2023 年 10 月,LayerZero 建立了面向 Lido 所发行的 stETH 的跨链桥,允许将其跨链至 BNB Chain 和 Avalanche。

LayerZero 曾向治理组织 Lido DAO 寻求批准,但在该组织正式批准之前就部署了该跨链桥。技术上而言这并不违规,而这种做法也并非完全前所未见——Lido 曾建立了各种跨链桥,并非所有跨链桥都等到社区投票后才启动。但 Lido DAO 部分社区成员认为 LayerZero 营销方式不当,他们认为 LayerZero 试图在没有 DAO 批准的情况下冒充官方 Lido 合作伙伴。一名成员在 Lido DAO 治理论坛上发文表示:“宣布未定事件,是对 DAO 的不尊重,也是一种明显的不严肃的体现。”

当时一封由一系列加密基础设施提供商签署的声明表示,LayerZero 在不当利用先发优势,以在竞争对手之前“锁定”用户。Lido 战略顾问 Hasu 在 Lido DAO 论坛上表示:“通过单方面部署跨链桥并以官方方式营销,似乎是在向 DAO 施加压力,以避免流动性碎片化。通过这样的营销吸引用户,使得其他的跨链桥提案受限,并且让 DAO、Lido 质押者和参与链陷入了困境。”

随着越来越多的区块链诞生,跨链“互操作性”变得至关重要,跨链桥是跨链互操作性正常运作所需的关键基础设施。但是这些服务也容易出现问题,这就是为什么协议对它们授予认可的地方如此重要的原因。

Lido 的对 stETH 的认可被视为互操作性提供商的重要标志,根据 DeFi Llama 的数据,其 TVL 达 208 亿美元,在 DeFi 协议中位列第一。

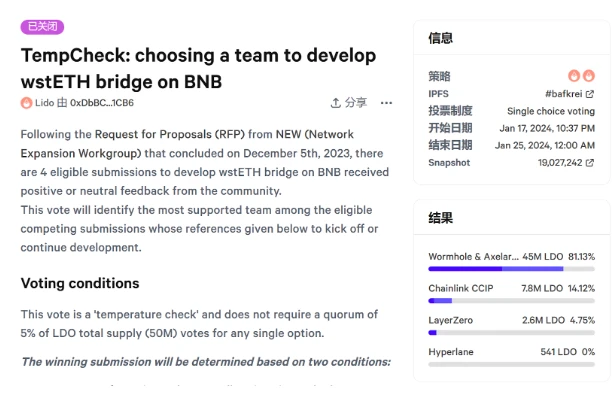

今年 1 月 17 日,Lido DAO 发起了一项选择 BNB Chain 的 wstETH 跨链桥开发者的温度检查投票,选项分别包括 Axelar & Wormhole、Chainlink CCIP、LayerZero、Hyperlane。最终 Axelar & Wormhole 支持率达 81.1% ,Chainlink 为 14.1% ,而 LayerZero 仅 4.7% 。

在即将进行的正式投票后,Axelar & Wormhole 将很快成为 stETH 跨链至 BNB Chain 的“官方”服务提供者。

Interop Labs(Axelar 开发商)首席执行官 Sergey Gorbunov 在接受 CoinDesk 采访时表示:“Axelar 和 Wormhole 团队决定合作,将两个网络的安全性有效结合起来,提供跨链 ETH LST 的有效安全性。”

Gorbunov 表示,Axelar 和 Wormhole 的目标是防止“服务提供商固化”,即服务提供商利用他们的先发优势永久巩固自己在协议基础设施中的地位。Axelar 和 Wormhole 跨链方式是开源且可扩展的,根据 Lido 基金会的选择,可能进行后端扩展以支持其他跨链桥提供商。这种可组合性是 Axelar+ Wormhole 提案中开源方法特点之一,其他提案无法复制,该“缺陷”导致了投票结果呈一边倒的形势。

Axelar 表示,跨链桥最初仅支持 BNB Chain,后续可能扩展至其他 EVM 链。

Wormhole 基金会首席商务官 Robinson Burkey 告表示:“在我看来,这不止是一次普通的治理投票,它变得更多地关乎原则而不仅仅是技术。代币持有者能够基于个人意愿支持符合协议利益的最佳选择,如果你剥夺了代币持有者的这种权力,那么就是在逐渐削弱去中心化的基本原则。”