尽管美国经济在第一季度录得低于预期的 1.1% 年化增长,但由于加息对 GDP 构成压力且经济衰退的威胁减弱,股市仍飙升。

消息传出后,比特币 (BTC) 一度跌至 28,748 美元,随后反弹至 28,934.06 美元。以太坊 (ETH) 从 1,883 美元跌至 1,869.53 美元,随后升至 1,883.40 美元。

随着衰退对美国经济的威胁下降,股市飙升

美国主要股市对该消息反应积极,道琼斯指数上涨 0.3%,标准普尔 500 指数上涨 0.6%,纳斯达克综合指数上涨 0.9%。

受正面财报消息的提振,Meta 的股价上涨了约 14%,而在收市后发布财报电话会议的亚马逊当天上涨了 3%。

由于交易员采取鸽派立场,预计到 2023 年底将降息三次,市场普遍预测 GDP 将增长 2.2%。GDP 也较上一季度的 2.6% 大幅下降。

本周早些时候,分析师 Noelle Acheson 指出,10 年 1 月的收益率曲线没有倒转。倒曲线是衰退指标。

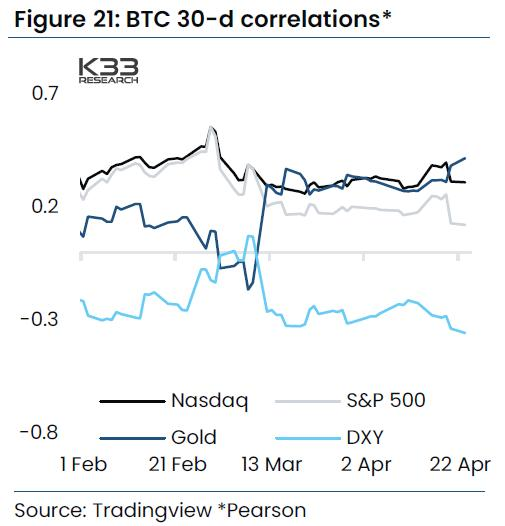

尽管消息传出后比特币交易基本持平,但 K33 Research 表示,在一系列国际银行假期期间,比特币将在未来几周与美国股市相吻合。

BTC 关联美国股票BTC-30 天相关性 |资料来源: K33 研究

自 2022 年 10 月以来,衡量美元兑其他主要货币强弱程度的美元指数已下跌 12%。

除非出现特定于加密货币的市场事件,否则 2022 年美元走强有时与比特币价格下跌相关。 8月美联储宣布进一步加息后,美元指数上涨,而比特币下跌11%。

在GDP数据公布前, BTC与美元的90天相关性为-0.7%。在此之前,美元指数自 10 月以来下跌了 12%。

这种关系表明,在 GDP 结果之后美元的任何进一步下跌都可能使比特币受益。

美联储预测还会加息两次

市场还将关注将于周五公布的美国个人消费支出指数,美联储将利用该指数评估其加息政策对经济的有效性。央行将于 5 月 3 日宣布下一次加息。

周四,美联储主席杰罗姆·鲍威尔 (Jerome Powell) 向冒充乌克兰总统泽伦斯基 (Volodymyr Zelensky) 的恶作剧者建议再两次加息25 个基点。

他说经济衰退“几乎与非常缓慢的增长一样可能”。

“我们需要一段放缓的增长期,这样经济才能降温,劳动力市场才能降温,工资才能降温。这就是通货膨胀下降的方式。这是我们知道降低通货膨胀的唯一方法。这可能会很痛苦,但我们不知道有什么不痛不痒的方法可以降低通胀。”

来源:Zerohedge

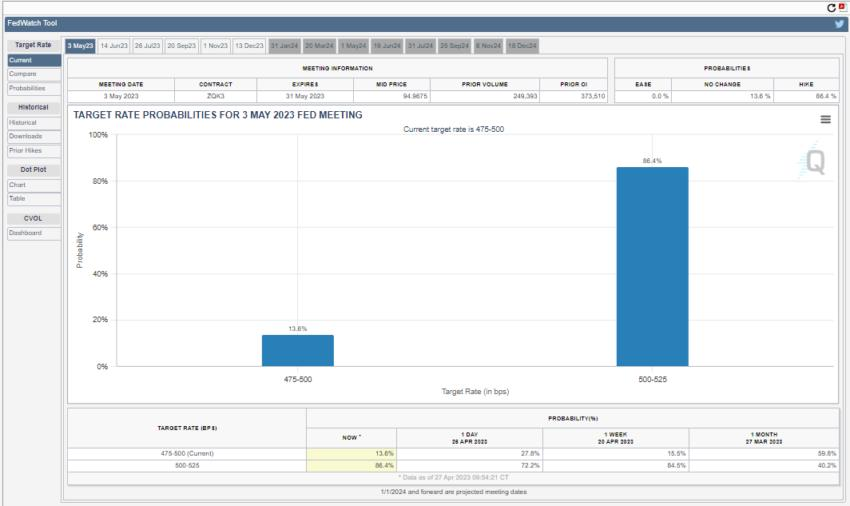

CME 目标利率CME FedWatch 目标利率预测 |资料来源:芝商所

CME FedWatch 工具对此表示赞同,认为即将到来的 25 个基点加息的可能性为 87.4%