编者按:作为 Asteroid Protocol 提出的首个 CFT 20 铭文,ROIDS 短短 24 小时内最高涨幅达到 11000 倍。尽管 Delphi 官推中强调 ROIDS 只是一个社会实验代币,但还是无法阻挡用户的 FOMO 情绪。加密研究员 yyy 在 X 平台发文对 Delphi Labs 进军 Cosmos 铭文的影响进行了探讨。Odaily星球日报整理如下:

Cosmos Hub 铭文 $ROIDS 24 小时最高涨 11000 倍的背后,是人性的贪婪,还是道德的沦丧,天网栏目为您揭秘Delphi Labs进军 Cosmos 铭文的背后,对 Cosmos Hub 的影响。

究竟是 Delphi saved the Hub 还是 Delphi destroyed the Hub? 故事还得从 1 天前 $ROIDS 的公平发射说起……

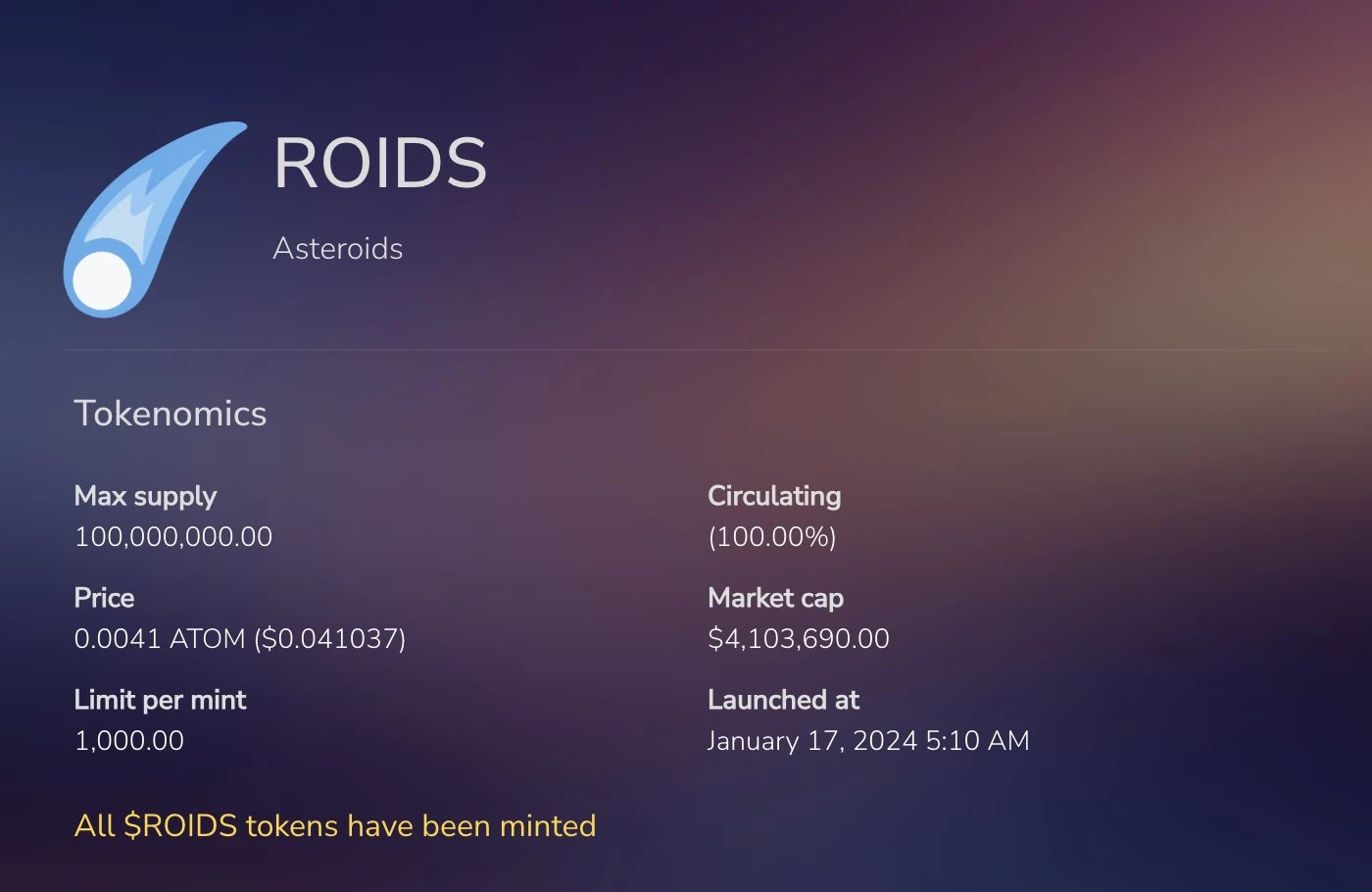

$ROIDS 是 Asteroid Protocol 提出的首个 CFT 20 格式的铭文,CFT 20 全称为 Cosmos Fungible Tokens.

Asteroid 作为开源的铭文协议由 Delphi Labs 和 Astroport 联合孵化,Delphi 本身也是自带流量的 VC, 是 $AXS 经济模型的缔造者,也是重仓 Luna 的落难者。

