原文作者:IGNAS

原文编译:深潮 TechFlow

导读

2024 年,再质押(Restaking)领域呈现爆炸式增长,成为了 DeFi 领域的一大趋势。本文将对 EigenLayer 的再质押机制、AVS 的应用案例等进行解析。此外,文章还将介绍 AVS 的不同类型,如 Ethos、AltLayer、Espresso、Omni 等,分析它们的特点和作用。

正文

记住我的话:再质押是 2024 年增长最快的领域。再质押是第 9 大 DeFi 类别,仅 EigenLayer 就有 20 亿美元的 TVL。

不要忘记排在第 13 位的"流动性再质押",其规模已达到 10 亿美元。

随着第一个主动验证服务(AVS)代币 ALT 的推出,以及 EigenLayer 在 2 月 5 日开放存款,现在是时候追踪这一领域的所有动态了。

我将简要解释 EigenLayer 的再质押,将介绍通过再质押启用的 AVS 的新兴用例。

EigenLayer 将于 2 月 5 日开放存款。以下是你需要知道的内容。

他们已经修改了他们的积分系统,通过将单笔存款和 LST/LRT 分配上限限制在 33% 来鼓励权力下放和去中心化。目前还没有任何单一的 LST/LRT 达到 33 %的上限。

Swell 和 EtherFi 通过原生代币空投提供双倍积分。我的方法是在不同的 LST/LRT 中进行多元化,以实现平衡的积分累积和风险。

关于 LRT 竞争,我正在对几个项目进行对冲投注:

EtherFi:这是领先的 LRT,拥有 51% 的 LRT 市场份额。使用我的推荐链接,每 ETH 可额外获得 1000 个 EtherFi 积分,并在合作 DeFi 协议中获得双倍积分。

Kelp DAO:通过再质押 stETH 或 ETHx 赚取 Eigenlayer 积分和 KelpDAO 里程。

Renzo:与 EtherFi 一样,使用 Eigenpods 进行原生 ETH 再质押。

Swell:你可以存入 ETH 以获得 swETH LST,并在 EigenLayer 上再质押。或者直接存入 rswETH LRT。

Eigenpie:Eigenpie 已有 1 亿美元的 TVL,支持 6 个 LST,并在前两周提供双倍积分。这这些积分用于 10% EGP 代币空投,并以 300 万美元 FDV 获得 60% EGP 代币 IDO,用来激励早期用户参与。

再质押:ELI 5

早在 2023 年 9 月,我就详细介绍了关于再质押和押注 Liquid Restaked 代币(LRT)。但从那时起,情况已经发生了很大变化。现在在主网上有多个 LRT 协议,随着 AltLayer 推出代币,事情正在升温。

许多人仍然对再质押感到困惑,经常把它复杂化。

简单来说,它让你为各种主动验证服务(AVS)质押(担保)你的 ETH,以增强所选协议的安全性。这包括桥接器、预言机和侧链等服务,以及即将出现的更多创新概念。

例如,Optimism 和 Arbitrum 可以绕过 7 天的欺诈证明窗口,实现即时提现,只要有足够的经济安全(在这种情况下是 ETH)支持提现即可。

这些 "保险(insured bridges) "可保证在验证器出现错误时进行充分的重新分配。你将 ETH 再质押到"保险桥 AVS",那么在验证器出错的情况下,有可能会损失一些 ETH。(从目前的情况来看,如果智能合约出现漏洞,"保险桥 "并不能保护你的利益)。

你可以直接重新再质押 ETH,也可以通过流动性质押代币如 stETH、rETH、cbETH 等进行再质押。EigenLayer 这一轮增加了 LST sfrxETH、mETH 和 LsETH。

再质押的好处:

多协议奖励:使用相同的 ETH 从多个协议中赚取收益

提升安全性:利用以太坊的安全性来实现新协议

开发者自由:无需建立新的安全层,从而节省开发人员的时间和资源

再质押的风险:

削减风险:由于恶意活动,损失质押的 ETH 的风险增加

中心化风险:如果过多的质押者转移到 EigenLayer,可能对以太坊构成系统性风险

智能合约风险:像在 DeFi 中的其他地方一样

我相信目前的风险是有限的,因为 Eigenlayer 仍在第二阶段测试网,且未启用无需许可的 AVS 部署。我同意 ChainLinkGod 的看法,尽管风险大多会被忽视,但至少我们会在 2025 年之前都会觉得不错。

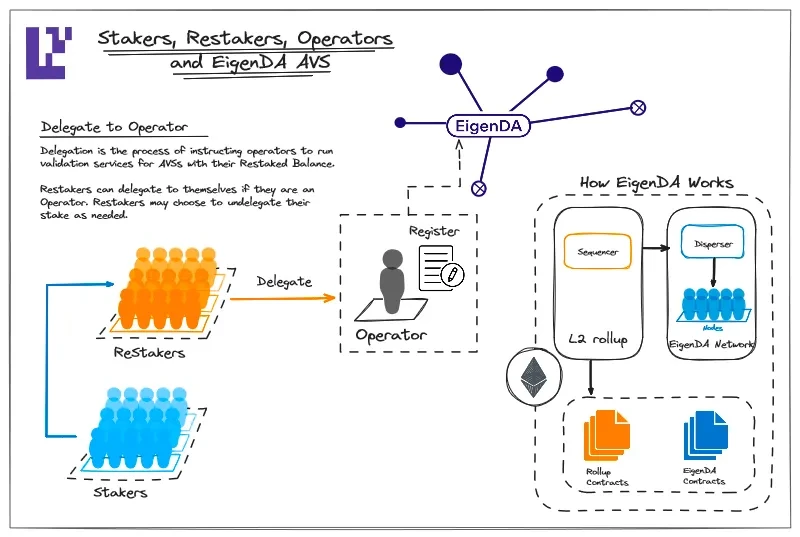

在当前的第二阶段测试网上,像你这样的再质押者可以委托给运营商。这些运营商验证 AVS。所以,你不是直接再质押到 AVS 上!

EigenDA(数据可用性)是第二阶段的第一个 AVS。Rollup 可以集成它来增加吞吐量。第二阶段主网将在 2024 年上半年启动,第三阶段将在 2024 年晚些时候启动,届时将有更多 AVS。

你实际上可以在 Goerli 测试网上查看运营商的委托是如何工作的。按照此处的指南获取一些 goerliETH 并兑换为 stETH。然后前往 Eigenlayer 测试网页面并存入 stETH。然后选择运行 EigenDA AVS 的运营商。

