原文作者:Axel Bitblaze(@Axel_bitblaze 69 )

原文编译:Joyce,BlockBeats

编者按:加密研究员 Axel Bitblaze 从技术、用例、性能、共识机制、市场地位及代币经济学角度分析了 Injective、Oasis 和 Near 三条公链。并根据 Injective 的交易量 / 市值比率较高,认为短期内市场对 Injective 的兴趣更多,其上的交易也更为活跃。BlockBeats 编译如下:

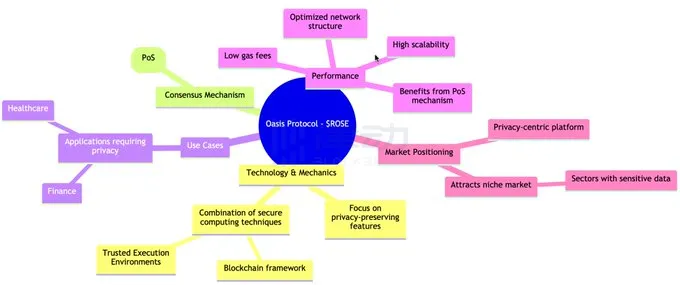

专注于隐私的 L1 解决方案 Oasis Protocol

技术:专注于隐私保护功能;结合安全计算技术(如可信执行环境)以及区块链框架;

共识机制:采用权益证明(PoS)来达成共识;

用例:主要针对需要隐私的应用程序;尤其适用于需要保护敏感数据的医疗保健或金融领域;

性能:具有高可扩展性和低 gas 费;PoS 机制和优化的网络结构的优势;

市场定位:作为一个以隐私为中心的平台,可能会吸引一个利基市场;对处理敏感数据的行业尤其有吸引力。

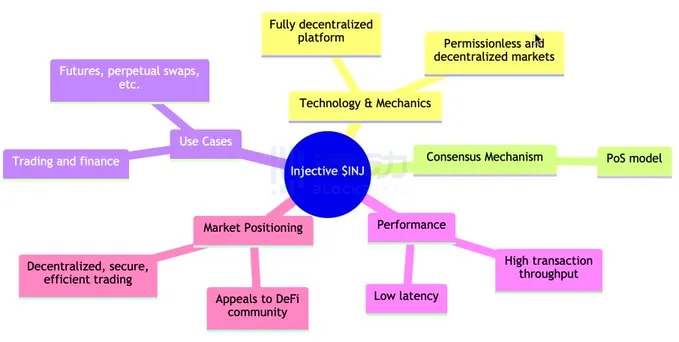

DeFi 和衍生品 L1 解决方案 Injective

技术:旨在为衍生品和无 DeFi 创建一个完全去中心化的平台;允许创建无需许可和去中心化的市场;

共识机制:使用 PoS 模型,有助于更快的交易速度和更低的费用;

用例:专注于交易和金融,支持期货、永续期货等一系列金融产品;

性能:高交易吞吐量和低延迟,解决了 DeFi 和交易中的一些常见痛点;

市场定位:对 DeFi 社区和寻找去中心化、安全高效交易平台的交易员具有强烈吸引力。

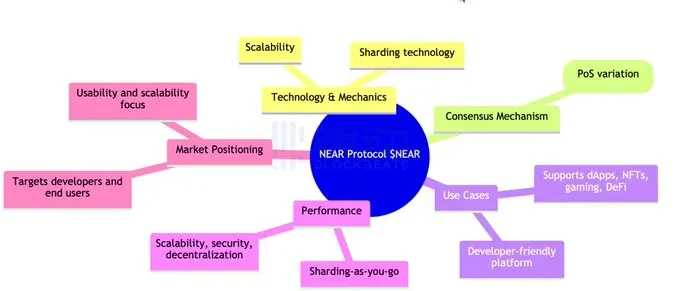

Near protocol

技术:利用分片技术实现可扩展性,允许网络在增长时处理更多事务;

