Authors: Joel John, Siddharth, Saurabh Deshpande

Compiled by: Felix, PANews

Under the impact of AI, the crypto field is in a period of low sentiment. With VCs leaving and founders considering transitioning to AI, is the crypto industry worth sticking with? Decentralised.co recently analyzed protocol revenue from a data perspective, pointing out that crypto asset valuations are returning to rationality, and the era of high premiums for infrastructure tokens has ended. Founders must abandon empty narratives, establish business models based on real revenue and moats, and endow tokens with actual rights. Details are as follows:

The "Fear and Greed Index" of the crypto market is at a historical low. At the same time, its profitability has reached unprecedented heights. Since 2018, DeFiLlama has tracked crypto-native protocols generating $74.8 billion in fees, with nearly half ($31.4 billion) generated in the 18 months from January 2024 to June 2025.

After experiencing some of the best performing quarters in the past eight years, why is an industry still mired in fear?

Entropy Protocol, Milkyway Protocol, Nifty Gateway, Rodeo, Forgotten Runiverse, Slingshot, Polynomial, Zerelend, Grix Finance, Parsec Finance, Angle Protocol, Step Finance—these twelve projects have shut down one after another in the past two months. These products had been operating for years, built by passionate founders. Additionally, OKX, Mantra, Polygon Labs, Gemini, and Binance have all conducted layoffs.

Fewer people are attending industry conferences, VCs are turning to AI, and developers are flocking to AI in droves. This apocalyptic pessimism is real. "If you're still in crypto, switch to AI" has become the mainstream view.

But should you really do that?

We have been pondering this question for the past few weeks. When a new technology emerges, the market initially gives it a premium due to its novelty and grand vision. In the 19th century, nearly 6% of the UK's GDP was invested in railway stocks. By 2026, the capital expenditure of major cloud service providers will account for 2% of US GDP. But when reality sets in, technology trends return to more reasonable valuations. The key is whether an industry can prove its value after returning to rationality.

This article will dissect the historical evolution of cryptocurrency revenue, the stickiness of the funds generated, and the nature of moats in the industry.

Studying the Ledger

Since the birth of the crypto industry, crypto-native businesses have been generating revenue. Exchanges like Bitmex, Binance, and Coinbase are all profitable enterprises. They are centralized, owned by a few, and their revenue is not public. DeFi-native infrastructures like decentralized exchanges (Uniswap) and lending platforms (Aave) changed this, allowing users to see the daily earnings of protocols.

There was an expectation that the trading valuation of tokens would reflect the economic activity facilitated by these infrastructures.

As of 2022, DEXs accounted for a high of 28.4% of revenue, with total revenue reaching $2.27 billion that year. The lending sector was similar and highly concentrated. Aave and Compound accounted for 82% of all lending fees. While there were leaders, there was also anticipation for protocols that were growing and trying to capture market share.

The technology itself was novel enough to warrant high valuations.

Cryptocurrency expansion in the consumer sector followed closely. NFTs represented a promising vision: putting cultural value on-chain. Celebrities known to the masses changed their profile pictures (PFPs) on X, and people thought this would translate into mass adoption. OpenSea generated $1.55 billion in revenue, accounting for 71.7% of all NFT marketplace revenue. In hindsight, its $13 billion valuation didn't seem so absurd; they themselves had the potential to develop into a long-term monopoly.

However, fate and the market had other plans. By 2025, NFTs accounted for less than 1% of total revenue. We experienced a "Beanie Baby moment" but were left without any physical mementos. In contrast, DEXs grew rapidly but struggled to see valuation growth. Last year, DEXs generated $5.03 billion in fees, and lending platforms generated $1.65 billion. Combined, these two sectors accounted for 22.9% of total fees, down from 33.1% in 2022.

Their share of economic activity in the larger pie shrank, and their valuations plummeted accordingly.

So, which areas actually grew? How have crypto-native business models changed since 2022?

