引言

dappOS 致力于构建完整的Web3意图层,帮助用户简化操作并获得机构级别的执行效率。Web3意图层的三大核心构成元素是:操作、资产、交易。此前,dappOS 已经推出了意图操作系统(IntentOS)、意图资产(Intent Asset),实现了操作和资产的意图化。基于这些产品技术积累,dappOS 现在推出了意图交易所 IntentEX,进一步帮助用户实现交易意图化,完善 dappOS 意图层生态的关键组成部分。

IntentEX 的核心优势,在于让普通用户直接享受到机构级别的流动性资源,并且交易执行速度更快、费用更低,体验接近 CEX 级别。

一、背景

当前市场处于新资产和 MEME 的热潮之中,用户有旺盛的链上交易需求。然而,许多现有的链上交易所难以为用户提供足够的流动性,执行速度较慢,且手续费较高。这些问题严重影响了用户体验。而出现这些问题的核心原因,是一个资产的交易流动性往往被分散到了各个交易所之中,用户无法在一个交易所内享受到全市场关于该资产的流动性。

dappOS 意图交易所 intentEX(https://portal.dappos.com/trade)的出现,解决了这些流动性、交易成本、交易效率的问题,真正帮助用户实现了交易意图化。

二、intentEX 的原理

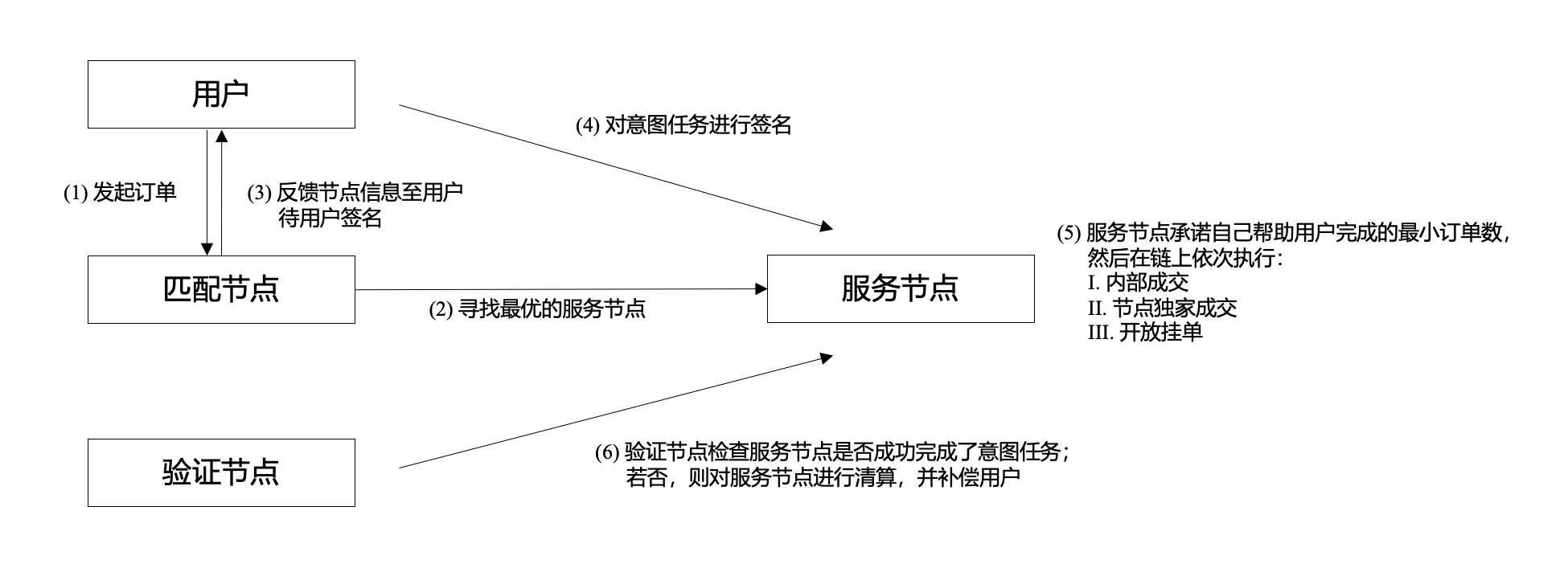

intentEX 的核心设计创新,是在传统订单簿交易所的基础之上,额外将用户的限价订单作为一种意图任务(intent task)委托给 dappOS 意图执行网络中的节点执行,并允许节点在任意链上完成交易。这一设计不仅能充分发挥专业机构的交易流动性优势,让 intentEX 中的代币实质上拥有了优于全部 CEX、DEX 中的流动性,而且给了用户更快的成交速度和更低的执行手续费。

