原文来源:Stacy Muur

原文编译:Luffy,Foresight News

加密研究机构 Delphi Digital 发布了一份 Web3 游戏年度报告,加密研究员 Stacy Muur 总结了报告的 20 个看点。

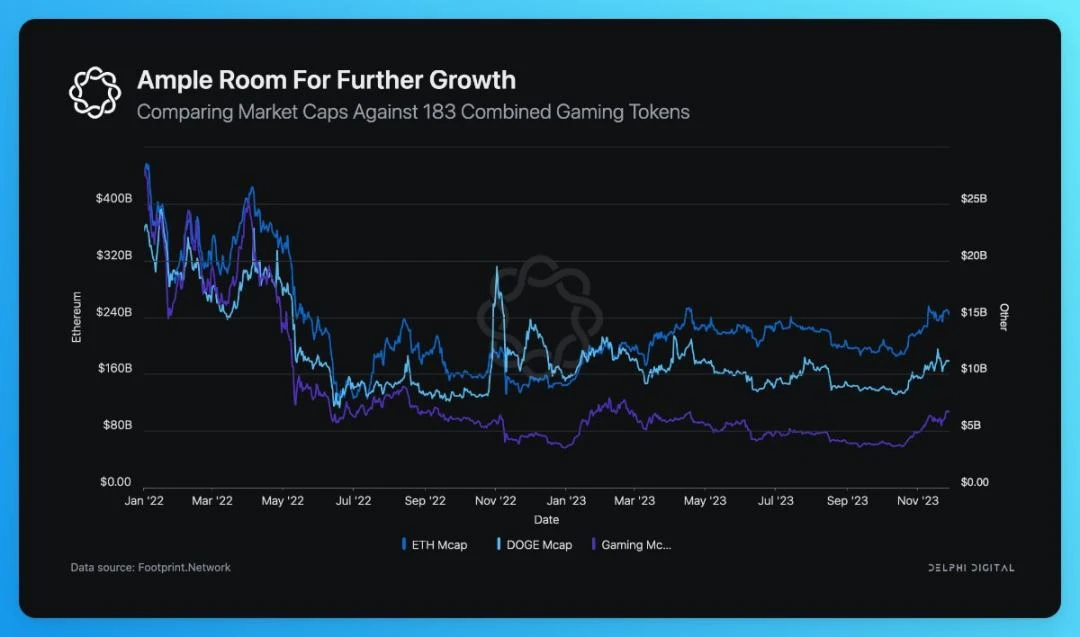

1、 2023 年 183 个游戏项目的总市值全年稳定在 40 至 70 美元之间,比 2022 年的历史高点下降了 86% 。但游戏行业仍有巨大的增长潜力。

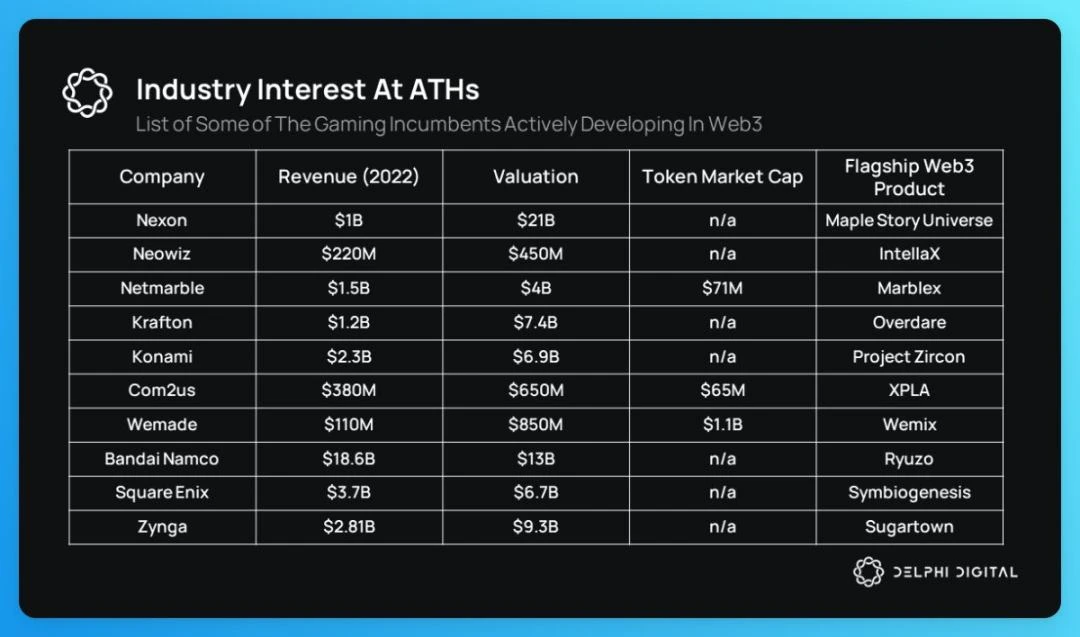

2、游戏巨头进入 Web3 市场的兴趣正在增长。

3、随着进入流程改进和法规更加宽松,移动端游戏已成为对 Web3 开发人员越来越有吸引力的平台。

4、区块链游戏的主要市场依次为菲律宾、尼日利亚、巴基斯坦、新加坡、越南、韩国、香港、中国和阿拉伯联合酋长国。

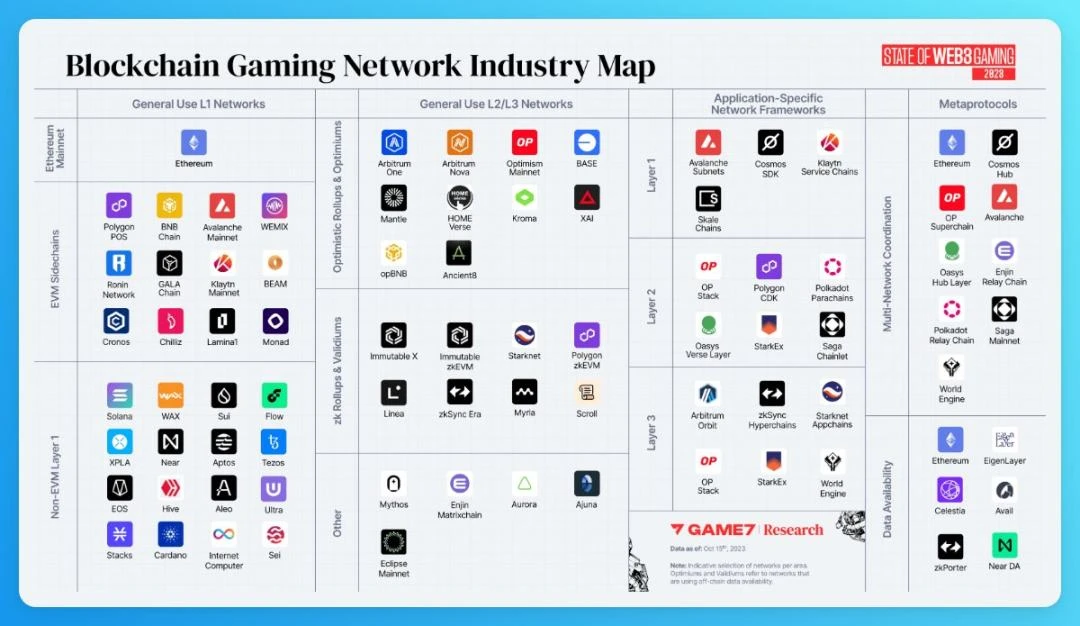

5、专注于游戏的区块链网络总数逐年增加。报告显示,仅 2023 年就出现了 76 个新网络,包括通用 L1、L2 和应用链。因此, 2024 年的一个重要主题对玩家流动性的争夺。

6、到 2023 年,区块链游戏产生的平均链上交易量是 DeFi 协议的 23 倍,显然这将成为许多游戏专用网络、子网和区块链的重点关注领域。

7、在所有可玩的区块链游戏中,只有略多于 5% 的游戏每日玩家数量超过 100 个用户钱包。