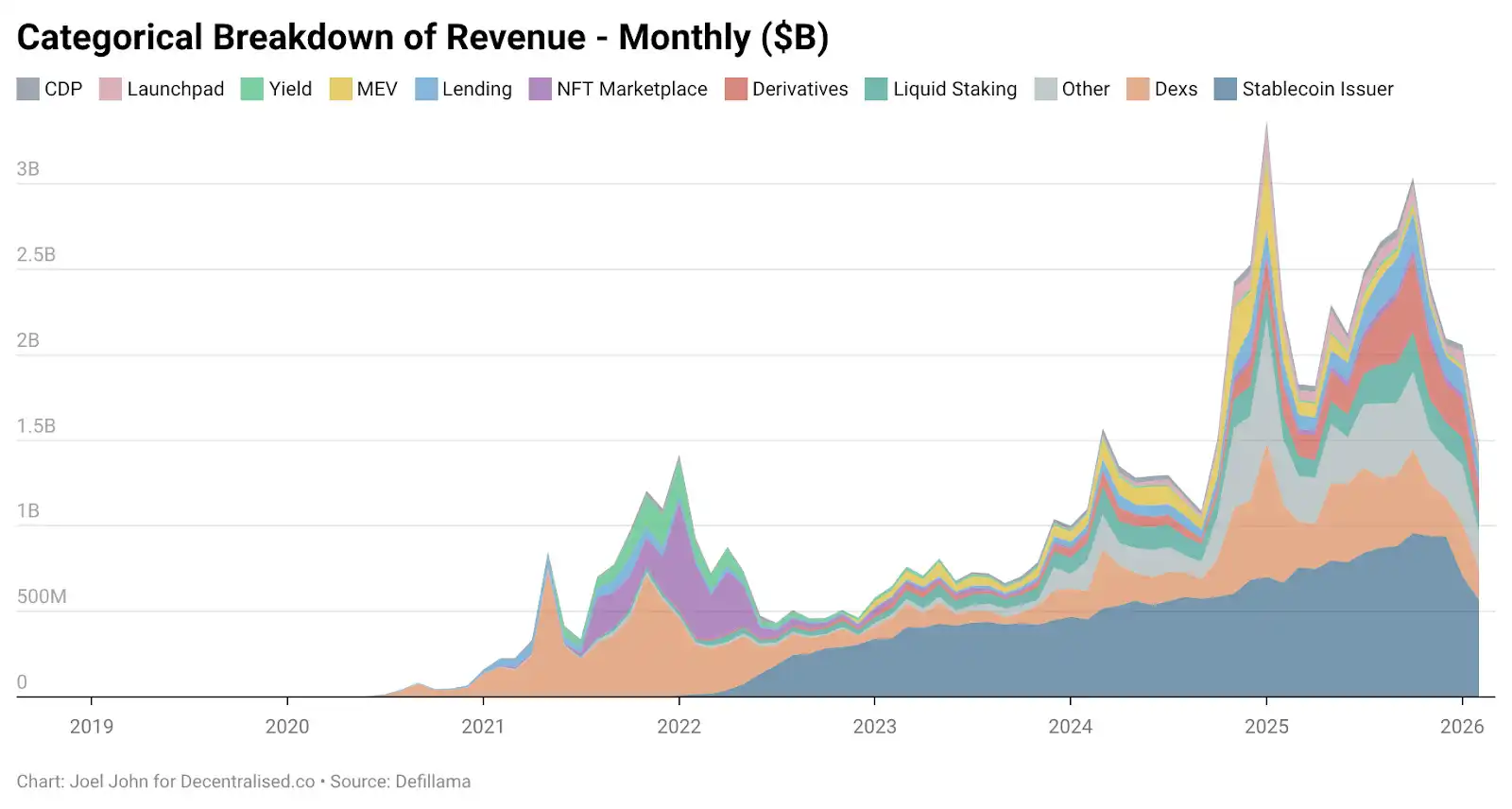

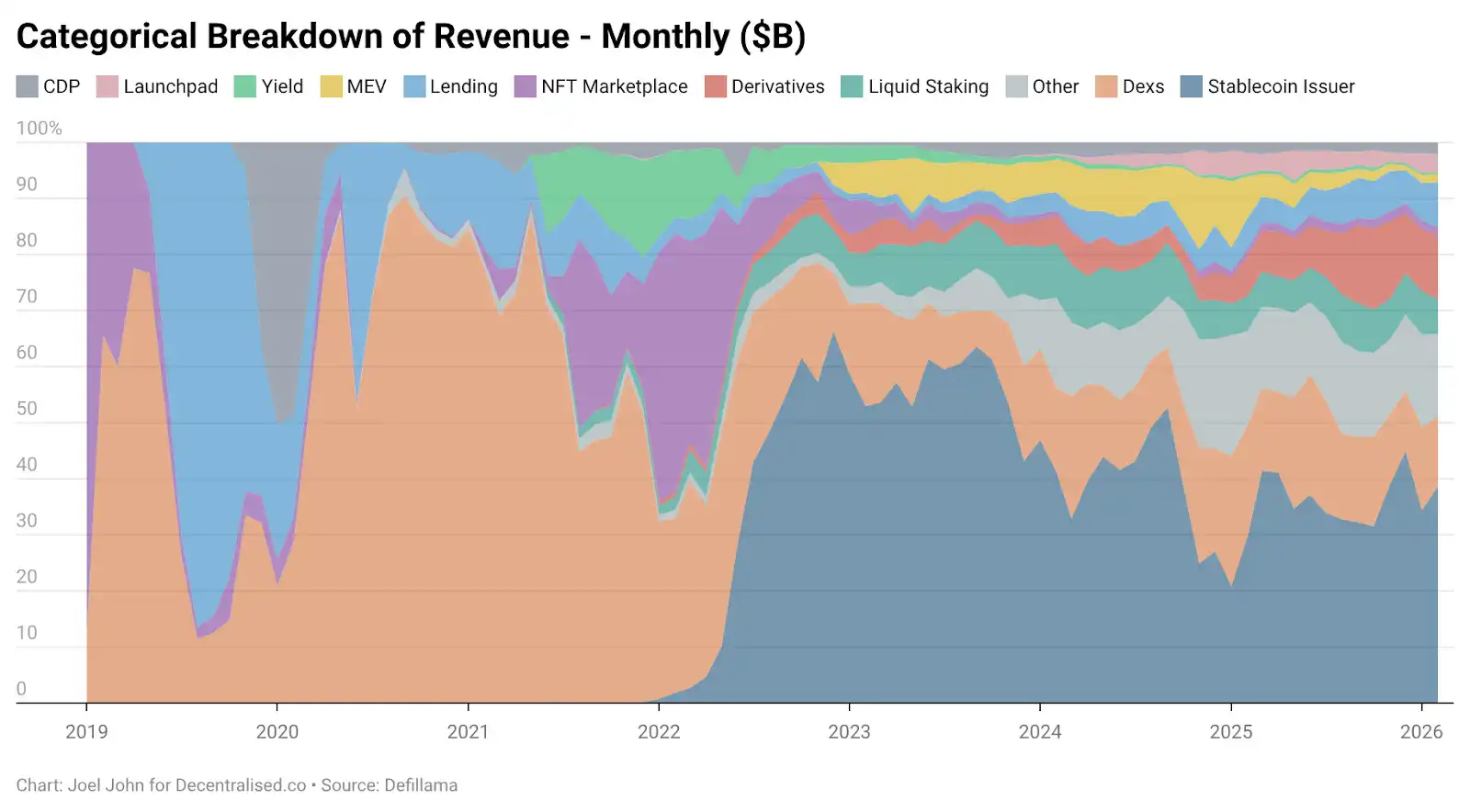

The chart below provides some clues.

