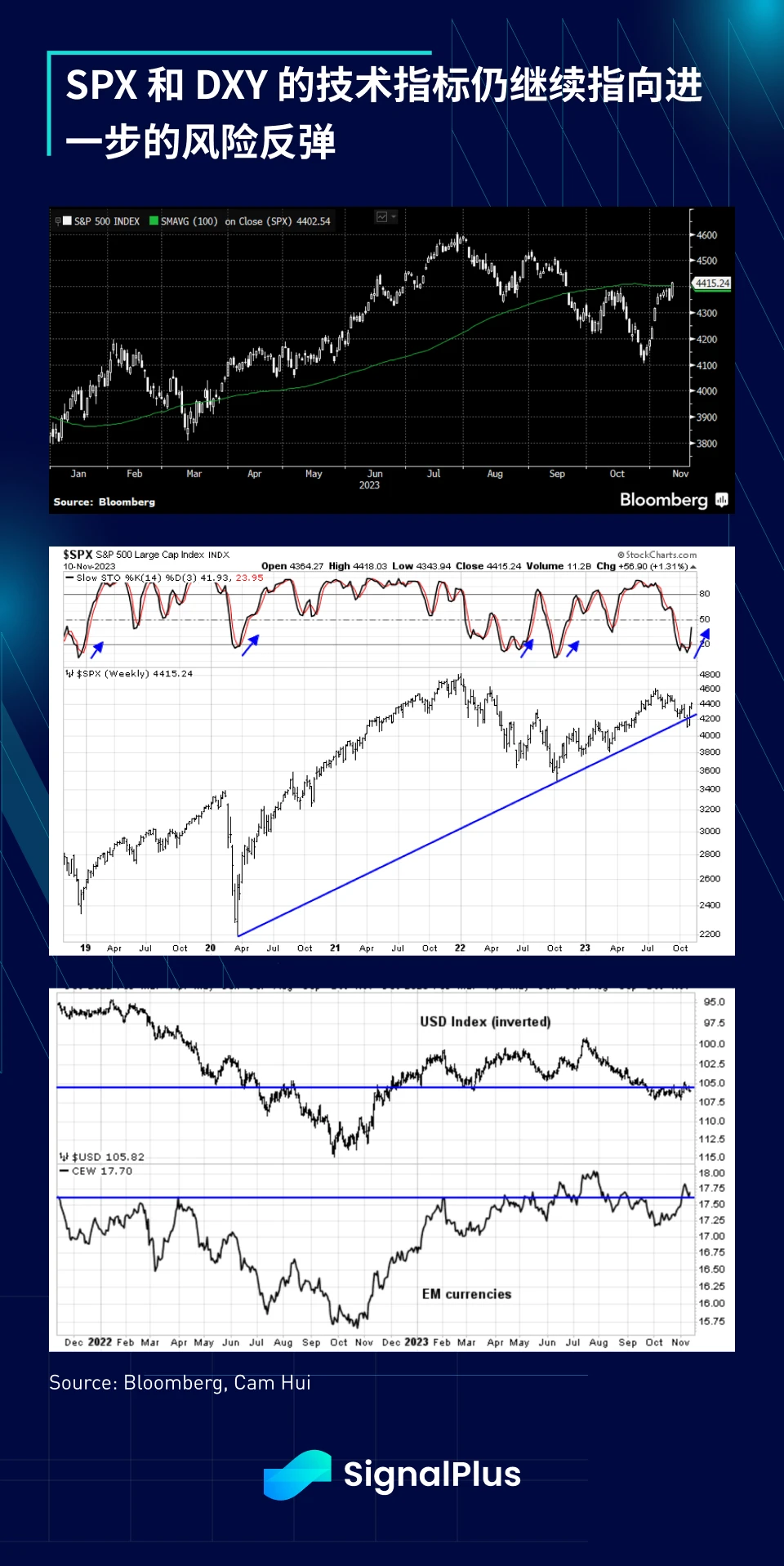

上周五,市场的交易活动较为清淡(正常交易量的 50 – 75% ),风险资产在上周的尾声仍表现强劲,SPX 重回 100 日均线和长期趋势线,且随机指标从超卖水平反弹;新兴市场货币似乎准备好突破,美元指数可能正在形成一个局部顶部,整体风险情绪依然高涨,市场目前几乎没有表现出疲软的迹象。