Delphi 官推中明确强调 $ROIDS 只是一个社会实验代币,没有任何投资价值,但完全无法阻挡用户的 FOMO 情绪。

$ROIDS 在短短数个小时内完成 100% 铸造,代币总量 1 亿枚,每张 1000 枚,共计 10 万张。

$ROIDS 的价格涨幅让人始料未及,短短 24 小时内最高涨幅达到 11000 倍。

单张 mint 价格为 0.00539 U, 最高单张 $ROIDS 价格突破 60 U,现在回落至 40 U-50 U 的区间。

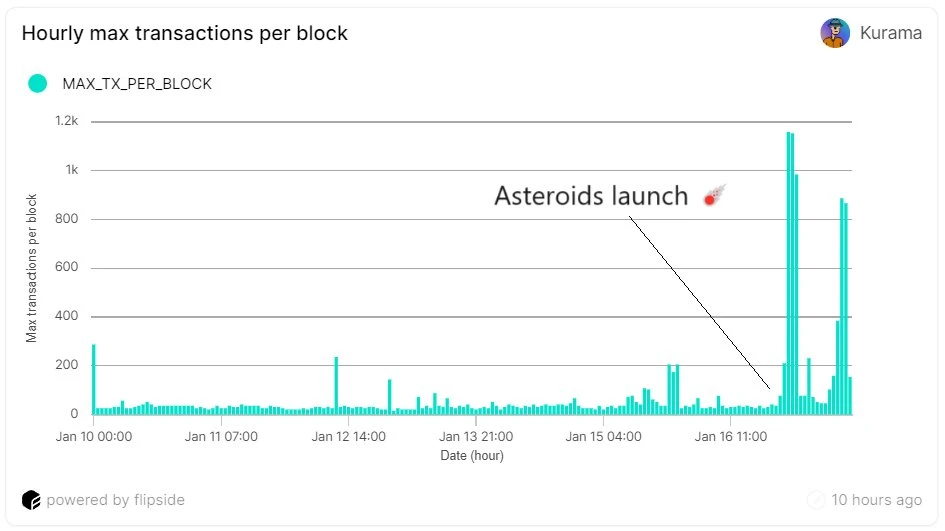

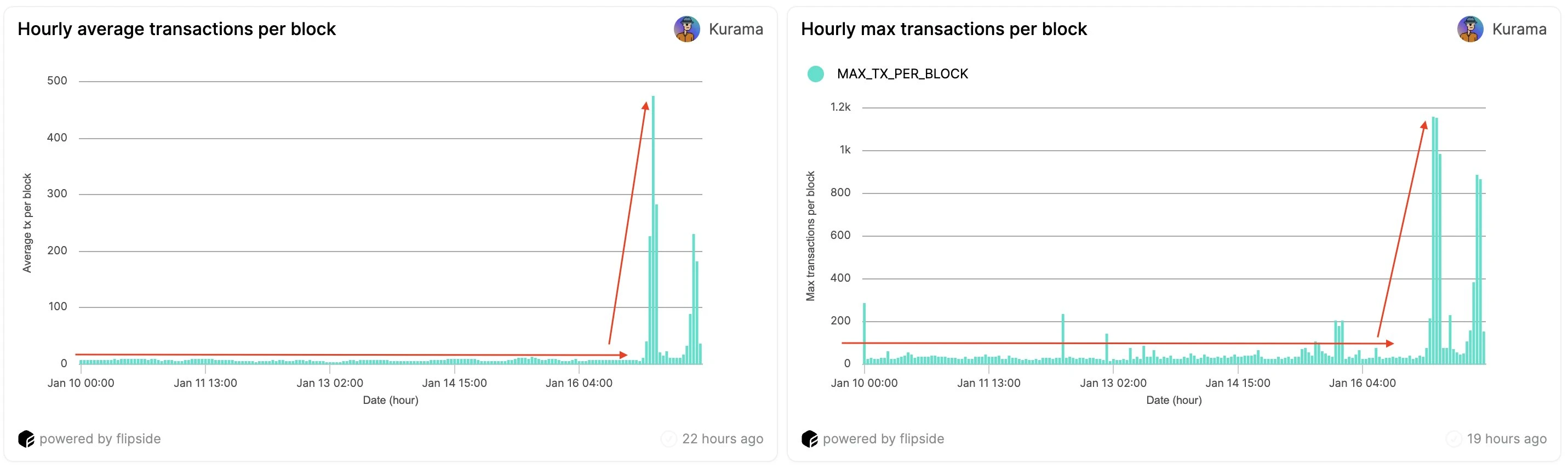

$ROIDS 是基于 cosmos Hub 发行的铭文,在 fairmint 期间 Cosmos Hub 链上交易激增,平均区块 tx 数和最大区块 tx 数都高达平时的百倍。