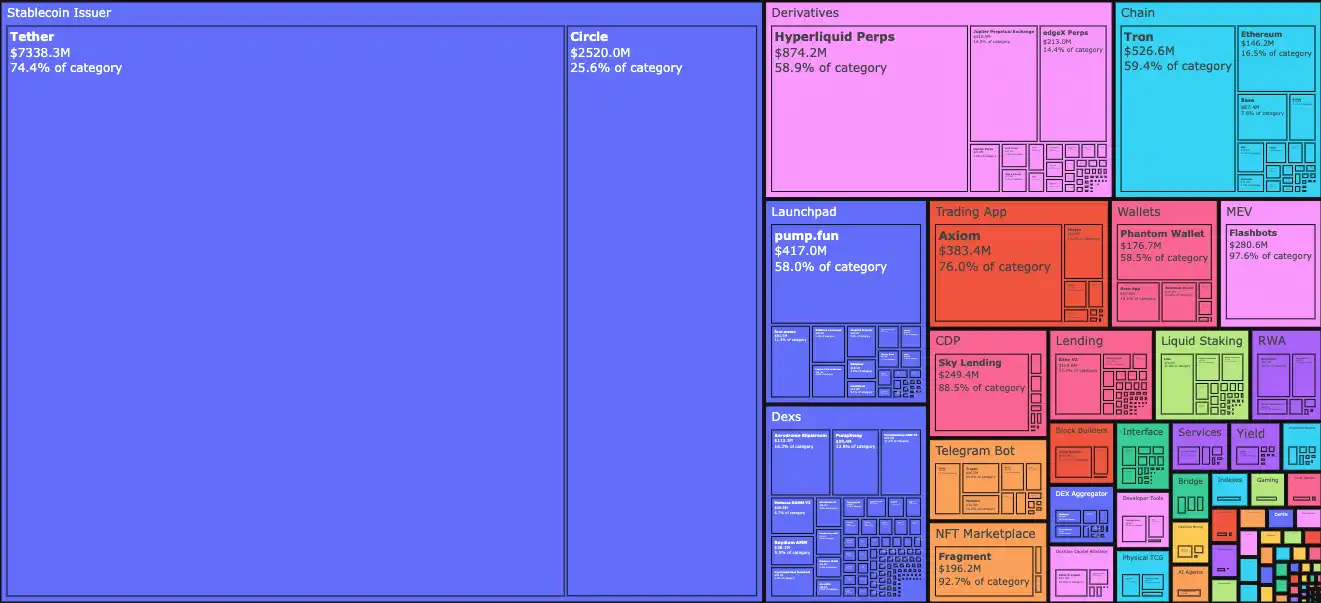

In January 2026, stablecoin issuers Tether and Circle accounted for 34.3% of all fees. In other words, for every $1 earned by this industry, $0.34 flowed to these two companies. Driven by US Treasury bills (T-bills), their revenue grew from $4.95 billion in January 2023 to $9.89 billion in 2025. For bank-scale financial products, this is purely startup-level growth speed. Tether's revenue is almost three times that of Circle.

Their rise is attributed to two major factors.

The first is demand. Countries in the Global South consistently need tools to hedge against local inflation and enable free flow of funds. The US dollar, even digital dollars, fills this void, which local currencies cannot. Capital outflow is an inevitable trend.

The second is the cost structure. The blockchain bears all the costs required to operate a stablecoin business. Unlike traditional banks or fintech companies, Tether and Circle do not need to hire employees proportional to the scale of stablecoins issued on-chain. The marginal cost of issuing the next $1 billion on-chain and transferring the next $100 billion between addresses is almost zero.

These two forces intertwine. On one hand, demand drives stablecoin issuance, with citizens voting with real money; on the other hand, the cost curve flattens. Together, they make stablecoin issuance one of the most capital-efficient businesses in financial history.

The stablecoin business requires building moats in liquidity, compliance, and the Lindy Effect (PANews Note: For things that do not naturally die out, such as a technology or an idea, their expected lifespan is proportional to how long they have already existed. That is, for every additional period they survive, their remaining expected lifespan increases a bit). Very few issuing institutions can withstand multiple cycles. Tether and Circle account for almost 99% of all stablecoin issuance revenue. Why is this? Both assets benefit from their first-mover advantage. The network effects from being integrated into multiple exchanges赋予 them "legitimacy," which technology alone cannot achieve.

Tether was initially launched on the Omni platform as a sidechain. It was slow and cumbersome but accessible through channels commonly used by OTC desks and exchanges. This was a distribution moat, not a technological one. Crypto-native founders often struggle to replicate this moat with code alone.

Stablecoins benefit from the Lindy Effect.

Soon, another category of cryptocurrency will also benefit from a distribution moat.

