Original Title: DTCC Isn't Tokenizing Shares, Here is What's Actually Changing

Original Author: @ingalvarezsol

Original Compilation: Peggy, BlockBeats

Editor's Note: The "tokenization" promoted by DTCC is not about putting stocks on-chain, but rather a digital upgrade of securities entitlements, with the core goal of improving the efficiency and settlement capabilities of the existing market system. Parallel to this is another, more radical path: tokenizing stock ownership itself, reshaping self-custody and on-chain composability.

These two models are not opposed; they serve different purposes—stable scaling and functional innovation, respectively. This article attempts to clarify this distinction and points out that the real change is not about one replacing the other, but about investors beginning to have the right to choose between different ownership models.

The full text is as follows:

Introduction: Tokenization, But Not the Kind You Think

The Depository Trust & Clearing Corporation (DTCC) has received a no-action letter from the U.S. Securities and Exchange Commission (SEC), allowing it to begin tokenizing its securities infrastructure. This is a significant upgrade to the "plumbing" of the U.S. capital markets: DTCC custodies approximately $99 trillion in securities assets and supports annual trading volumes in the quadrillions of dollars.

But the market reaction to this news reveals a clear gap between expectations and reality. What is being tokenized is not "stocks," but security entitlements—and this difference determines the nature of almost all subsequent issues.

Current discussions about "tokenized securities" are not herald a single, monolithic future, but rather the simultaneous emergence of two different models at different levels: one is an internal改造 of the existing indirect holding system to improve how securities are held and transferred; the other is a fundamental reshaping of what it means to "own a share of stock."

Note: For ease of expression, the following text will not distinguish between DTCC's subsidiary DTC (Depository Trust Company) and its parent company DTCC.

How Securities Ownership Actually Works Today

In the U.S. public markets, investors do not directly hold shares with the listed company. Stock ownership is placed within a chain of multiple intermediaries.

At the bottom is the issuer's shareholder register, typically maintained by a transfer agent. For almost all listed stocks, this register usually records only one name: Cede & Co., the nominee holder designated by DTCC. The purpose is to avoid the issuer having to maintain records for millions of individual shareholders.

One level up is DTCC itself. It "immobilizes" the physical movement of these shares through centralized custody. DTCC's direct participants are called clearing brokers, who represent retail brokers面向终端客户, handling custody and clearing/settlement. What DTCC records in its system is: how many shares each participant "is entitled to."

At the top are the investors themselves. Investors do not hold specific, identifiable shares, but rather a legally protected security entitlement—this is their claim against their broker; and the broker, through the clearing broker, holds corresponding entitlements within the DTCC system.

What is being tokenized this time is these "entitlements" within the DTCC system, not the shares themselves.

This upgrade can indeed improve system efficiency, but it cannot solve the fundamental limitations inherent in the multi-layered intermediary structure itself.

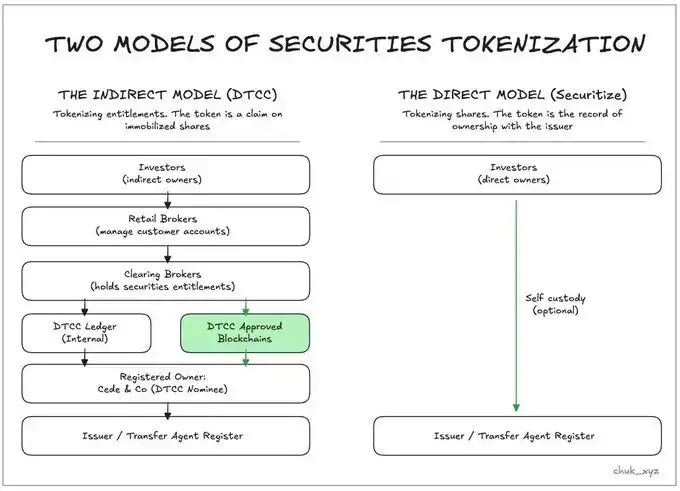

DTCC tokenizes "claims," while the direct model tokenizes "the shares themselves." Both are called "tokenization," but they solve completely different problems.