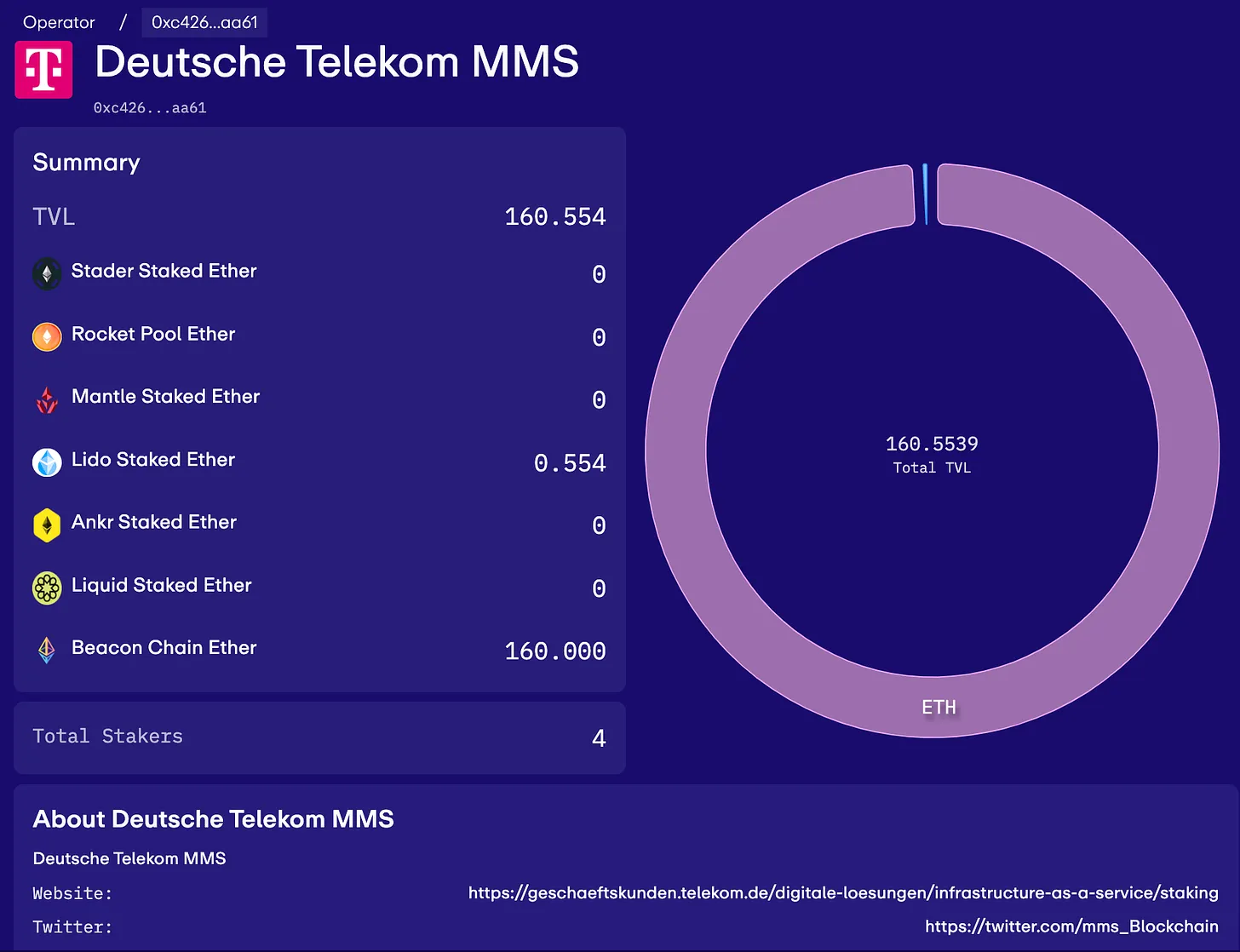

有趣的是,在众多运营商中,有一家脱颖而出:Deutsche Telekom。Telekom 似乎将使用 Eigenlayer 进行质押服务。

无论如何,你准备好在主网上自己手动选择 AVS 和运营商了吗?考虑到高昂的 Gas 费用?然后从 AVS 那里领取奖励?然后出售奖励以获得更多的 ETH 进行复利?如果你不是特别富有的话,会认为这里的 Gas 费用将会很高。

我相信你可以猜到我接下来要说什么:流动性再质押代币(LRT)。但更多关于 LRT 的内容将在下一篇文章中讨论。现在,让我们关注 AVS 将会空投给我们的新代币的用例。

首个 AVS 是 EigenDA,但我不会详细介绍,因为我怀疑它会有单独的代币(这是一个用于 Rollup 的数据可用性层,以节省数据存储费用)。

主动验证服务

不要被名字迷惑。AVS 是功能完备的协议,它使用再质押的 ETH 来增强其功能。我上面提到了“保险桥”,但 AVS 的范围和影响很快就会变得更加明显。

我将在这篇博客中用非常简单的语言介绍 7 个 AVS。因为如果我们将 ETH 投资到 Restake 生态系统中,我们需要了解 AVS 。

Ethos:将 ETH 安全带到 Cosmos

Ethos 将以太坊的经济安全性和流动性引入 Cosmos。

所谓的 Cosmos Consumer 链通常发行其原生质押代币来保护网络。然而,这引入了更多的复杂性和通货膨胀代币经济学。虽然 Cosmos ATOM 质押者提供了一个链间安全(ICS)解决方案,但以太坊生态系统通过 Ethos 和再质押,现在正在扩展到 Cosmos 自己的领域。