The market now only needs a hint of liquidity

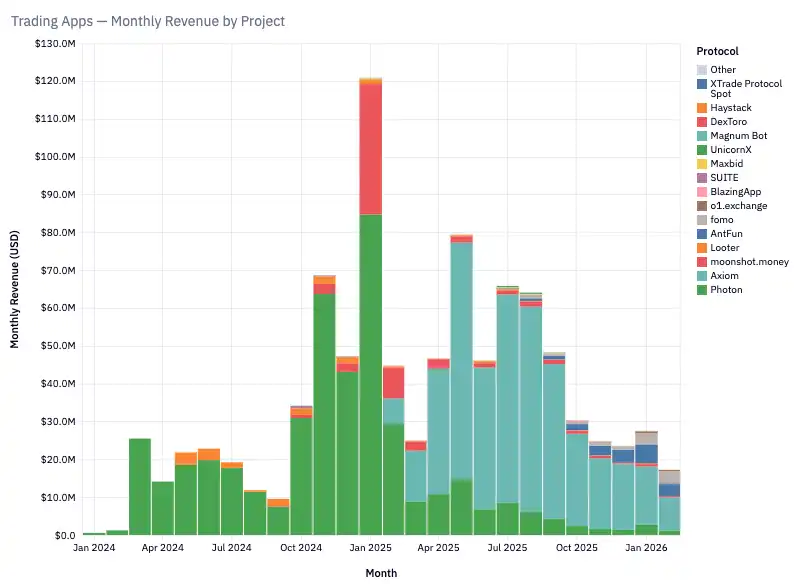

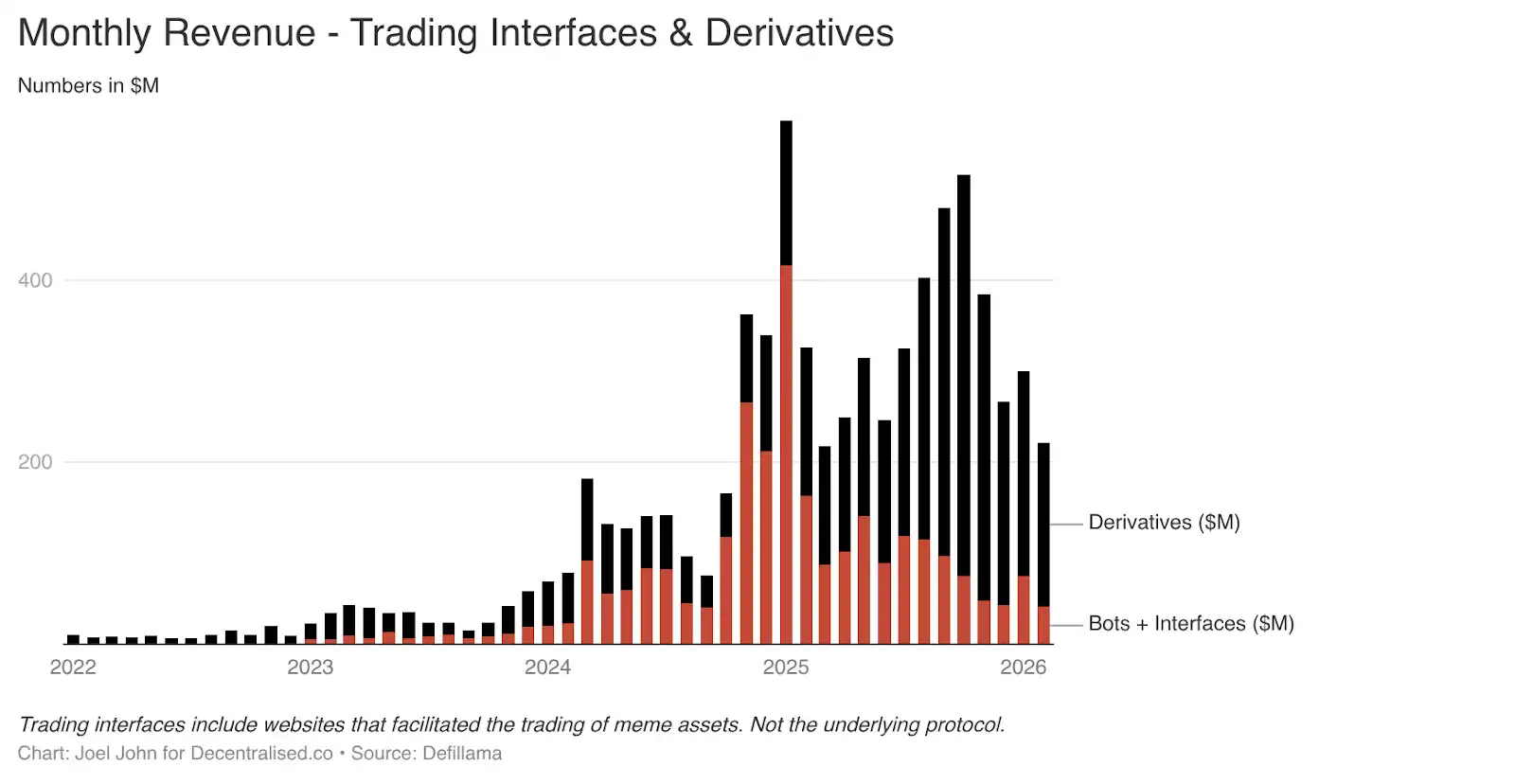

The view that "cryptocurrency is a trading economy" was outlined in two previous articles. One was "Fund Flows," and the other was "Everything is a Market" written last year. What wasn't anticipated at the time was how fast trading products built around Telegram trading bots and trading interfaces would grow.

These two areas alone contributed $575 million in fees by January 2025. Given consumer demand, this is understandable. Meme coin trading and perpetual contracts allow users to profit quickly. In pursuit of quick returns, they are willing to pay high fees. This category grew from 1% of total revenue in 2022 to just over 15% in 2025.

Products like TryFomo and Moonshot have created millions in revenue by focusing on end-users. These products are not technically complex. Instead, their advantage lies in aggregating crypto-native underlying elements and bundling them to create a better user experience. Thanks to the maturity of tools like Privy, developers no longer need to incentivize liquidity or bother managing wallets.

Those native features we were excited about in 2022 have now matured. Applications like BullX and Photon are built on these capabilities. This field alone generated approximately $1.93 billion in trading fees from January 2024 to February 2026.

Meme assets have a fatal flaw: they are functionally thin and highly cyclical. Does that sound familiar? That's because NFTs and Web3 games experienced similar explosive growth and eventual collapse. This cyclicality is both a flaw and a feature of the crypto industry. We will revisit this topic later. For now, let's clarify where the revenue is flowing.

Perpetual futures exchanges (and later prediction markets) represent new avenues with longevity. PumpFun democratized asset issuance through Meme coins, but this game is not fair.

Eventually, the market realized that Meme coins would die out. The dream of becoming a millionaire by buying a coin named "ShibaInuYouShouldShareThisNewsletter" also faded. People don't want to manage random token portfolios; they want to take risks. Perpetual exchanges恰好满足了他们的需求.

You can trade Bitcoin, Solana, or Ethereum with extremely high leverage. Market makers and traders needing an alternative to centralized trading channels flocked in. The core product of this category is liquidity. Hyperliquid dominates because its order book depth is comparable to centralized exchanges. Without this parity, users have no reason to migrate. Over the past three years, Hyperliquid and Jupiter have captured the majority of fees in this category.

Perpetual exchanges and trading platforms have彻底揭开了加密货币的神秘面纱. They clearly show: making small fees from high-frequency trading is the real way to profit. These "Meme trading platforms" and perpetual exchanges are like dopamine machines that package and sell risk.

One of them will develop into core financial technology, used by people around the world to trade commodities, stocks, and digital assets, even on weekends. Blockchain-native applications replicate the functions long provided by Robinhood and Binance: channels for risk-taking.

The Demise of Protocols

Notice we haven't mentioned protocols yet? That foundational layer recording all internet money flows? That's because their story is completely different (but equally important). They are victims of the novelty premium, which is gradually fading.