数据来源:https://flipsidecrypto.xyz/Kurama/2024-01-17-05-33-pm-qLcvvz…

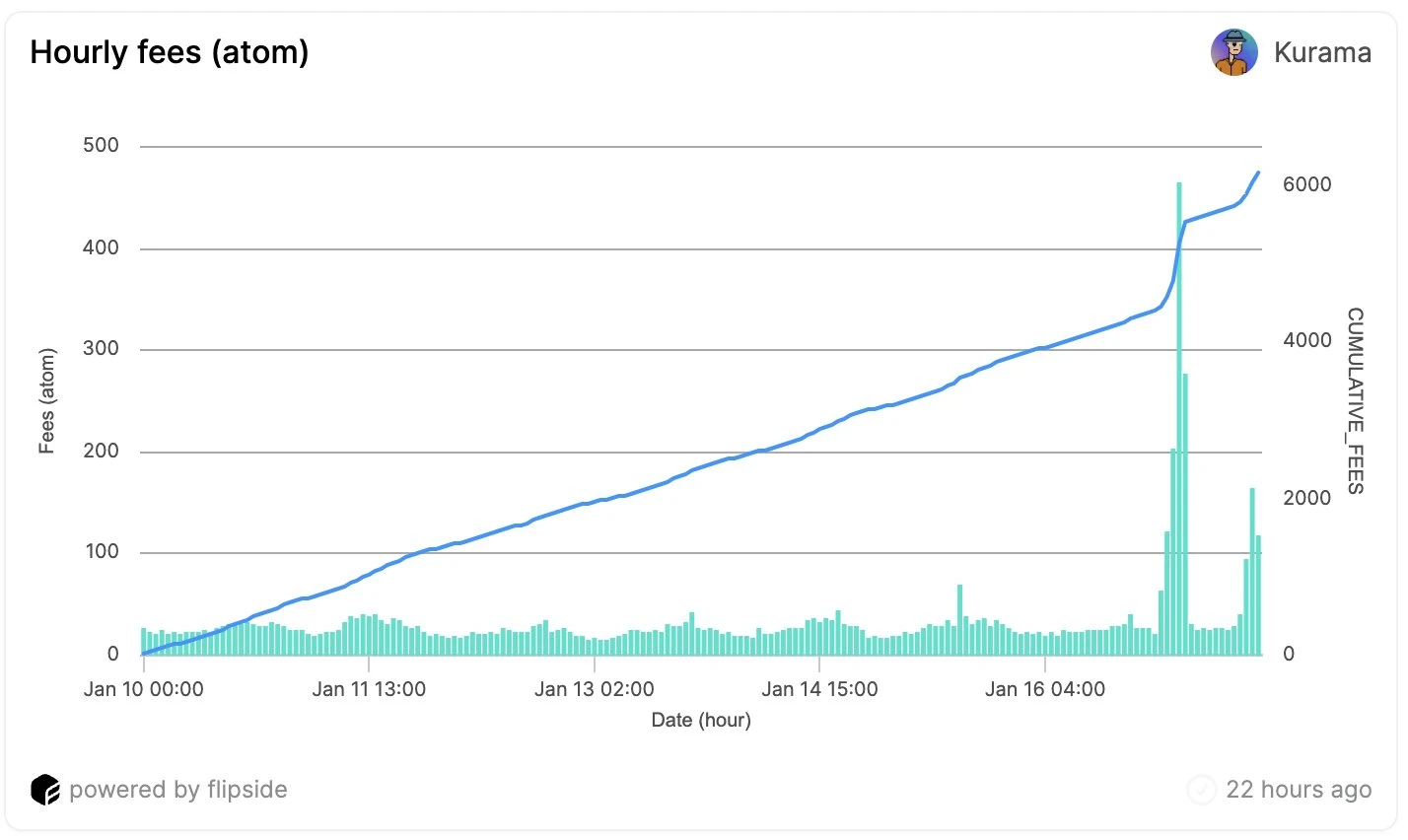

链上 tx 的激增产生了大量的 gas 费收入,如下图所示。

而链上 gas 手续费的捕获基本上分配给质押 $ATOM 的活跃验证者节点,小部分 2% 分配给社区池。

验证者节点又分为区块提议者和签名者,提议者可以获得额外 1% -5% 的 bonus 奖励。具体规则见文档链接,此处不赘述。

https://hub.cosmos.network/main/validators/validator-faq.html…

不可否认的一点是,验证者节点将受益于链上交易活跃带来的 gas 收入,是对 $ATOM 最直接的赋能,且有别于通胀赋能,不以 $ATOM 通胀作为代价。

虽然这部分收益很少,但的确是最直接、可持续的赋能方式。

权衡点在于: Cosmos Hub 作为专注于治理的链,为保证其绝对的安全性,Hub 一直遵循功能极简的理念,不支持智能合约场景。

而铭文的引入在一定程度上增加了 Cosmos Hub 的负荷和复杂性。

因此,这里出现了 $ATOM 直接赋能和 Cosmos Hub 潜在安全性的权衡。

我的观点是:Cosmos 铭文的引入利大于弊。除 gas 的直接捕获外,更重要的是铭文作为 Cosmos 生态新资产,为整个生态带来了更多潜在的应用场景。

Cosmos Hub 的铭文在 Cosmos 生态的正统性更强,更容易获得社区以及 Cosmos OG 们的认可。

借助于 IBC, Cosmos Hub 上的铭文资产可以便捷地跨链到 defi 应用链。 如 $ROIDS 可跨链至 Osmosis²,组成 $ROIDS- $ATOM LP 对进行流动性挖矿,实现价值赋能的同时扩宽了 $ATOM 的应用场景。

写在最后

Cosmos Hub 一直给人的刻板印象是传统和古板,缺乏创新,Hub 太需要新东西了。 而 Dephi 为 Hub 带来了铭文这种星星之火,希望可以燎原。