8、玩家激励、游戏启动和维护运营的成本不断上升,Web3 游戏在经济上难以维持。

9、区块链游戏的用户获取成本可能非常昂贵。事实上,某些案例研究表明,与非 Web3 游戏相比,区块链领域移动休闲游戏的客户获取成本高出 77% 。

10、为了实现盈利和规模化,众多 Web3 游戏将不得不扩大其商业化用户基础,增加鲸鱼的支出,或者两者兼有。

11、目前,每天约有 120 万个独立活跃钱包参与游戏,每日游戏交易为 1500 至 2500 万笔。

12、Optimism 和 OP Stack 成为全链游戏 (FOCG) 开发人员最受欢迎的选择。 Starknet 是 FOCG 另一个受欢迎的基础设施。

13、Telegram (TON) 加密游戏是一种新趋势。

14、人工智能驱动的「生成代理」将创造全新的玩家体验。

15、根据 Delphi 的观点,值得关注的人工智能和加密游戏交叉点的项目有 Parallel、Today - 、AI ARENA、Geppetto AI、AVALON。

16、Web3 游戏开发的基础设施正在快速扩张。

17、根据 Delphi Digital 的说法,潜力最大的两个项目是 HYTOPIA 和 Ronin Network。

18、过去两年,AAA 级游戏无疑是区块链游戏行业关注的焦点。

19、在高水平上,AAA 游戏不仅相互竞争,而且还与更广泛的 Web2 射击游戏市场竞争。

20、 2024 年对于 Web3 游戏行业来说将是激动人心的一年。