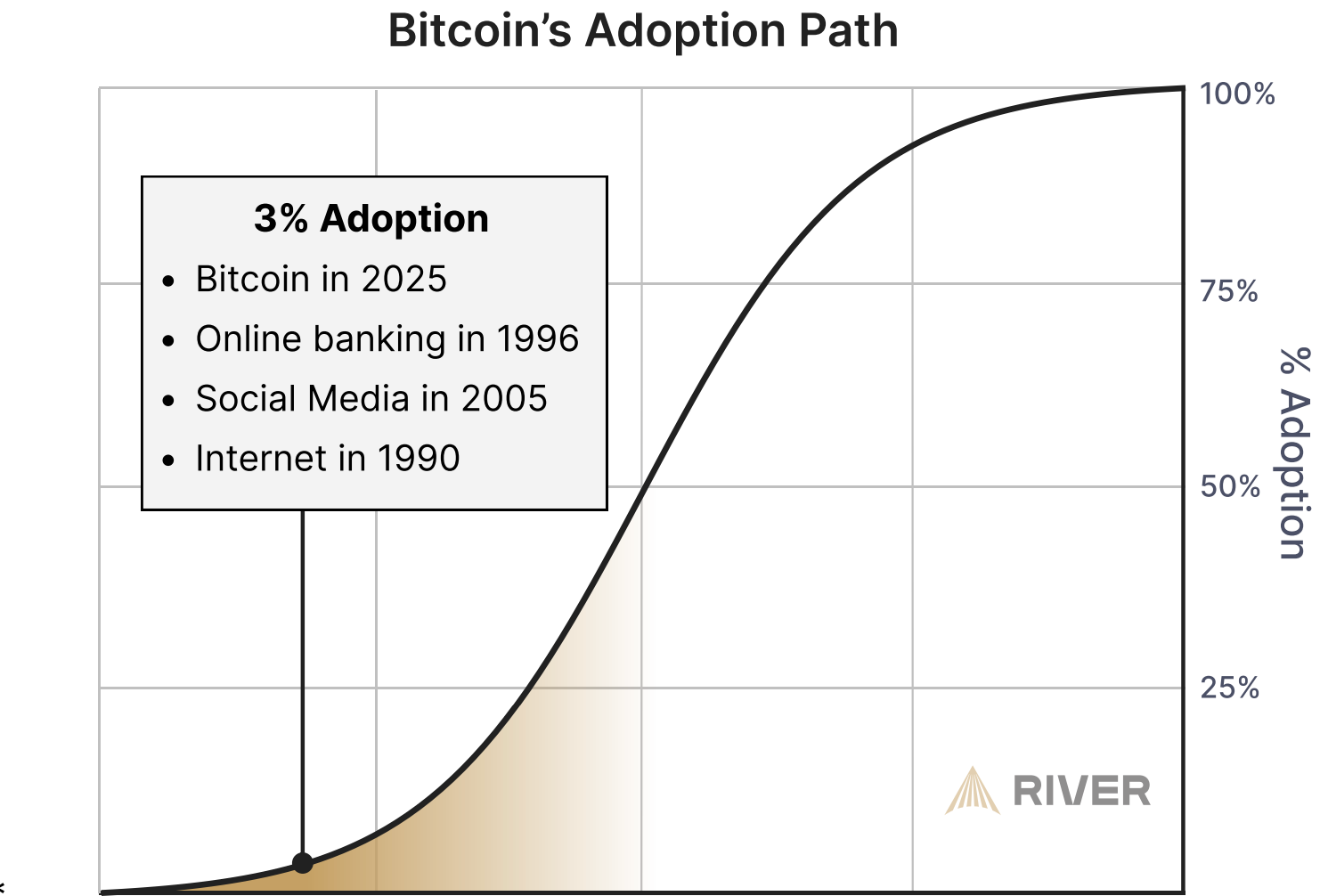

В целом, принятие BTC, как правило, было выше в более развитых регионах, чем в развивающихся. River оценивает, что BTC достиг только 3% от своего максимального потенциала принятия, что свидетельствует о том, что цифровая валюта все еще находится на ранних стадиях глобального принятия.

Путь принятия биткоина пройден всего на 3%. Источник: River

Финансовая компания пришла к цифре 3%, рассчитав общий адресный рынок биткоина, который включает правительства, корпорации и учреждения — всего 1%.

River также учла институциональное недораспределение и индивидуальные ставки владения, чтобы прийти к метрике 3%.

Хотя биткоин прошел долгий путь с первых дней шифропанка, недавно став резервным активом правительства США, на пути массового принятия биткоина в мировом масштабе стоит несколько препятствий.

Оценочное владение биткоинами по географическим регионам. Источник: River

Что мешает массовому принятию?

Биткоин находится на стыке технологий и финансов — двух тем, которые сами по себе достаточно плотные, не говоря уже о совокупности.