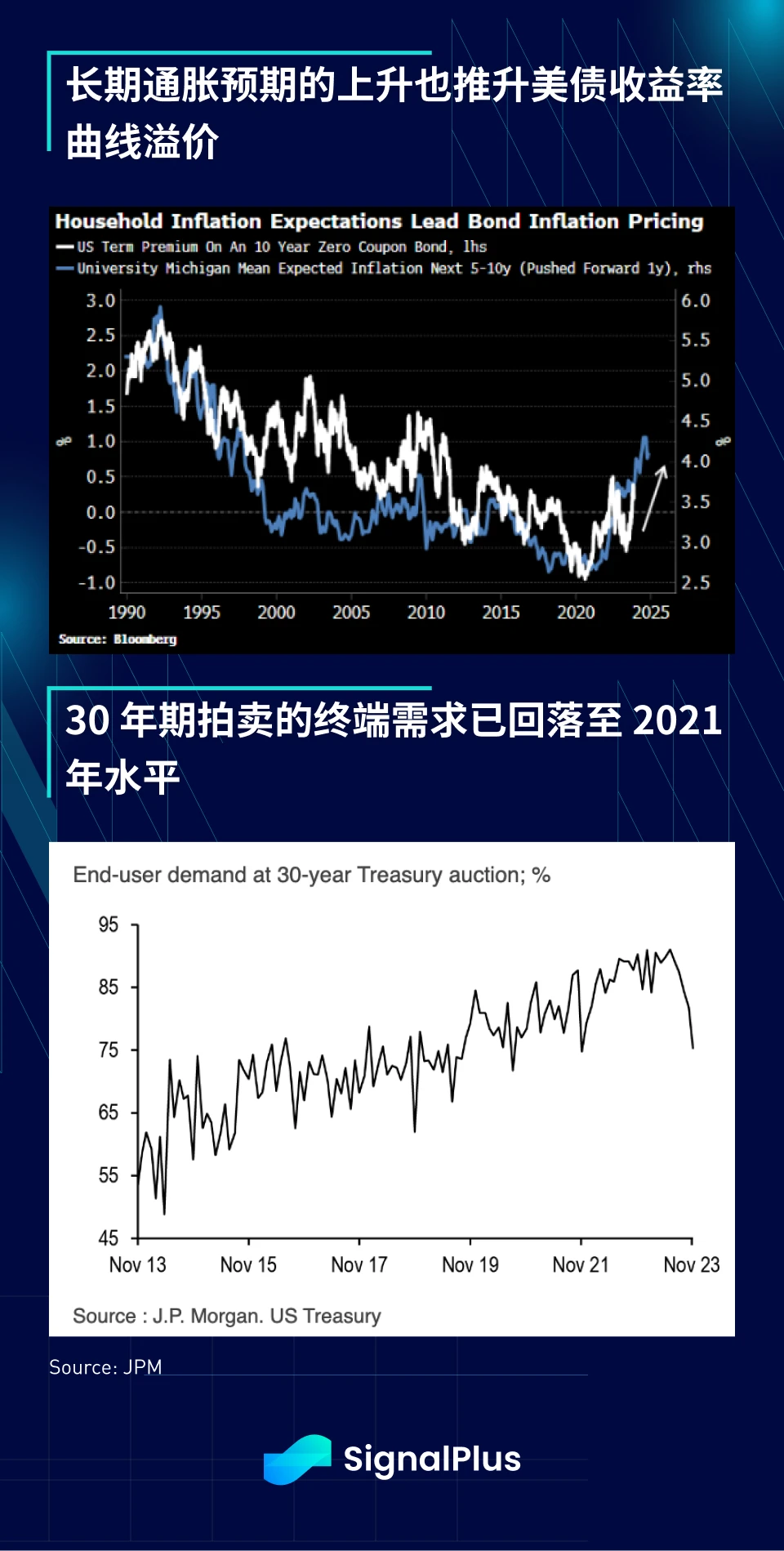

在利率市场方面,Lagarde 反驳了所有关于“在接下来几个季度”降息的预期,使得欧洲短天期债券疲软,导致利率市场在上周五交易日中走平;美国方面,唯一值得关注的数据是密大消费者信心调查,其中现况指数和预期指数均低于预期,另一方面,一年期通胀预期回升至 4.4% ,高于市场预期, 5 – 10 年长期通胀预期也相应上升;长期通胀预期的上升通常对固定收益期限溢价不利(长天期利率更高,曲线更陡),这是美联储在解决通胀预期问题时最大的担忧之一。

