By: Zhang Yaqi, Wall Street News

Volatility at the index level for US stocks appears calm on the surface, but internal pressures are building. Under the triple constraints of geopolitical tensions, monetary policy expectations, and signals from the credit market, market fragility has climbed to a multi-year high—and a high-expectation, high-risk earnings season is now kicking off.

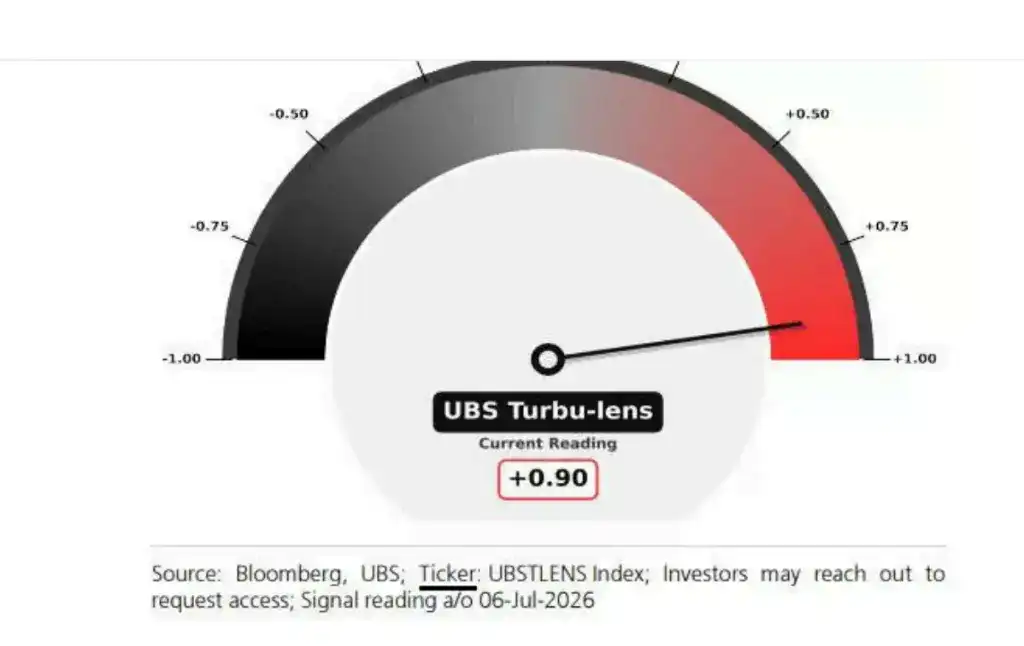

The "Turbu-lens" market fragility indicator from UBS's derivatives strategy team currently reads 0.9 (on a scale from -1 to 1), its highest level since mid-September 2025. Historically, such readings have often preceded a sharp, phased increase in the VIX. UBS derivatives strategist Maxwell Grinacoff's team warns that this indicator points to "extreme market fragility" just as earnings season begins. Meanwhile, the team also noted that if systematic strategies fully add leverage, the reading "could truly touch +1".

High market expectations are further amplifying risks. Analysts expect Q2 earnings growth for S&P 500 index components to be as high as 24%, and 12% for the Europe STOXX 600. Unlike previous earnings seasons, analysts have persistently raised forecasts ahead of the reporting period, a confidence so strong that it conversely implies greater room for adjustment if results disappoint the market.

The VIX is currently at low levels, but this calm is deceptive. Barclays strategist Anshul Gupta's team points out that the recent decline in the VIX coincided with a seasonal calendar window where price volatility typically narrows, representing a "short-lived sweet period" with limited persistence. The onset of earnings season could push the VIX higher again.

More noteworthy is that the subdued index volatility masks extreme divergence within the market—single-stock volatility has exceeded index volatility by more than threefold. Grinacoff noted that the probability of this gap narrowing during the summer is high, at which point either monetary policy repricing or geopolitical disruptions could trigger a sharp spike in index-level volatility.

Regarding hedging strategies, as dispersion trading and sector rotation may persist over the coming weeks of the earnings period, index-level hedging might be limited in its effectiveness. Grinacoff suggests, "Single-stock options perhaps offer better opportunities on a tactical level."

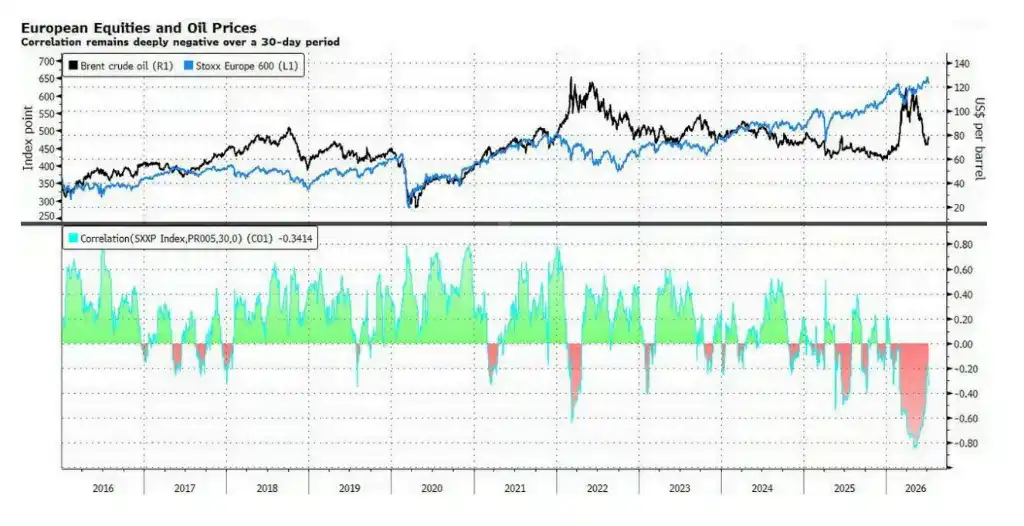

Oil price volatility driven by geopolitical tensions is creating persistent pressure on global equity markets. Brent crude has climbed to just below $80 per barrel, a move that could keep inflation expectations elevated and the Federal Reserve on the sidelines. While expectations for rate hikes saw limited change following the release of the Fed meeting minutes, the 10-year Treasury yield has quietly risen to around 4.6%. Rising bond market volatility is sending a negative signal to global equity markets, or at least capping further upside potential.

Strategists at Citi (including Alice Zheng) noted that current market positioning for higher oil prices is skewed, with Europe being particularly vulnerable—due to its high reliance on imported energy and lower exposure to AI-benefiting assets. "If the oil rally continues, the pullback in European equities could be quite significant, given the market had already largely priced in expectations for the conflict to end," the strategists wrote.

Performance in the credit market sounds a cautionary note for the current equity market upward momentum. Compared to the stock indices' previous surge to record highs, the narrowing of credit default swap (CDS) spreads has been quite limited; the credit market has not fully endorsed the equity rally. As equities have pulled back recently, the two have realigned, but analysts believe that to support a more robust equity market advance, clearer tightening signals from the credit market are needed.

Facing the above risks, UBS recommends investors capture stock-specific volatility opportunities through pair-wise correlation trades. In terms of sectors, UBS believes the Technology, Energy, and Financial sectors in the US market are most suitable for setting up pair-wise volatility trades, while in Europe, the Energy, Technology, and Consumer Discretionary sectors are recommended.