共识机制:采用 Nightshade,一种 PoS 的变体,有助于实现高吞吐量和低交易成本;

用例:旨在成为一个开发者友好的平台,支持各种 dApp,包括 NFT、游戏和 DeFi;

性能:采用了一种独特的分片方法(sharding-as-you-go),为区块链不可能三角问题提供了一个潜在的解决方案;

市场定位:专注于可用性和可扩展性,旨在瞄准区块链生态系统中从开发者到最终用户的更广泛细分市场。

对比分析

1)侧重领域

- $ROSE 因其隐私功能而与众不同。

- $INJ 针对 DeFi 和交易市场。

- $NEAR 将自己定位为适用于各种 dApp 的通用、可扩展区块链。

2)技术优势

- $ROSE 隐私保护方法是一个关键的差异化因素,在关注数据敏感性的行业尤其相关。

- $INJ 为金融部门提供专业工具,特别是衍生品和交易。

- $NEAR 分片技术为可扩展性提供了坚实的基础,对许多 dApp 开发人员具有广泛的吸引力。

3)用例和生态系统

- $ROSE 可能会在需要数据隐私的行业中看到利基采用。

- $INJ 可以吸引金融机构和 DeFi 爱好者。

- $NEAR 由于其灵活性和可扩展性,有可能被更广泛地采用,吸引了多样化的 dApp 开发。

4)投资者视角

- $ROSE 对于那些希望投资加密货币隐私领域的人来说可能很有吸引力。

- $INJ 可能会吸引对区块链上金融应用的增长和创新感兴趣的投资者。

- $NEAR 对于押注区块链技术在各个领域广泛采用的投资者来说,这可能是一个合适的选择。

代币经济学

1)市值

• $NEAR 1, 228, 940, 901 美元

• $ROSE : 263, 770, 383 美元

• $INJ 1, 152, 649, 407 美元

分析:

与 ROSE 相比,NEAR 和 INJ 的市值明显更高。这表明市场估值更高,投资者的信心或效用感知可能更高。较高的市值通常意味着在市场上的地位更成熟,但也可能意味着更成熟,与小盘币相比,可能提供更低的增长率。

2) 24 小时交易量及市值比率

- $NEAR :

- 交易量: $ 22, 437, 661

- 交易量/市值比率: 0.02

- $ROSE :

- 交易量: $ 6, 461, 412

- 交易量/市值比率: 0.02

- $INJ :

- 交易量: $ 51, 954, 873

- 成交量/市值比率: 0.05

分析:

$INJ 相对于其市值,交易量明显更高,表明交易更活跃,短期内可能有更高的流动性和投资者兴趣。

$NEAR 和 $ROSE,虽然具有相似的比率,但相比之下不太活跃。

供应指标:

1)流通供应量

- $NEAR : 989, 205, 461 (占总供应量的 98.92% )

- $ROSE : 5, 029, 357, 184 (占总供应量的 50.29% )

- $INJ : 83, 755, 556 (占总供应量的 83.76% )

2)总供应量和最大供应量

- $NEAR : 10 亿总供应量,未定义最大供应量

- $ROSE : 100 亿总供应量,未定义最大供应量

- $INJ : 1 亿总供应量和最大供应量

$NEAR 其供应量几乎完全流通,表明通胀压力有限。

$ROSE 只有其总供应量的一半在流通,可能导致通货膨胀影响。

$INJ 供应有上限,如果需求保持强劲,则吸引价值升值。

代币经济学的结论

• $INJ 脱颖而出 - 相对于其市值,它的交易量更高,这可能表明市场兴趣或投机交易更活跃。

• 流通供应比例至关重要:

- $NEAR :几乎完全稀释。

- $INJ : 大部分的代币供应量已经达到了设定的最大供应上限,并可以在市场上自由交易。

- $ROSE : 相当一部分尚未进入流通。