Editor's Note: While the market has grown accustomed to categorizing Bitcoin as a "risk asset," the recent market movement triggered by the Iran conflict has delivered a clear signal that deviates from the consensus: against a backdrop of falling traditional assets and failing safe-haven assets, Bitcoin has instead strengthened.

Author Matt Hougan (current Bitwise CIO, co-founder of Future Proof, former CEO of ETF.com) argues that Bitcoin's rise is not "ignoring the war," nor is it solely the result of "money printing expectations," but is directly driven by the geopolitical conflict itself.

Hougan proposes a more explanatory framework—Bitcoin is not a single asset, but a "stacked bet": on one hand, it is competing with gold for the status of a "store of value"; on the other hand, it is also making a bet, albeit with low probability but high elasticity, on becoming a true global currency.

In the past, this second layer of logic was more of a distant imagination. However, as the financial system is gradually "weaponized," this hypothesis is beginning to move from the fringe to reality. From SWIFT sanctions to the rise of parallel settlement networks, to Iran's attempt to collect shipping passage fees in Bitcoin, Bitcoin is no longer just a tool against inflation; it is also being incorporated into the borderlands of national-level games.

Against this backdrop, Bitcoin's pricing logic has also changed. It is no longer driven solely by liquidity, tech stocks, or risk appetite, but has begun to price in the "uncertainty of the global monetary system." When conflicts increase the probability of its "monetary attributes" being realized while amplifying the volatility of the global financial system, the upside potential of this asset is also reopened.

If the narrative of Bitcoin over the past five years has focused on "digital gold," what is emerging now is a more complex dual role: both a store of value and a potential depoliticized settlement medium. And once this structure is established, its market boundaries may no longer be limited to the $38 trillion corresponding to gold.

Below is the original text:

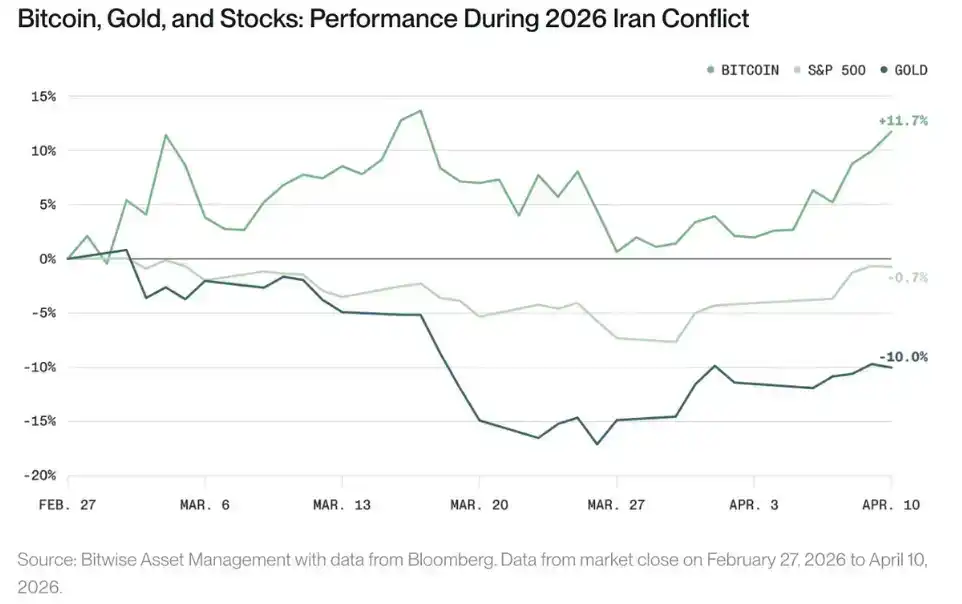

Bitcoin has performed relatively strongly since the outbreak of the Iran conflict. Since the U.S. and Israel began airstrikes against Iran on February 28, Bitcoin has risen by 12%, while the S&P 500 index has fallen by 1%, and gold has dropped by 10%.

This has surprised many. Bitcoin has long been viewed as a risk asset, and many originally believed it should fall during the "risk-off" sentiment triggered by geopolitical conflict. Consequently, various explanations have emerged: some argue that geopolitics is irrelevant to Bitcoin; others point out that wars often lead to money printing, which in the long run benefits Bitcoin.

Neither explanation is accurate. Bitcoin's strong performance during this crisis stems precisely from the conflict itself. Understanding this is important.

One Investment, Two Bets

Buying Bitcoin is essentially betting on two things simultaneously.

First, you are betting that Bitcoin will become "digital gold" and compete with physical gold in the $38 trillion "store of value" market. This is Bitcoin's primary use case currently and a bet I find very attractive. As I have explained before, simply capturing about 17% of this market over the next decade could potentially drive Bitcoin's price to $1 million.

But when you buy Bitcoin, you are actually making a second bet—that one day, perhaps, Bitcoin will function like a traditional currency.

In the past, I have always viewed this as an "out-of-the-money call option": a speculative bet on a future that is unlikely to materialize. After all, for most of Bitcoin's existence, this possibility seemed extremely remote to most people. Until a few years ago, the global financial system was almost entirely built on the U.S. dollar track, and using a volatile, early-stage "cryptocurrency" for international trade sounded more like a fantasy at the time.

The turning point came in 2022, when the U.S. kicked Russia out of the dollar-centric SWIFT system. The French finance minister called it a "financial nuclear bomb" at the time, and countries became alert. China quickly built a parallel financial system, and other countries also took action. Russia moved 99% of its financial activities to these new systems, and other countries began to experiment.

At the time, I pondered that weaponizing SWIFT might open up space for Bitcoin: if countries gradually become reluctant to rely on the dollar system, it seems logical that at some stage they might turn to a "depoliticized" alternative.

And in this Iran conflict, we are seeing an early (and unsettling) manifestation of this trend: Iran stated in an interview with the Financial Times that it would begin charging all ships passing through the Strait of Hormuz a "toll" of $1 per barrel (approximately $20 million per day), to be settled in Bitcoin.

Obviously, this move raises important concerns about sanctions evasion and money laundering. Although in a sense it might be preferable to the status quo—for years, Iran has been evading U.S. sanctions through China's financial systems, which are harder to track than cryptocurrencies—it also brings new risks.

At the same time, it reveals a reality beyond the current conflict: in a world where countries are weaponizing financial systems, Bitcoin is gradually becoming a depoliticized alternative.

Option Pricing Logic

This is also why I analogize Bitcoin's potential as a currency to an "out-of-the-money call option."

The value of an option typically stems from two points: either the probability of reaching the target price increases, or the volatility of the underlying market rises.

In this Iran conflict, both occurred: first, the probability of Bitcoin being used as a "currency" rose; second, the uncertainty and volatility of the global monetary system increased.

This analytical framework can help us understand two important things. First, in future geopolitical conflicts, Bitcoin is likely to continue rising—especially in regions caught between the U.S. and Chinese systems. Second, Bitcoin's potential market size may far exceed the $38 trillion gold market.

Over the past five years, we have almost exclusively viewed Bitcoin as a "store of value." But if it begins to play a dual role as both a "store of value" (like gold) and a "payment currency" (like the dollar), then we may need to readjust our expectations for its long-term potential upward.