2.1 发布意图任务

当用户在 intentEX 上发出限价订单时,相当于在 dappOS 意图执行网络中发布了一个意图任务。网络中的匹配节点将会把该意图任务匹配给综合竞争力最强的服务节点。匹配节点在选择服务节点的时候会综合考虑各种因素,如:节点的保证金、执行成本、执行速度、每偏离盘口一定价格节点愿意接多少单等。

用户完成签名以后,确认接到这个意图任务的服务节点会按照自身的情况,承诺一个自己保证用户能够成功成交的订单数额。由于 dappOS 意图执行网络的OMS 机制约束,服务节点一旦签名完成确认了独家成交数量,如果最终未兑现节点将会被清算,因此通常到这一阶段用户既可认为服务节点承诺的订单部分已经完成,无须等待最终链上确认。当用户报价在盘口附近时,由于服务节点会倾向于承诺成交所有的订单,用户订单成交的速度可以高于公链本身的区块速度。

2.2 链上订单处理

在完成承诺后,服务节点将在系统约束下在链上按照以下三个步骤完成订单处理:

- 内部成交(Internal Fill):如果 intentEX 订单簿中有匹配的挂单,系统会直接撮合成交。未能在此阶段成交的部分订单,将进入下一阶段。

- 节点独家成交(Node Exclusive Fill):剩余的订单,在一定的时间内这个服务节点将拥有独家成交的权利。如果服务节点承诺用户成交的订单数量在内部成交阶段并没有完成,服务节点需要自行成交,否则将面临 dappOS 网络的清算。服务节点也可以在这一阶段额外成交比自己承诺的更多的订单。

- 开放挂单(Open Order):剩余的订单,将会被挂到 intentEX 的盘口,供其他用户交易。

如果一个服务节点的执行速度过慢、或者承诺帮助用户成交的订单数较少,则其在匹配节点的竞争力权重就会被降低,从而难以接到更多的订单。这个机制有利于服务节点倾向于承诺帮助用户成交更多的订单,并且更快的完成交易。

2.3 一个具体案例

为了便于读者理解,这里举一个具体场景作为案例 —— 假设现在 intentEX 中的$A 代币的卖盘盘口的卖一总额有 990 U,价格为 9.9 U;卖二总额有 1010 U,价格为 10.1 U。

这个时候用户发起了 300 个 10 U 的限价买单,那么这个买单将作为意图任务发布到 dappOS 意图执行网络之中,网络中的匹配节点将把这个任务分配给当前最优的服务节点。

假设一个服务节点成功竞争到了这个意图任务,那它需要承诺一个自己帮助用户成交的最小订单数(比如 250 个$A 买单)。这个承诺的具体数额一般和节点的策略、以及当前所有其它交易市场中$A 代币的盘口深度有关,比如这个节点愿意承诺帮助用户至少成交 250 个买单,可能是因为:intentEX 盘口当前本身就有 100 个能立即成交的卖单;并且它在观察了所有其它的 DEX、CEX 以后,找到了 150 个计入相关手续费后成本低于 10 U 的$A 代币。

从用户的视角来看,它的 300 个限价买单中的 250 个,在服务节点向网络提交承诺的时候就已经成交完毕了,这个成交速度是快于公链本身的出块速度的。在这个例子中,$A 的盘口深度并不大,但在更多情况下,当盘口深度足够的时候,节点就会承诺帮助用户成交所有盘口附近的订单,这样用户就能发现自己所有的订单的能够立即得到成交。

接下来服务节点将按照以下流程进行交易执行:

1.内部成交(Internal Fill)

用户的 300 个 10 U 的限价买单中的 100 个将会和 intentEX 现有盘口的 100 个 9.9 U 卖单匹配,并以 9.9 U 的价格直接成交。

2.节点独家成交(Node Exclusive Fill)

由于节点做出了帮助用户至少成交 250 个订单的承诺,在这一阶段它至少需要帮助用户成交剩余的 150 个订单,否则将面临清算。

这里就体现出了 intentEX 的优势: 相比于让用户剩余未执行的订单挂在盘口、等待其它的做市商来进行套利,意图执行网络中的专业服务节点直接承担了这一角色。这一方面让用户实质上拥有了全市场有关$A 代币的流动性,另一方面也让用户的订单有了更快的成交速度。

3.开放挂单(Open Order)

最后的 50 个 10 U 的限价买单如果匹配到的服务节点不愿意成交,就会出现在 intentEX 的$A 代币的买盘盘口中。

一般来说,这种情况只会在用户的挂单价格离盘口较远、或者相关代币在所有交易市场的流动性都相对不充足的时候才会出现。

三、intentEX 的核心优势

1. 机构级的全市场流动性

dappOS 的专业服务节点能够在全市场的 CEX 和 DEX 中实时观察并匹配用户订单。因此 intentEX 内的代币交易拥有全市场级别的流动性。

相比 router 等纯链上询价的设计,intentEX 同时结合了链上和链下的优质流动性,带来了机构级的流动性捕捉能力。这样,用户的每个订单都能迅速接入最优价格源,实现更高的成交率和更快速的交易执行,享受到全市场的流动性。

相比于其它意图架构的设计,dappOS 独特的 OMS 机制能够让节点接任务的时候不占用资金成本(只要能够确保完成意图任务,资金可以多业务同步使用,不需要向充当 LP 一样专门质押资金)以及应对抢单的成本,这降低了节点的综合运行成本,让整个系统的运行效率更高。

2. 执行速度快

intentEX 利用其全平台的流动性,通过对盘口价格的快速匹配,为用户提供比常规链上交易更快的成交速度。intentEX 的执行效率得益于 dappOS 意图执行网络的专业服务节点,在一般情况下从用户签名完成开始可以在 500 毫秒内完成签名确认,甚至高于公链出块的速度。这大幅降低了交易等待时间,使用户能够更快完成交易。

相比于其它的意图架构设计,这种优于公链的交易速度和流畅的体验,为用户带来了更加接近中心化交易所的便捷感受。

3. 交易手续费低

intentEX 依托于 dappOS 专业的服务节点网络,极大地优化了交易手续费,成本低至 0.1% ,远低于多数链上交易所的费率。这使得 intentEX 成为用户在链上交易时更加经济的选择。

4. 去中心化与透明性

intentEX 所有交易均在链上公开记录,保障了系统的透明性和可信性。dappOS 意图执行网络中的去中心化机制确保订单的可靠执行,即使某个服务节点出现故障,其他节点也能无缝衔接,持续确保交易成功。通过这种去中心化结构,intentEX 为用户提供了更为稳定且无依赖单点服务器稳定性的交易体验。

四、intentEX 与 dappOS 生态系统

意图交易所 IntentEX 是 dappOS 生态系统中的重要组成部分,是 dappOS 在实现了操作意图化、资产意图化之后,为帮助用户实现交易意图化所推出的产品。

前文中已经详细阐释了 intentEX 基于 dappOS 意图执行网络的详细具体实现。关于 dappOS 意图执行网络的详细原理,请参考:https://dappos.gitbook.io/docs/dappos/how-dappos-works

除此之外,intentEX 中交易所使用到的 USDT、BTC、ETH 实际上是 dappOS 的意图资产,即 intentUSD、intentBTC、intentETH。这样用户即使是在持有这些主流资产不交易的时候,也可以享受到利息收益,并且完全不影响到用户立即使用这些主流资产进行交易。关于 dappOS 意图资产的详细原理,请参考:https://dappos.gitbook.io/docs/dappos/intent-task-frameworks/intent-assets