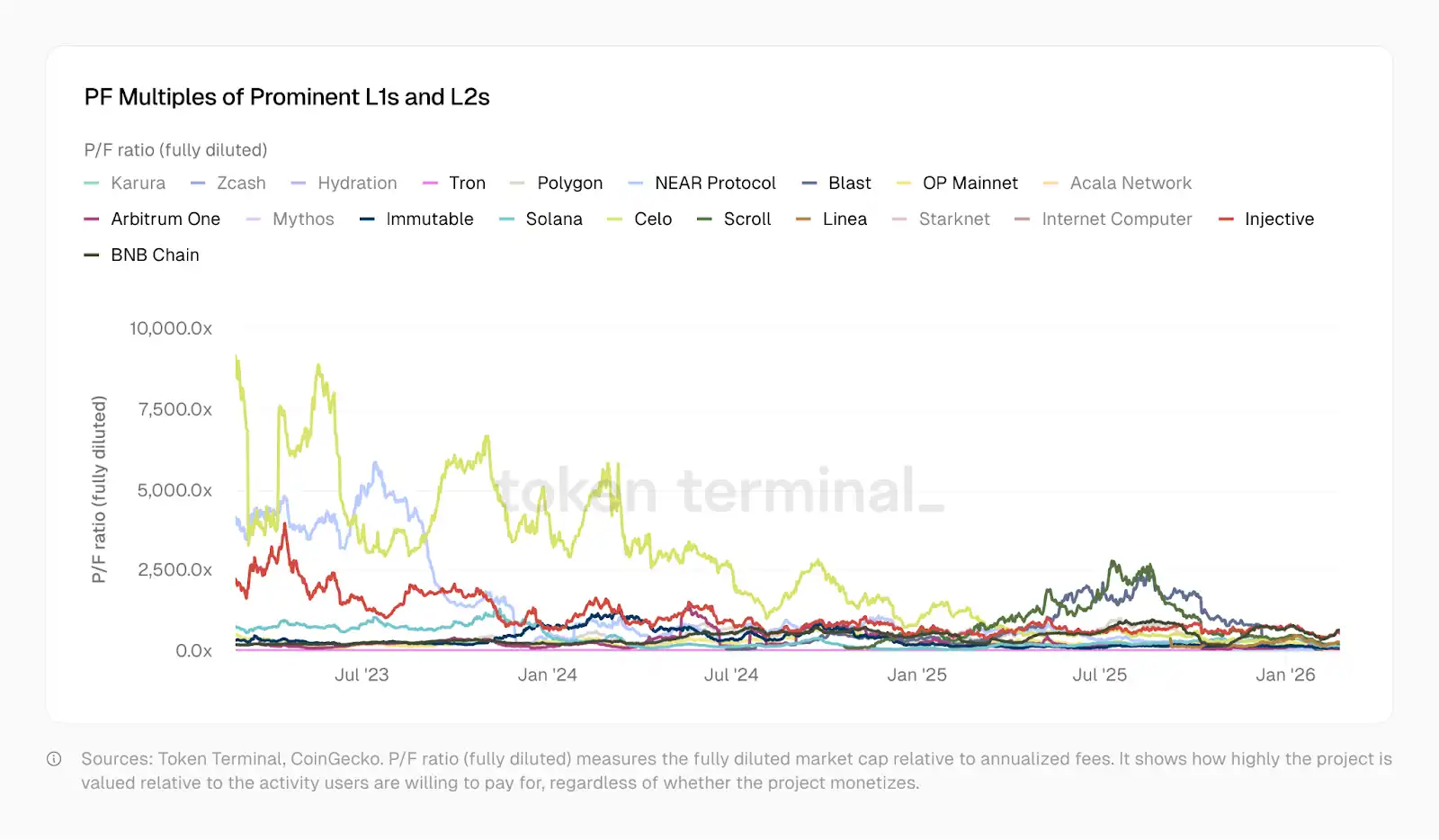

In January 2023, Optimism's P/F (Price-to-Fee ratio) was 465x, Solana's was 706x, Arbitrum and BNB were around 206x. Today, Solana is at 138x, Arbitrum at 62x, OP at 37x. Polygon trades closer to a fintech company, at 20x. Tron, which supports the stablecoin ecosystem, has a P/F of 10.2x. Since then, Optimism, Solana, Arbitrum, and Polygon have each implemented more complex products. They each have more users, better liquidity, and a more sophisticated suite of financial applications built on them.

The discount in their P/F ratios reflects the market's view of them.

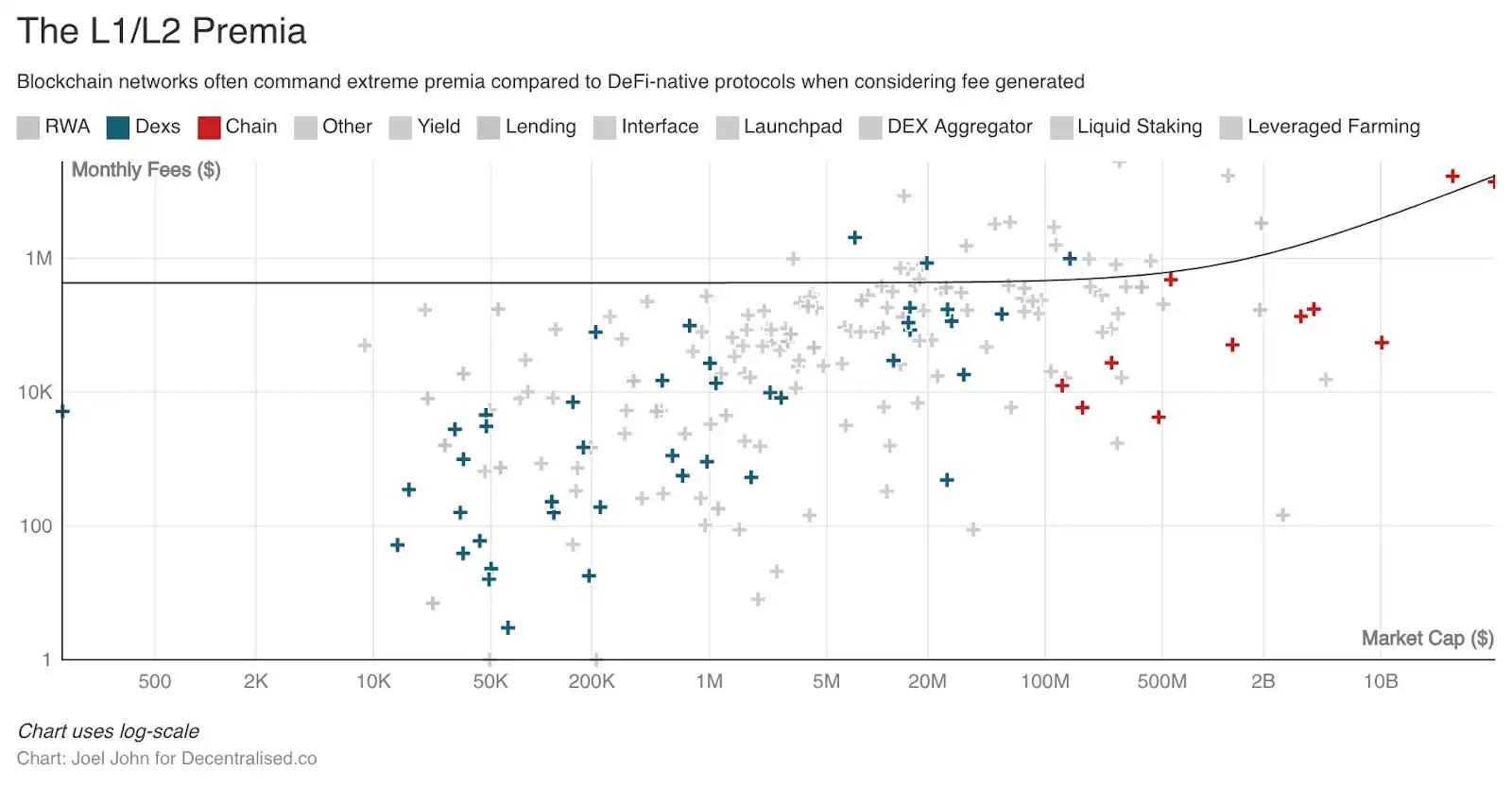

Historically, L1s and L2s have traded at extremely high premiums compared to standalone infrastructure or projects. If this premium had been well invested, it could have created new economic systems. It could have funded developers to build applications that truly matter to ordinary people outside the industry. However, the open-source nature of products and the ease of tokenization led to having fifty copies of the same product on thirty networks,破坏组合性.

That's okay, because we have cross-chain bridges, cross-chain messaging, and countless other fund transfer mechanisms. And the value of all these mechanisms is now declining.