Why Upgrade?

The U.S. securities system is quite robust, but its architecture still has significant limitations. Settlement relies on processes with time delays and limited operating hours; corporate actions (like dividends, stock splits) and reconciliation are still mostly done through batch messaging rather than shared state. Because ownership is nested within a complex network of intermediaries—each layer with its own pace of technological upgrade—real-time workflows are almost impossible without simultaneous support from all levels, and DTCC is a key "choke point" in this system.

These design choices also bring capital commitment issues. Long settlement cycles require tens of billions of dollars in margin to manage risk between trade execution and final settlement. These optimization schemes were originally designed for an old world where "capital transfer was slow and expensive."

If the settlement cycle is shortened, or instant settlement is achieved for voluntary participants, the required capital scale will decrease significantly, costs will随之降低, and market competition will intensify.

Some of these efficiency gains can be achieved by upgrading existing infrastructure; but others—especially those involving direct ownership and faster innovation iteration capabilities—require a completely new model.

Tokenizing the Existing System (DTCC Model)

In the DTCC path, the underlying securities remain in centralized custody and continue to be registered in the name of Cede & Co. What actually changes is the form of expression of the entitlement records: these "entitlements," which originally existed only on proprietary ledgers, are given a "digital twin" token on an approved blockchain.

This is important because it enables modernization without颠覆 the existing market structure. DTCC can introduce 24/7 entitlement transfers between participating institutions, reduce reconciliation costs, and gradually push these entitlements towards faster collateral liquidity and automated workflows, while still retaining efficiency advantages of centralized systems like net settlement.

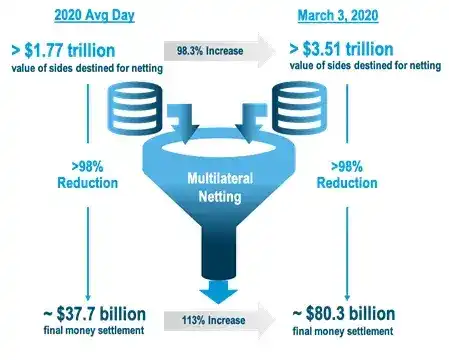

Multilateral netting can compress total trading activity worth trillions of dollars into a final settlement amount of only hundreds of billions. This efficiency is core to today's market structure, even as new ownership models are gradually emerging.

But the boundaries of this system are deliberately set. These tokens will not make the holder a direct shareholder of the company. They are still permissioned, revocable claims, existing within the same legal framework: they cannot become freely composable collateral in DeFi, cannot bypass DTC's participating institutions, and will not change the issuer's shareholder register.

In short, this approach is about optimizing the system we already have, while fully retaining the existing intermediary structure and its efficiency advantages.

Tokenizing "Ownership Itself" (Direct Model)

The second model starts precisely where the DTCC model cannot reach: it tokenizes the shares themselves. Ownership is recorded directly on the issuer's shareholder register, maintained by the transfer agent. When the token is transferred, the shareholder of record changes accordingly, and Cede & Co. is no longer in the chain of ownership.

This unlocks a range of capabilities that are structurally impossible under the DTCC model: self-custody, direct relationships between investors and issuers, peer-to-peer transfer, and programmability and composability with on-chain financial infrastructure—including collateralization, lending, and many new financial structures yet to be invented.

This model is not just theoretical. Galaxy Digital shareholders can already tokenize their equity through Superstate and hold it on-chain, directly reflected in the issuer's cap table. By early 2026, Securitize will also offer similar capabilities, with 24/7 trading supported within compliant brokerage systems.

Of course, the trade-offs of this model are equally real. Once outside the indirect holding system, liquidity becomes fragmented, and the efficiency of multilateral netting disappears; brokerage services like margin and lending need to be redesigned; operational risk shifts more to the holder themselves, rather than intermediaries.