再加上 Dymension、ATOM 分叉、以及现在 Ethos 的推出,ATOM 似乎承受了很大的压力。

Ethos 的灵感来自于 Mesh Security(允许一条链的质押代币在另一条链上使用),从而在不需要额外节点的情况下增强经济安全性。更多详情请点击此处查看 Ethos 博客文章。

哪种安全解决方案会胜出取决于其采用情况。Ethos 正势头强劲地启动。

Sommelier 是是第一个合作伙伴,这是一家自动化收益库提供商,TVL 为 6000 万美元。据我所知,更多的 Consumer Chain 即将推出。

这种结构的优点在于 ETHOS 可能会收到合作伙伴链代币空投(和收入)。与此同时,ETHOS 代币本身将被空投给 Eigenlayer 上 ETH 的再质押者,作为我们收获 EIGEN 代币的一部分。

你需要做的就是再质押 ETH,并领取空投。

AltLayer:再质押的 Rollup

我在之前的文章中刚刚介绍了 AltLayer,所以这篇文章我不会过多深入它的功能。可以点击这里进行查看。

但你需要知道的是,AltLayer 引入了三个 AVS,为 Rollup 带来了

快速的最终确定性

去中心化的排序

去中心化的验证

ALT 代币经济模型很有趣,因为 ALT 是必须与再质押的 ETH 一起质押,以保护这三个 AVS。

如果你经历过 2020 年 DeFi Summer,你会理解它可能产生的庞氏效应。

目前,社区只有 3% 的总供应量被空投,但未来计划有更多的空投。初始流通供应量为 11% 。43 亿美元的 FDV(在撰写本文时)是否证明了一项几周前还没有人听说过的协议的合理性?

不太确定,但这让我对整个再质押生态系统更加看好。

此外,我怀疑 AltLayer 为再质押者保留了流动性挖矿奖励。随着更多 AVS 的推出,各种服务将竞争吸引宝贵的 ETH 存款。毕竟,没有任何存入的 ETH 的 AVS 是没有价值的。

Espresso:去中心化排序器

Espresso 专注于 Layer 2 的去中心化排序器。如你所知,L2因排序器的中心化而受到许多指责。关于 Espresso 如何利用其 HotShot 共识来实现这一目标,有一个很好的可视化展示,请点击这里进入他们的网站进行查看。

AltLayer 实际上集成了 Espresso,因此开发人员可以选择使用 AltLayer 的去中心化验证解决方案和/或 Espresso 排序器在 AltLayer 堆栈上部署。

Omni:连接所有 Rollup 的区块链

问题:L2降低了交易成本,但导致了生态系统的碎片化。这使得开发者很难接触到广泛的受众,使用户体验变得复杂,并分散了流动性。

桥接也成为必须,但桥接通常会发行包装代币(wrapped token),存在风险。如果桥接器被黑客攻击,就没有足够的底层资产来支持桥接的包装代币。结果,包装代币就会失去挂钩。

解决方案:Omni

Omni 是一个“通过再质押保护的L1区块链”,旨在将以太坊的所有 rollup 统一在一个屋檐下。

Omni 引入了一个“统一的全局状态层”,通过 EigenLayer 的再质押来保证安全。这一层将应用程序的跨域管理集中在一个屋檐下。

使用案例包括:

跨 rollup 保证金账户和杠杆交易:在一个域上发布保证金,并在另一个域上使用该保证金进行交易

跨 rollup NFT 铸造

跨 rollup 借贷:在一个域上存入抵押品,并在另一个域上借用抵押品

还有很多,但这听起来很熟悉吗?这就是 LayerZero 所做的。

LayerZero 的跨链消息传递使得 Omnichain 可替代代币(OFT)成为可能,而不是包装代币。Manta 的 STONE 代币是一种 ETH OFT,LayerZero 发行了 Lido 的 wstETH OFT。