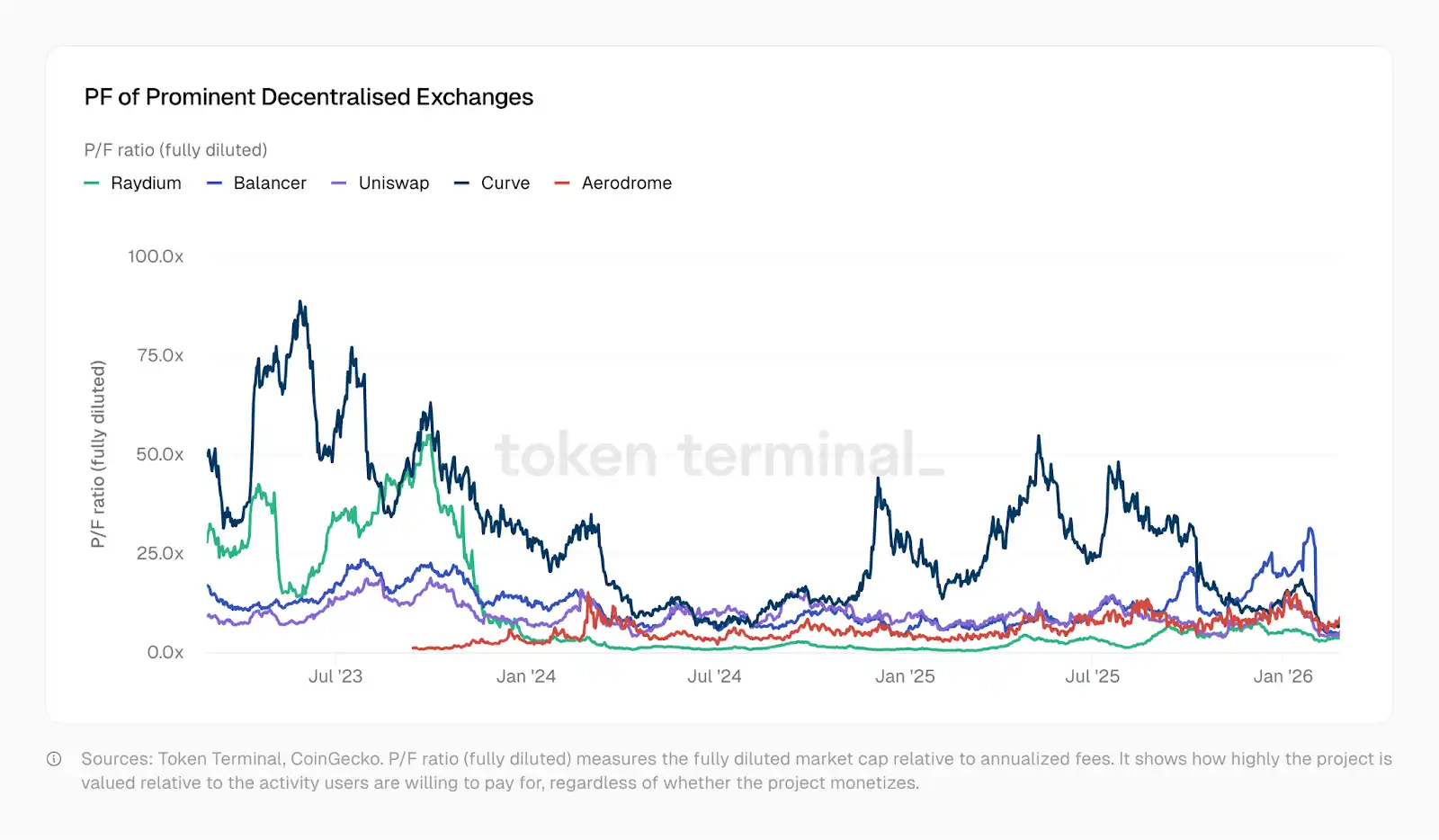

Take the fate of foundational DeFi projects as an example. Investor choice overload and lack of novelty led to a plunge in valuations, even though these foundational projects did drive more economic activity. These markets are highly fragmented, with investors having numerous choices to bet on. The novelty of "decentralization" or "blockchain-based" has long worn off. Projects like Kamino, Euler, Fluid, Meteora, and PumpSwap emerged, but their price-to-fee ratios were all lower than those of 2022 protocols. As shown in the TokenTerminal chart below, the price-to-fee multiples for DEXs fell sharply between 2023 and 2025. Some exchanges now have price-to-fee multiples as low as 1.

In other words, the market values them below the fees they generate in a year. A strange paradox emerges: although the valuations of underlying protocols (whether DeFi or L1 itself) are trending downward, applications built on these protocols are generating higher revenue in a shorter time.

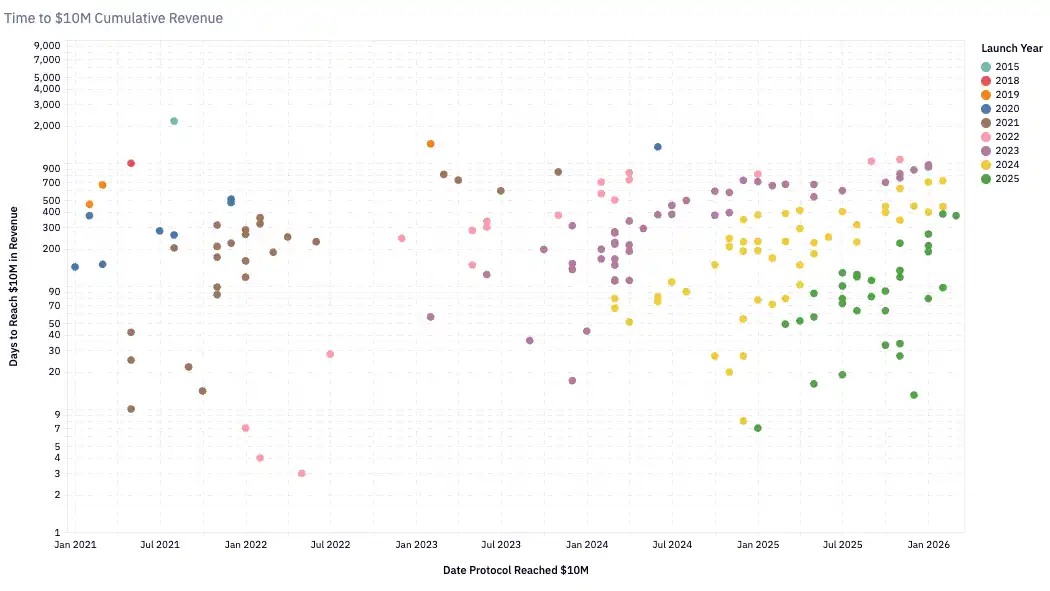

Since early 2020, the number of teams with quarterly revenue exceeding $1 million has grown steadily, now exceeding one hundred. In 2020, protocols that took 24 months to reach $10 million in annual revenue were considered fast-growing. By 2024, the time for protocols to reach this milestone had shortened to about six months. Pump.Fun launched in early 2024 and took about two months to reach $10 million in revenue, setting the record for the fastest growth rate.