But it is the agency brought by direct ownership that allows investors to actively choose whether to accept these trade-offs, rather than passively inheriting them. And within the DTCC framework, this choice space barely exists—because any innovation regarding "entitlements" must pass through layers of governance, operations, and regulatory processes sequentially.

There are key differences between these two models. The DTCC model has much stronger compatibility and scalability with the existing system; while the direct ownership model opens up greater space for innovations like self-custody.

Why They Are (For Now) Not Competing Visions

The DTCC model and the direct ownership model are not competing routes; they solve different problems.

DTCC's path is an upgrade to the existing indirect holding system, preserving core advantages like net settlement, liquidity concentration, and systemic stability. It targets institutional participants who need scale, settlement certainty, and regulatory continuity.

The direct ownership model meets another set of needs: self-custody, programmable assets, and on-chain composability. It serves investors and issuers who want entirely new functionalities, not just a "more efficient pipeline."

Even if direct ownership may reshape market structures in the future, this transformation will必然 be a multi-year process, requiring同步推进 in technology, regulation, and liquidity migration; it cannot happen quickly. The pace of clearing rules, issuer behavior, participant readiness, and global interoperability moves much slower than the technology itself.

Therefore, a more realistic prospect is coexistence: modernization of infrastructure on one side, and innovation in ownership on the other. Today, neither can替代 the other in fulfilling its mission.

What This Means for Different Market Participants

These two tokenization paths affect participants at different levels of the market differently.

Retail Investors

For retail users, the DTCC upgrade is almost imperceptible. Retail brokers have long shielded users from most friction (e.g., fractional shares, instant buying power, weekend trading), and these experiences will still be provided by brokers.

What真正带来变化 is the direct ownership model: self-custody, peer-to-peer transfer, instant settlement, and the possibility of using stocks as on-chain collateral. Today, stock trading has begun to appear through some platforms and wallets, but most implementations still rely on a "wrapped/mapped" form. In the future, these tokens could potentially become real shares on the register, not a synthetic layer.

Institutional Investors

Institutions will be the biggest beneficiaries of DTCC's tokenization. Their operations heavily rely on collateral movement, securities lending, ETF flows, and multi-party reconciliation—areas where tokenized "entitlements" can significantly reduce operational costs and increase speed.

Direct ownership is more attractive to some institutions, especially opportunistic trading firms seeking programmable collateral and settlement advantages. But due to liquidity fragmentation, broader adoption will start from the edges of the market.

Brokers and Clearing Institutions

Brokers are at the center of the transformation. Under the DTCC model, their role is further strengthened, but innovation moves towards them: clearing brokers who率先 adopt tokenized entitlements can differentiate themselves, and vertically integrated institutions can directly build new products.

In the direct ownership model, brokers are not "removed," but reshaped. Licensing and compliance are still necessary, but a cohort of native on-chain intermediaries will emerge, competing with traditional institutions for users who value the characteristics of direct ownership.

Conclusion: The Real Winner is "Choice"

The future of tokenized securities is not about one model winning out, but about how the two models evolve in parallel and connect with each other.

Entitlement tokenization will continue to modernize the core of public markets; direct ownership will grow on the periphery where programmability, self-custody, and new financial structures are more valued. Switching between the two will become increasingly smooth.

The end result is a broader market interface: existing tracks are faster and cheaper, while new tracks emerge for new behaviors that the existing system cannot support. Both paths will produce winners and losers, but as long as the direct ownership path exists, investors are the ultimate winners—gaining better infrastructure through competition and having the right to freely choose between different models.

Recommended Reading:

Why Isn't Asia's Largest Bitcoin Treasury Company Metaplanet Buying the Dip?

Multicoin Capital: The Era of FinTech 4.0 Has Arrived

a16z's Heavily Funded Web3 Unicorn Farcaster Forced to Pivot, Is Web3 Social a False Proposition?