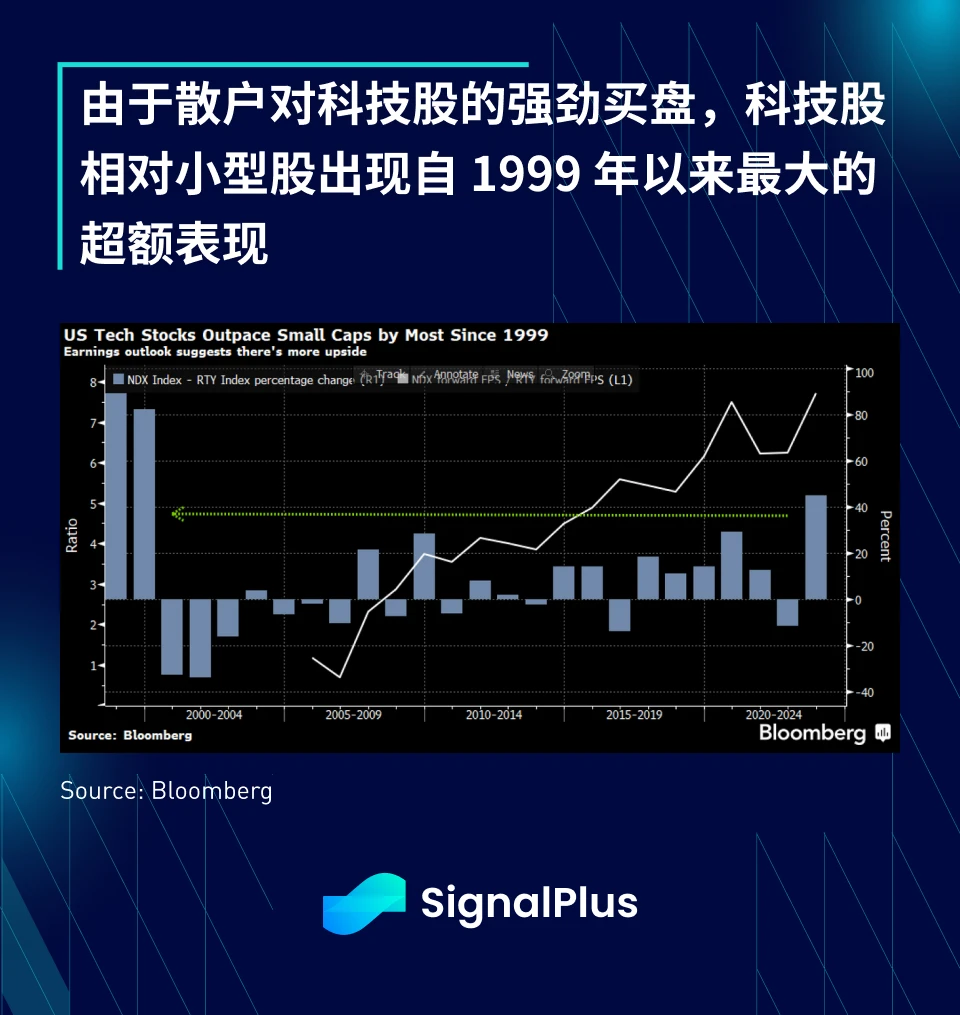

根据 JPM 的数据,散户交易员过去几周一直积极增加股票敞口(比 12 个月平均还高出 + 1.4 个标准差),其中大部分资金流入是通过 ETF,与整体指数相比,对科技股的偏好相当明显(SPX -1.3 个标准差,NASDAQ + 1.2 个标准差),而尽管固定收益强劲反弹,流入债券的资金相对有限(+ 0.4 个标准差),据估计,CTA 通过空头回补增加了近 60 亿美元的股票敞口,而机构投资者则增加了 180 亿美元的股票期货多头部位。

