简而言之 - “委员会认为,在对通胀能够持续向 2% 迈进更有信心之前,不宜降低利率目标区间” 且 [Powell] “认为美联储不太可能在 3 月份启动降息”。

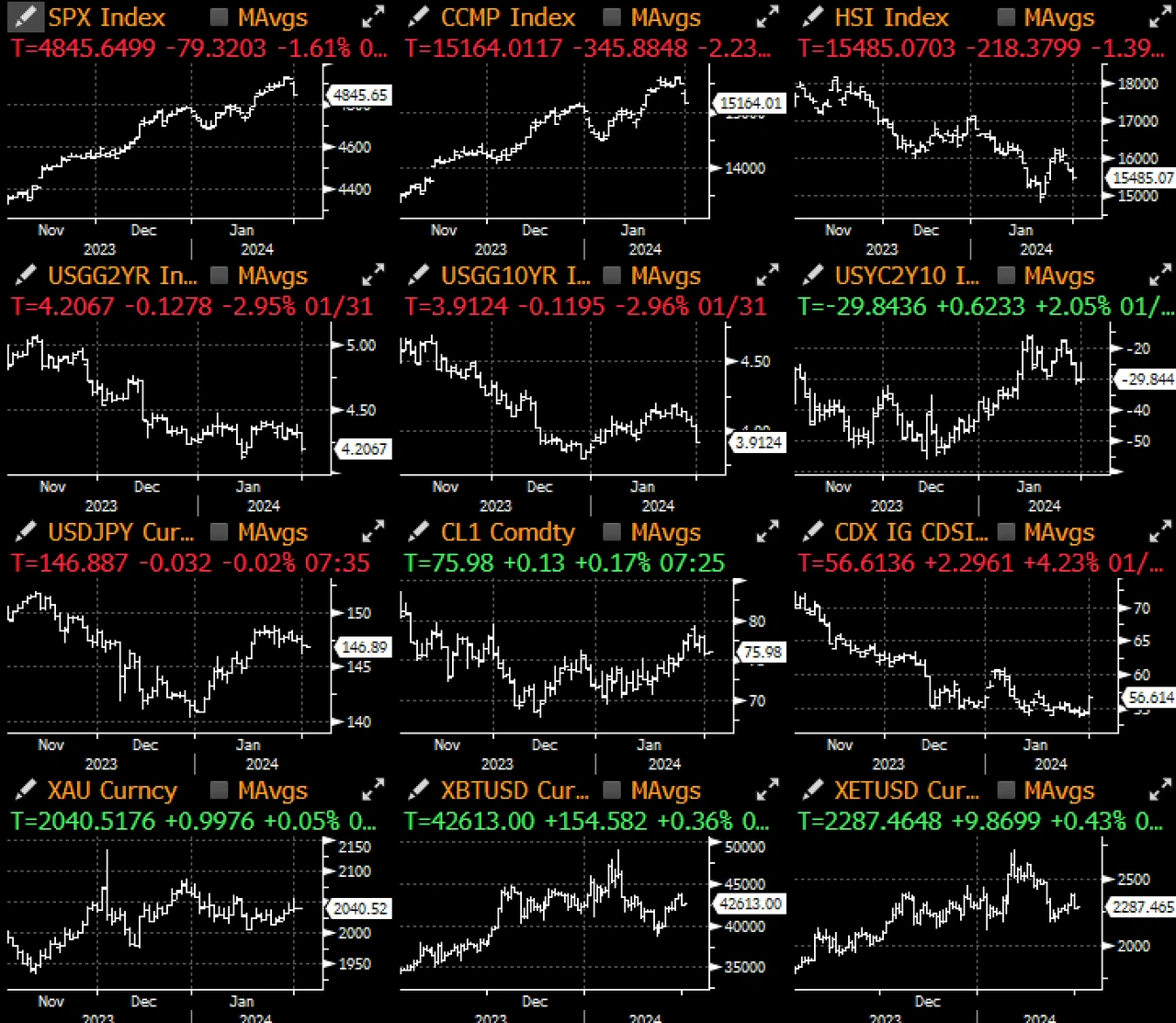

昨天的 FOMC 会议和市场价格走势可以用一句话来概括 - 先不要指望 3 月份会降息。尽管美联储按预期从官方声明中移除了加息倾向,但市场对于这种明确的鹰派反制评论仍是措手不及,虽然“更大的信心”的具体含义尚不明确;无论如何,这被视为美联储对市场日益增长的宽松政策预期的直接否定,导致 OIS 利率从低点跃升 10 个基点(吐回稍早疲软的 ADP 和劳工成本指数带来的涨幅),市场预期降息的可能性也降至 30% 左右。