This accelerated growth reflects both the maturity of the underlying infrastructure (faster chains, lower transaction costs) and the expanding pool of on-chain capital (seeking yield and entertainment). If you are a developer or founder, consider the following facts:

-

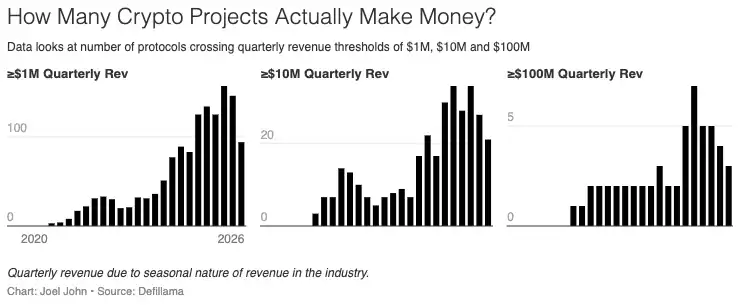

Today's crypto market has nearly 900 revenue-generating protocols.

-

Each protocol is competing for an increasingly smaller median share of revenue, but looking at broader trends, more and more teams are generating revenue. For reference, the number of revenue-generating protocols has grown nearly 8-fold, from 116 to 889.

-

The median monthly revenue has fallen to $13,000.

Blockchain-native businesses have three forms of moats. Each is evident when studying their revenue models.

-

First-Mover Advantage: The network effects gained by Tether and Circle through early advantage are difficult to replicate. Despite constant new entrants, they have weathered multiple cycles and established a duopoly. Currently, these businesses are not tokenized and are highly financialized. Tether is a centralized entity whose revenue primarily comes from US Treasuries.

-

Liquidity Moat: In an industry where capital has historically been utilitarian, Aave has been able to maintain liquidity depth across cycles. Hyperliquid also seems to have achieved this, but it's too early to tell. These protocols have an incentive to return funds to liquidity providers and shift tokens towards governance functions.

-

Distribution Moat: Cyclical applications (like Meme coin trading platforms) rely on capital velocity and consumer demand. Web3 games and NFTs are good examples. AI-powered productivity will mean that lean, small teams can now launch consumer-facing products faster. Where does the advantage come from? Ultimately, it's about onboarding and retaining the most users when the market is hot.

Products built on a distribution moat can be extremely valuable, but they are the exception, not the norm. Traditionally, a startup is valuable because its experience can be replicated. Y Combinator succeeds partly due to the "Lindy Effect" of past successful ideas. Cryptocurrency moves too fast to replicate this Lindy-based experience, which partly explains why we rarely see founders replicating their success in consumer goods across different areas. The cyclical factors that initially helped the business scale may not be replicable.

This doesn't mean founders shouldn't seize these opportunities. Niche areas like prediction markets or data providers for agent economy products might generate significant cash flow in the short term. But it's important to understand that these are high-volatility, short-term games that may not last. The trap for such products is: blindly raising venture capital, or being trapped by a token issued long after the "Meta (core narrative)" that initially gave the product life has died.

So, what makes a tokenized business valuable? Are their valuations reasonable?

The data might provide some clues.

Questioning Governance

In 1999, many tech companies had price-to-sales (P/S) ratios as high as 10x to 20x. Content delivery network company Akamai had a P/S ratio of 7434x. By 2004, Akamai's P/S ratio had fallen to 8x. Many companies saw their P/S ratios plummet from 30x-50x to below 10x. The dot-com bubble burst wiped out trillions in speculative value. However, many companies ultimately survived because their underlying businesses were real. Amazon's stock fell 94% from its dot-com peak but eventually became one of the most valuable companies in history.

The crypto industry is experiencing the same market cap compression, and faster. In 2020, when DeFi was still experimental, the total annual revenue generated by the crypto industry was only about $21 million. The average P/S ratio for all tracked protocols was a staggering 40,400x. The market hype was all about the future: "What could cryptocurrency be?" By 2021, with the arrival of "DeFi Summer," protocol revenue turned into actual earnings, and the P/S ratio plummeted to 338x. Today, with annualized revenue reaching $18 billion, the P/S ratio is about 170x. The P/S ratio compressed from 40,400x to 170x in just five years.

However, there is a problem here. When Visa has a P/S of 18x, shareholders receive dividends and buybacks. They have legal ownership of the company's earnings and governance seats under securities laws. When Aave has a P/S of 4x, token holders have governance rights, but until recently, they had no direct economic rights. Hyperliquid uses its aid fund for buybacks, making HYPE holders the closest thing to equity holders in DeFi. Aave approved a $50 million annual buyback program in 2025.

Do you think I can pass these terrible charts off as art?

These moves are significant, but they are exceptions. In the broader market, most protocols lack mechanisms to return value to token holders. These P/S multiples look low, yet the holder rights are weaker than those in traditional markets. These multiples are possible because the crypto industry creates revenue on a scale and efficiency unmatched by traditional businesses.

The protocols pulling down the crypto P/S ratio are not large organizations with thousands of employees. They are small teams running global financial infrastructure with near-zero marginal costs and no physical offices. How thin can these costs be? And how much trust can holders place in the reasonable use of protocol revenue by these teams?

Segmenting the market by sector provides a clearer picture. Aave, the largest lending protocol in DeFi, has a P/S of about 4x. Hyperliquid controls about 80% of the decentralized perpetual futures market, with a P/S of about 7x. These are not bubble multiples. Arguably, they are even lower than the closest traditional financial counterparts. Coinbase, the only major crypto exchange that is publicly listed, has a P/S of about 9x. CME Group, the world's largest derivatives exchange, has a P/S of about 16x. Visa, as payment infrastructure, has a P/S of about 15x.

Crypto analyst Will Clemente mentioned on a podcast that cryptocurrency is the purest form of capitalism. No industry's successful companies achieve the estimated $100 million profit per employee that Tether does. For context, Nvidia's revenue per employee is $5.2 million, Apple's is $2.4 million, Google's is $2 million. Tether has 125 employees and annual revenue of approximately $12.5 billion, its scale suggests the company has the highest profit per employee in corporate history.

Although the overall 170x P/S number seems crazy, the market is not irrational towards protocols that actually generate revenue. It prices them at or below traditional financial infrastructure.

This leads to the next question: What is the token actually for? In many areas, tokens are powerful tools for concentrating capital and working towards a common vision. Cryptocurrency is at a stage where entrenched duopolies have become the norm. Traditionally, founders had to borrow (pledging equity) or raise funds to inject capital into financial products. Hyperliquid, Uniswap, Jupiter, and Blur have all proven that with token incentives, people will contribute capital to new products. If tokens come with governance rights, these people can contribute even more. In this regard, tokens might evolve two functions:

-

Coordinating capital and resources from the right people;

-

Empowering them to govern the protocol.

