过去一周,市场在持续下跌后,周一迎来一轮抛售高潮。那么,现在是否是抄底的好机会呢?虽然美国降息似乎近在咫尺,但一直未能兑现。叠加失业突增触发萨姆法则,市场正在经受严峻考验。周末,巴菲特对苹果的抛售以及中东局势的紧张,成为压倒市场的最后一根稻草。亚洲早盘出现多年未见的抛盘,市场情绪尚未完全平稳,投资者应谨慎对待这一波下跌行情。

宏观环境

1)日元快速上涨,套利交易崩盘

日元套利交易是一种利用日元在不同市场或金融工具之间价格差异进行套利的策略。常见形式包括利率套利、货币套利、期货套利和跨市场套利。投资者通过借入低利率的日元资金,投资于高收益资产,或利用外汇市场和期货市场的价格差异进行买卖操作,从中获取利润。这种交易通常需要快速决策和执行,以在价格差异出现的瞬间获利。

图 1 :美元对日元

来源:TradingView

许多交易员借入日元做多美元资产,目前出现的天量反转可能形成强大的反身性。估计套息交易的资金量在 4 万亿美元左右,目前市场继续外部注入流动性。

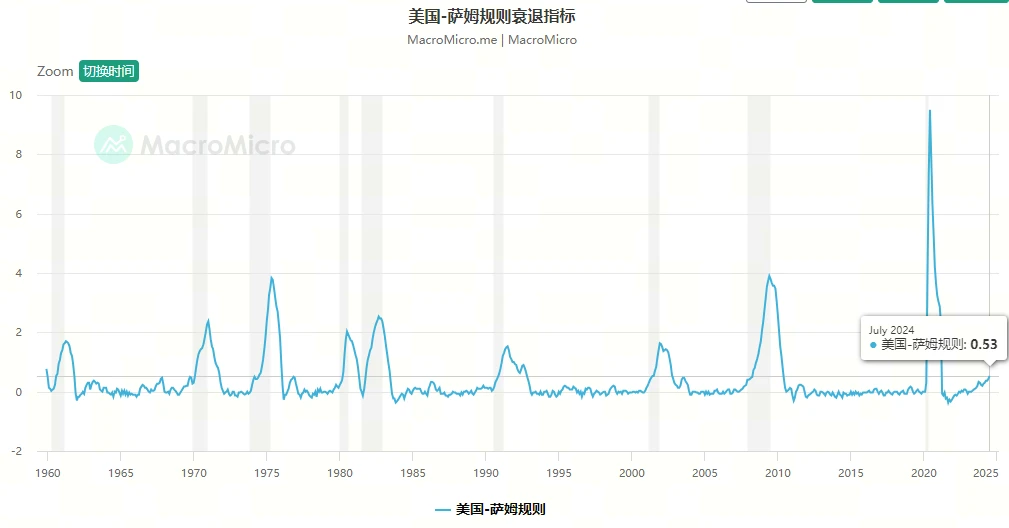

2)市场开始恐慌,联储有望入场干预

近期市场受美国经济走软影响,比特币(BTC)价格下滑,山寨币市场也随之下行。非农最新失业率计算,美国失业率从今年以来的低点飙升了 0.6% ,失业率连续超预期激增数月后,终于触发了基于失业率预测衰退的“萨姆规则”。

图 2 :萨姆规则衰退指标

来源:MacroMicro

需要密切关注美联储的下一步行动。网传美联储将于周一召开紧急会议,讨论日本股市股灾后的利率问题。

图 3 :恐惧贪婪指数

来源:Coinglass

这波抛售潮似乎源于一个“时间触发”的算法程序,该程序在过去 7 个交易日内每天美国东部时间上午 10 点(美国市场开盘后)触发卖单。这个算法在周末仍在运行,可能导致高频交易(HFT)驱动的抛售和做空潮,迫使杠杆多头投资者认输。

图 4 :爆仓热力图( 24 小时)

来源:Coinglass 官网

在杠杆多头遭遇“爆金币”阻击后,市场可能会在短期内收拾筹码,进入上涨状态。

优质赛道

在当前市场环境下,投资者应谨慎选择投资标的,并密切关注宏观环境和市场动态,以便在适当时机做出明智的投资决策。

1)链上黄金(XAUT)

基本面:实物黄金抵押

Tether Gold(XAUt)是一种数字资产,代表着在金库中持有的实物黄金所有权。

价值稳定

XAUt 的价值与实际黄金挂钩,每枚 XAUt 代表一定数量的黄金。这使得 XAUt 在市场恐慌中表现出色。

透明度和安全性

XAUt 采用区块链技术,确保交易透明和安全。每笔交易都记录在区块链上,可追溯和验证,降低潜在的欺诈和风险。

便捷性

XAUt 可以在全球范围内快速、低成本地交易。相比传统的黄金交易,XAUt 交易速度更快,并且不受地理和时间限制。

2)波场(TRX)

交易量超越以太坊

根据 X Lookonchain 上的区块链分析,Tron 网络上的交易数量已超过 80 亿。这是以太坊 (ETH) 的四倍。

盈利稳定

TRX 预计今年能达到 7-8 亿美元的整体协议收入,每年协议通缩率达到 6% ,在不稳定的熊市中,TRX 将是更稳定的代币。

总结

周一的抛售导致加密市场避险情绪飙升,考虑到日元套利交易的崩盘和市场恐慌加剧可能导致的高频交易抛售潮。本次的链上回稳可能将取决于美联储的强力干预与市场情绪的修复。我们认为在高风险的市场中,持有或者买入链上黄金(XAUt)和波场(TRX)作为优质赛道将能够较好的规避市场进一步下挫的风险。