但如果 LayerZero 消息传递系统出现漏洞怎么办?好吧,Omni 通过再质押的 ETH 来保护它,如果验证者行为不端,这些 ETH 将被没收。

考虑一个经常投机的 degen,他想在 Arbitrum 上使用他的 ETH 来在 Optimism 上获得 USDC 贷款。Degen 在 Arbitrum 上的交易由 Omni 验证者监控,他们确保数据传输到 Optimism 的完整性。这些验证者通过奖励来激励,并因为错误报告而失去他们质押的 ETH 的风险而受到威慑。

LayerZero 可能会使用他们的代币质押来保护跨消息传递安全,但如果 LayerZero 合约出现问题,代币就会下跌,那种安全性就没有用了。ETH 是系统外部更难保护网络的资产。

LayerZero 的竞争正在升温

Injective 与 Omni 合作,使$INJ 成为 Omni 开放流动性网络上的第一个资产。Omni 发行 xERC 20 INJ 代币,从而将 INJ 带入以太坊 rollup 生态系统。

Omni 得到了如 Pantera Capital、Two Sigma Ventures 和 Jump Crypto 等知名投资者 1800 万美元的支持。所以,我猜它会做得很好。

Hyperlane:与 Omni 类似,但似乎更好

你认为 Omni 在连接以太坊 Rollup 方面很牛?但 Hyperlane 似乎更牛。因为 Hyperlane 的目标是连接所有L1和L2。

使用 Hyperlane,开发者可以构建跨链应用程序 ,跨越多个区块链的应用程序,使用跨链消息传递,通过其模块化安全堆栈进行保护,该堆栈包括跨链安全模块和再质押的 ETH。

从文档中判断,Hyperlane 将支持以太坊L2、Cosmos 生态系统链、Solana、基于 Move 的链等。

Hyperlane 无需许可的互操作性使其与众不同,因为 Rollup 可以自己连接到 Hyperlane,而无需繁琐的治理批准等等。他们对此感到非常自豪,正如您从下面的推文中看到的那样。然而,LayerZero v2 似乎也允许无许可的部署。

不幸的是,我目前找不到 Omni 或 Hyperlane 的代币信息。

The Blockless:在使用 dApp 时为其提供动力

在普通的 dApp 中,我们不能直接贡献计算能力,应用受限于特定的L1或L2的能力,如延迟、交易速度、Gas 费等。

因此,Blockless 采用了网络中立的应用程序(nnApp),允许用户只需使用它们即可为应用程序提供支持。它使用了“嵌套节点(nestled nodes)”,其中每个用户的设备充当一个节点,为网络贡献其资源。这意味着应用程序的计算能力随着用户群的增长而扩展,这是传统模型的一个重大转变。

简而言之,你在使用应用的同时运行一个节点。

Blockless 登陆页面

例如,一些 dApp 可能选择将治理保留在以太坊上,将数据可用性工作负载保留在 Celestia 或 EigenLayer 上。但对于机器学习、人工智能接口和游戏等用例的密集型计算工作将在更快、更高效的链下环境中执行。

这导致这些应用程序的计算支持直接随着用户数量的增长而扩展,更多的用户意味着更多社区提供的计算能力。

这让我我想到了 Grass,这是 Solana 上的一款应用程序,可以出售闲置的互联网带宽来训练人工智能,尽管它不是 Blockless 的一部分。

Blockless 使用权益证明来保护其网络,因此代币不仅仅是一个 Meme。

至于再质押,Blockless 将为 EigenLayer 上构建的应用提供其网络,以最大限度地减少意外削减。

其他

你可以在 Eigenlayer 网站上查看所有 AVS 的完整列表。值得一提的是:

Lagrange :LayerZero、Omni 和 Hyperlane 的另一个竞争对手,其跨链基础设施能够在所有主要区块链上创建通用状态证明。最近从 1kx 和其他公司筹集了 400 万美元的种子资金。

Drosera: “事件响应协议(incident response protocol)”,用于控制漏洞。当黑客攻击发生时,Drosera 的陷阱会检测到它并采取行动来减轻攻击。

Witness Chain:使用再质押来进行勤奋证明(Proof of Diligence),并确保 rollup 的安全,并使用位置证明(Proof of Location)建立物理节点去中心化。