Самая большая проблема, с которой сталкивается массовое принятие биткоина, — это отсутствие финансового и технического образования, что подпитывает заблуждения о BTC, включая идею о том, что это мошенничество или финансовая пирамида.

Цифровые активы также печально известны своей высокой волатильностью — это друг краткосрочного трейдера, но враг любого, кто использует BTC в качестве средства обмена или хранилища ценности.

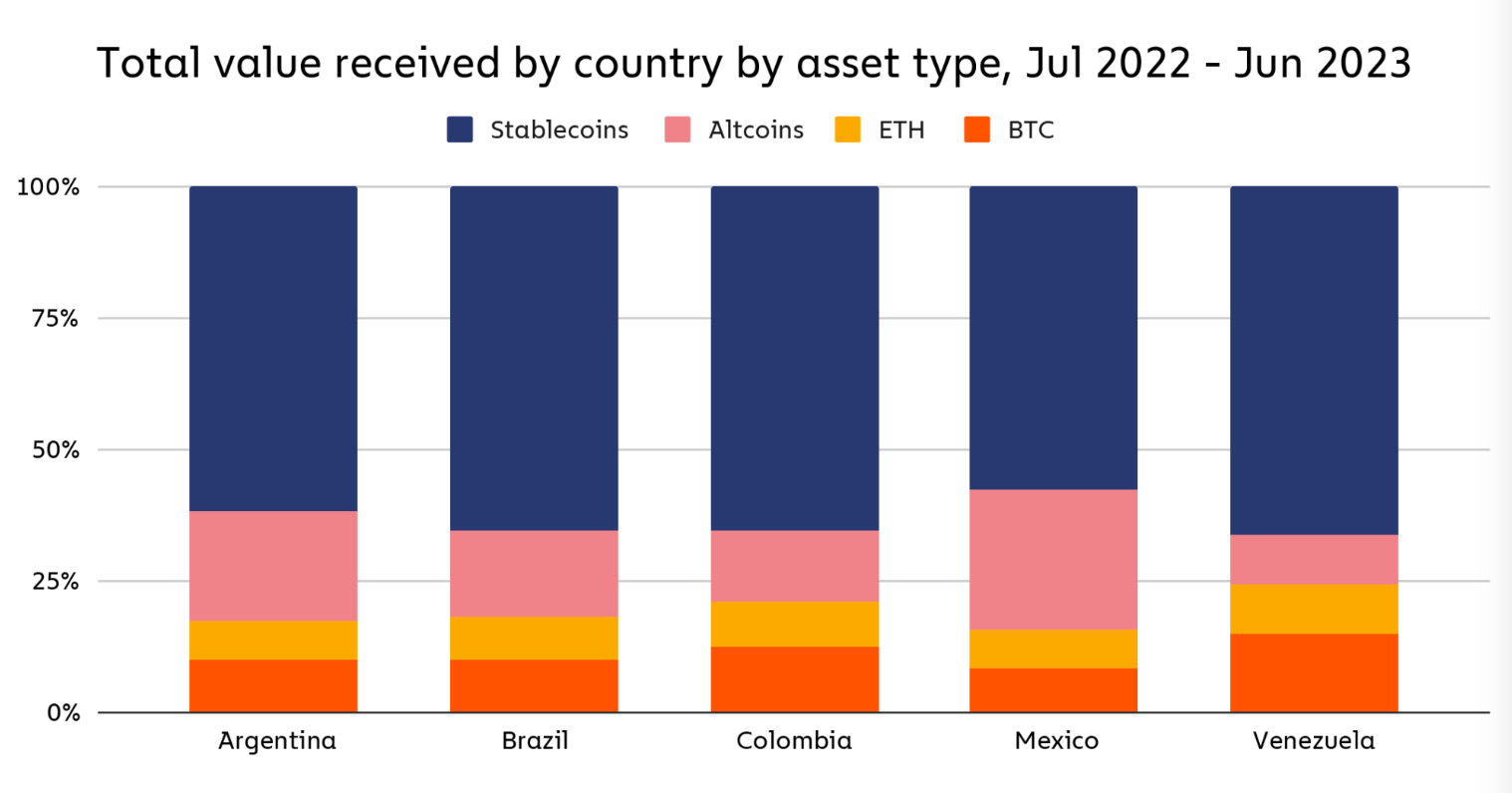

Отчет Chainalysis за 2023 год показал, что стейблкоины были наиболее широко передаваемым цифровым активом в странах Латинской Америки. Источник: Chainalysis

Высокая непропорциональность волатильности влияет на жителей развивающихся стран, которые обратились к стейблкоинам доллара США в качестве цифрового хранилища ценности из-за их низких комиссий за транзакции и относительной стабильности по сравнению с другими криптовалютами.

Во время недавнего саммита по криптовалютам в Белом доме 7 марта министр финансов США Скотт Бессент объявил, что США будут использовать стейблкоины для обеспечения гегемонии доллара США и защиты его статуса мировой резервной валюты.