在 2: 30 的记者会上,Powell 最初试图通过以下评论“平衡”鹰派声明:

政策利率“已进入限制性区域”。

“今年某个时候放松政策限制”是适当的。

FOMC 成员们对于通胀的缓解“越来越有信心,但我们希望获得更大的信心”。

“我们不是在寻求更好的数据,而是希望看到更好的数据能持续”。

在通胀方面,Powell 指出,“通胀数据的构成不如总体通胀水平重要”,这是对商品和服务通胀之间持续存在分歧的回应。

然而在记者会问答环节的尾声,主席以下的评论彻底毁灭了鸽派的希望:

“本次会议没有降息的提议”。

“实现软著陆仍有很长的路要走”。

[Powell]“认为美联储不太可能在三月降息”。

最后的评论起到了致命一击的作用, 2 年期美债收益率上升约 8 个基点,股市当天暴跌约 1.5% ,看来真正的 2024 年才刚开始。

除了美联储会议之外,还有其他值得关注的消息。首先,备受期待的债券发行计划完全符合市场预期,对债券价格起到了缓解作用,尽管财政部连续第三次提高季度发行规模,但官员表示这将是 2024 年最后一次增发,且供应规模(下周 3 年期/10 年期/30 年期共 1, 210 亿美元)完全符合去年 11 月所设定的节奏;此外,财政部还确认将在 5 月的再融资公告中宣布新回购计划的开始日期,该计划旨在协助现金管理和改善非当期国债的流动性。

关于债券发行的期限结构,财政部表示,预计至少将目前的国库券拍卖规模维持到第一季末,然后在下一季小幅减少。无论如何,随著财政部继续牺牲一定程度的融资谨慎性,为长债的供应提供缓解,国库券在总发行量中所占的份额将保持在建议的范围之上。

在其他消息方面,ADP 疲软(+ 10.7 万 vs 上个月 + 15.8 万)、劳工成本指数(2021 年以来最慢的年化增速)、芝加哥 PMI(46 vs 47.2)以及 New York Community Bancorp (一个纽约区域银行)因大幅贷款减值而宣布削减股息,导致股价暴跌 40% 。

该银行去年收购了 Signature Bank 的一部分,由于去年第四季度拖欠 30 天以上的贷款猛增 48% ,加上预计商业房地产市场将进一步疲软,因此提高了贷款损失准备金;本季坏帐冲销总额飙升至 1.85 亿美元,超过了过去 10 年减值损失的总和,使得该银行第四季度的净亏损达到了 2.52 亿美元,远低于分析师预期的 2.06 亿美元的收益,并宣布削减约 70% 的股息,以保存现金。

尽管许多信贷分析师认为这是一个独立的、特定股票的事件,但去年 3 月的阴影在许多人的脑海中挥之不去,而即将在 3 月份退场的 BTFP 计划无疑无助于缓解担忧。美国 KBW 银行指数当天一度下跌 5.5% ,最后收盘跌幅收窄至 3% 左右。