Tokens themselves are no longer valuable; even stocks are being tokenized now. These instruments must have claims on economic activity and the ability to guide governance. Many Layer1 and Layer2 tokens struggle with both. Teams and VCs typically hold most of the tokens, leaving retail holders in disarray. This gives ordinary investors little reason to pay attention to newly listed digital assets.

Today, these attempts are showing divergence. MetaDAO allows holders to get a full refund if the team makes false statements. No large protocol has adopted this model yet. The core problem with cryptocurrency is that traditional tokens赋予 holders very few rights. Various protocols are now trying to answer a long-standing question: Why should people hold these assets at all? In a future article, we will explore the correlation between holder rights and valuation.

The Fork in the Road

Over the past two decades, capital markets have become increasingly intertwined. This is largely thanks to technological advancement. We can trade commodities, foreign indices, digital assets, and even computing resources (GPUs) in the near future. Blockchain makes trading in these markets possible globally, anytime, anywhere. Nasdaq and the New York Stock Exchange are now moving towards 24/7 trading models, an example of technology changing the times.

We live in a highly financialized world, ironically, where news of war makes us scramble to find the best prediction markets to bet on.

For founders, this means rethinking the products they build and how they build them. If the data in this article explains anything, it's that all blockchain products ultimately profit through two core principles.

-

By taking small commissions from high-frequency trading, or

-

By taking large commissions on transactions that emphasize verifiability and trust assumptions.

The advantage lies either in transaction speed or in verifiable transparency.

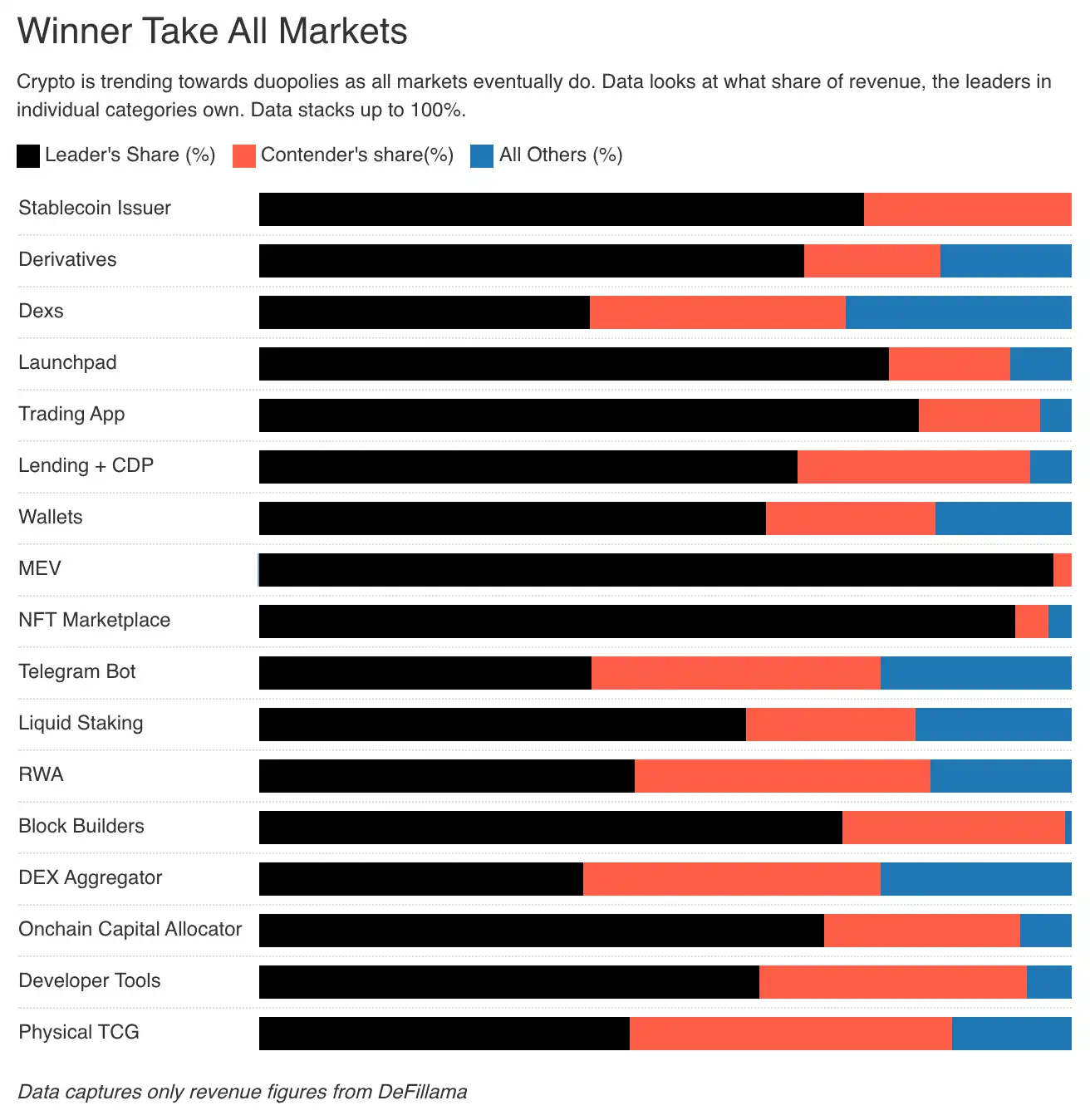

The profit motive is the purest driver for capital market participants. It is widely believed that markets ultimately tend towards extreme efficiency. We see this trend embodied in industry leaders. For example, the charts we see show that 70% of the share in multiple segments is held by two key players. This is the brutal reality we all face, the brutal side of how markets operate. For founders, this means that the funds that once flowed to their tokens are now being reallocated to assets with higher volatility or higher returns on capital.

Long-term capital does exist and may even pay a premium, but only if it recognizes the value of the underlying business. Investors in Google and Amazon don't need to scramble to exit because their underlying businesses are valuable.

In an era where even the value of software itself is questioned, blockchain-native applications will have to find new ways to demonstrate value. We can restructure tokens. Maybe even have startup equity traded on-chain. But this is not just about tokens; it's also about business models. The vast majority of long-tail blockchain applications: such as Web3 social, identity, and gaming products, struggle to scale and achieve meaningful differentiation from traditional competitors. These experiments are not without value; it's that we struggle to monetize them effectively.

The era of building cryptocurrency infrastructure is over. In the future, it will be integrated into the internet. Then, people will no longer talk about "online" businesses; you simply exist on the internet. No one calls themselves a "mobile app developer" anymore; you are simply a developer.

Long live the era of blockchain enthusiasts! We are just advocates of ledger maximization, thinking about how best to utilize these ledgers.

Related reading: 36 Years, 4 Wars, 1 Script: How Does Capital Price the World in Conflict?