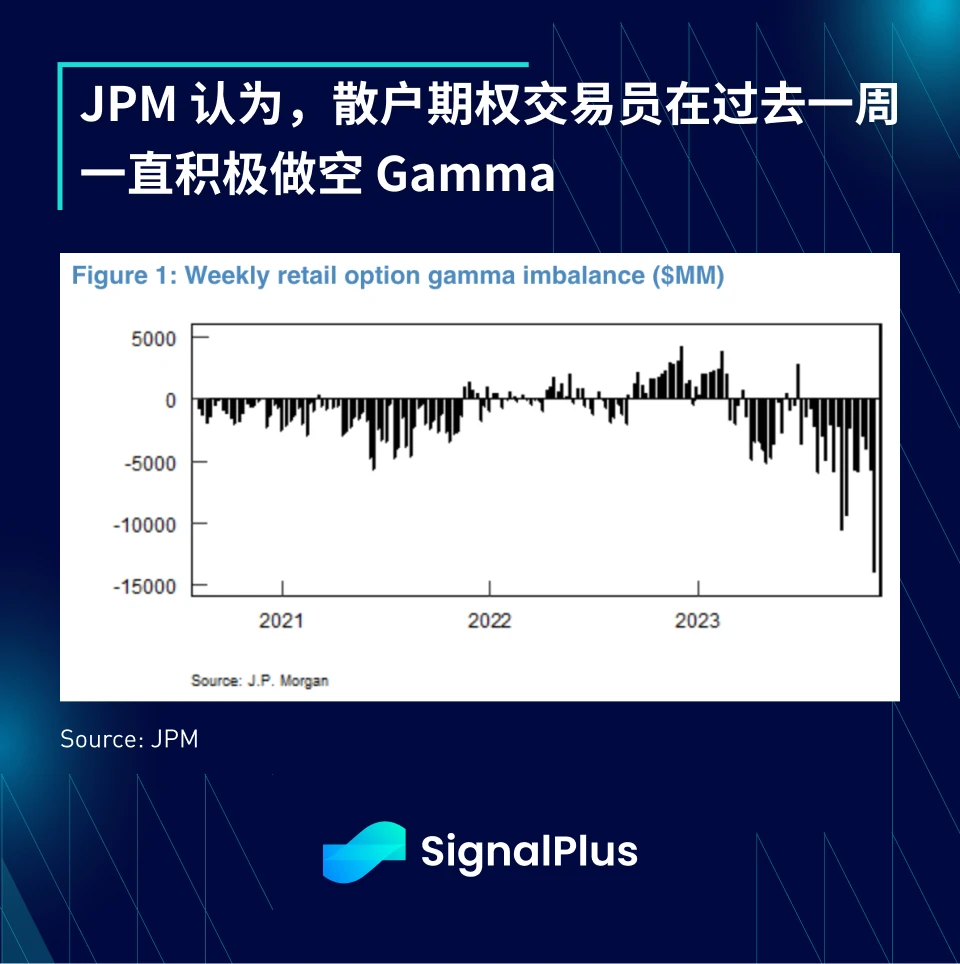

在期权市场方面,散户交易员积极做空 Delta 和 gamma 敞口,主要通过 0 DTE 进行操作,JPM 估计由此产生的 gamma 不平衡将是其历史数据上最严重的,这种 gamma 不平衡(与券商多头相反)可能导致了股市的稳定上涨,SPX 指数在过去 10 天中有 9 天呈现涨势。