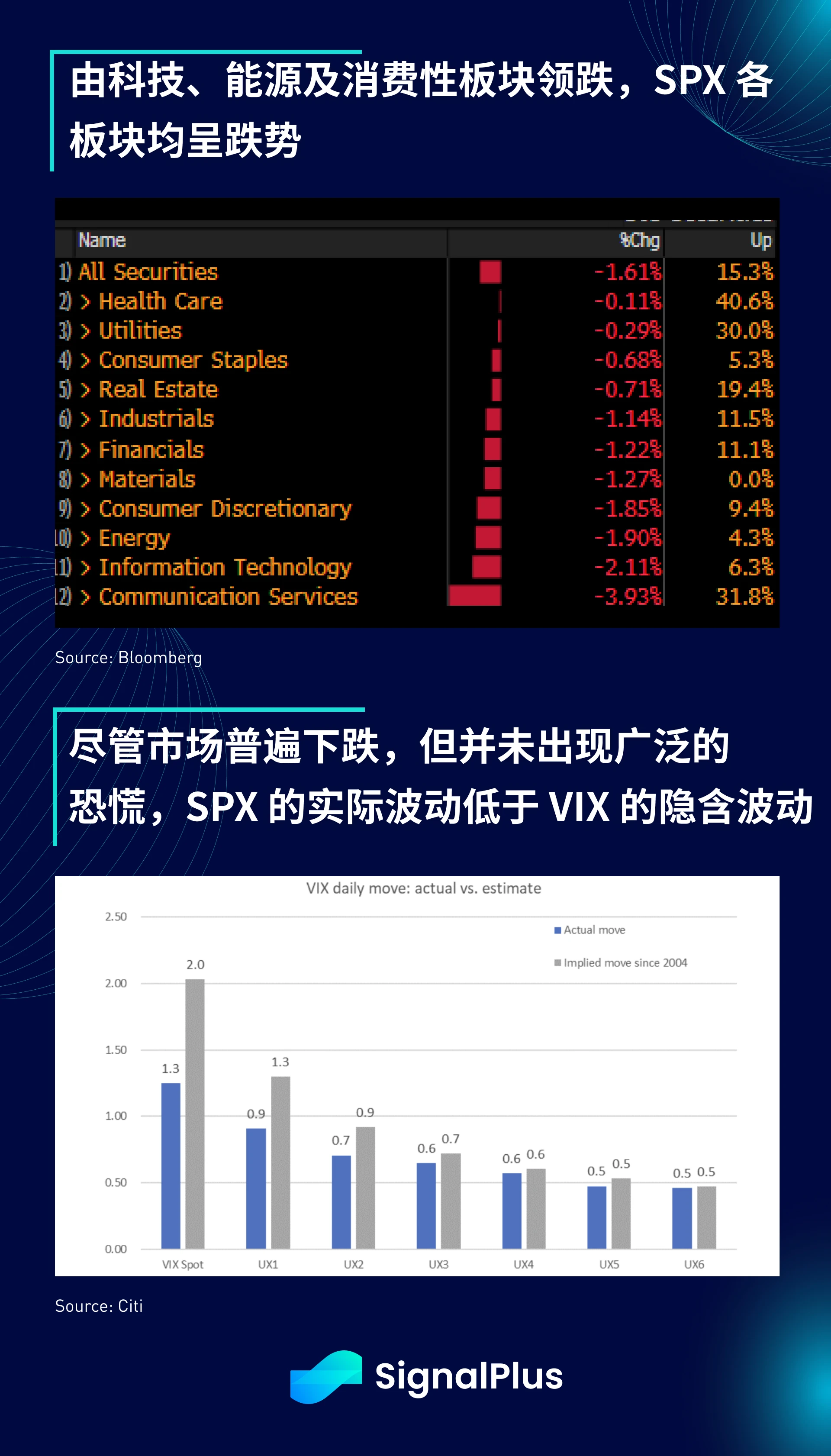

在股市方面,除了鹰派美联储和 NYCB 引发的恐慌之外,各大企业财报普遍令人失望。AMD (-2.6% )、Samsung (-2% )、Google (-7% )、Microsoft (-2.5% ) 和 Disney (-2.5% ) 获利均未达当前高期望值。科技、能源和非必需消费品板块领跌指数,但并没有出现广泛的恐慌,SPX 的实际波动基本上低于 VIX 的隐含波动。

在加密货币方面,FOMC 会议的结果尚未产生明显影响,不过最新的法庭听证会消息指出,FTX 预计将全额赔付其客户,且因为难以找到买家,将放弃重启 FTX 2.0 的计划。虽然加密货币行业受到主流群体多次的攻击,但最大的破产事件现在将实现等值赔付(基于美元而不是代币),比起许多风险投资、私募股权二级市场、中国房地产债券和美国商业房地产基金“一文不值”的回收情况,加密货币也许并没有那么糟糕?

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:SignalPlus 123)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com