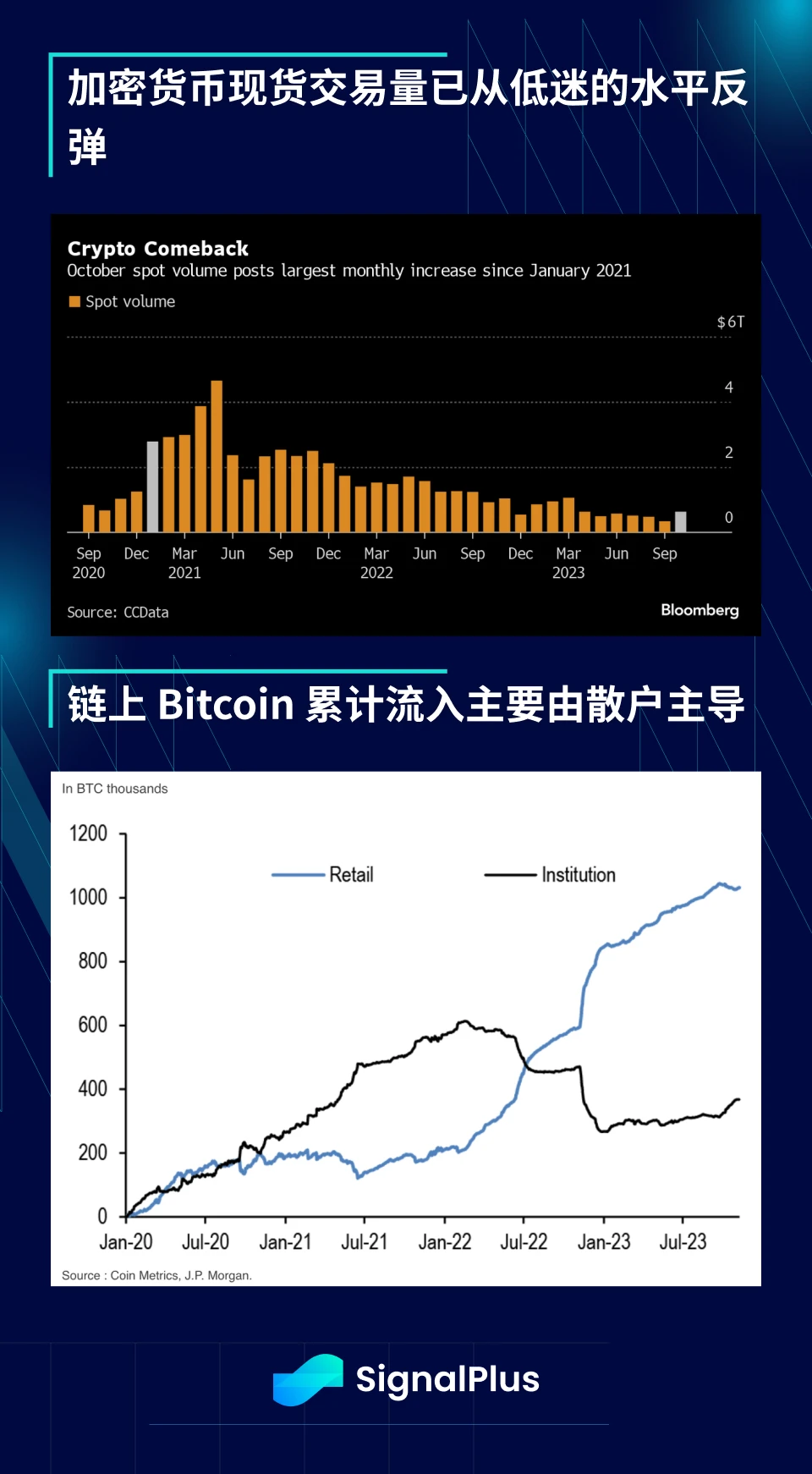

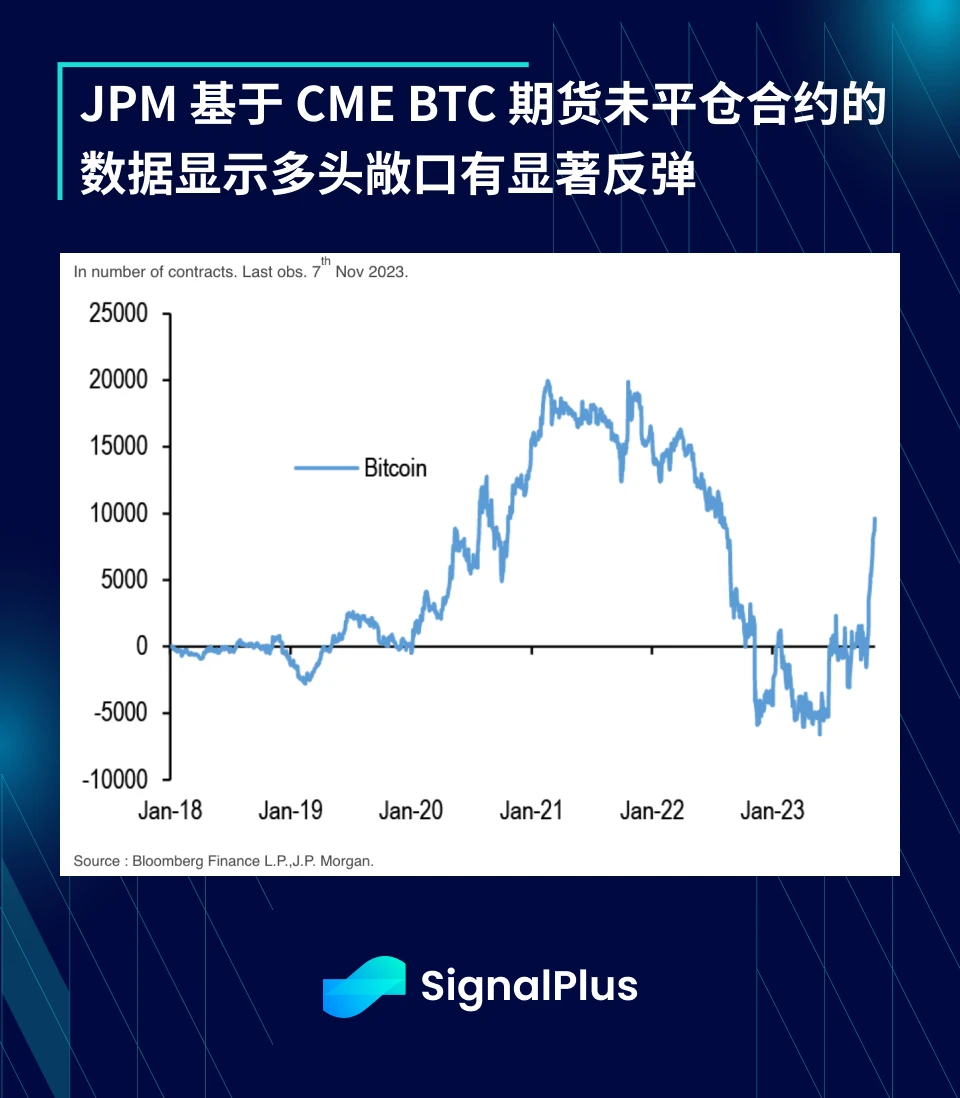

在加密货币方面,现货交易量出现自 2021 年 1 月以来最大月度增幅(虽然是从低迷水平反弹),这主要是由散户多头带动,且在 ETF 批准之前机构买入也有所回升;目前的多头头寸似乎已经超过基本面,即使 ETF 迅速获得批准,要带来结构性资金流入至少也要等几个季度,因此,我们建议在此时考虑获利了结/进行一些价外备兑看涨期权操作。

您可在 ChatGPT 4.0 的 Plugin Store 搜索 SignalPlus ,获取实时加密资讯。如果想即时收到我们的更新,欢迎关注我们的推特账号@SignalPlus_Web3 ,或者加入我们的微信群(添加小助手微信:xdengalin)、Telegram 群以及 Discord 社群,和更多朋友一起交流互动。

SignalPlus Official Website:https://www.signalplus.com