Source: Wintermute

Author: Jasper De Maere

Compiled and Edited by: BitpushNews

Bitpush Note:

As a leading market maker in the crypto industry, Wintermute handles daily trading volumes amounting to hundreds of billions of dollars. Compared to ordinary researchers, they can penetrate the fog and see the most authentic flow of retail funds. In this latest report, Wintermute raises an alarming point for the crypto circle: the "retail faith" that once supported the crypto market is wavering. In the past, cryptocurrencies and stocks typically rose and fell together, but starting from late 2024, this relationship completely reversed—retail investors began making a "choose one" single choice between the two.

Below is the main text:

Retail activity drives the cryptocurrency market. Through speculation, reflexive buying on dips, and agile capital rotation within the token world, retail investors define every major market cycle. However, new data indicates that the relationship between retail investors and cryptocurrencies is changing. For some time, we have observed that the stock market is attracting retail attention at the expense of altcoins. New data from J.P. Morgan's strategy department, combined with our own flow data, now suggests that stocks and cryptocurrencies are increasingly becoming complementary risk assets.

Core Viewpoints

-

Reversal Phenomenon: Retail investment activity in cryptocurrencies and stocks used to move in the same direction. But since late 2024, the two have shown an inverse relationship: when retail buys stocks, they remain quiet in the cryptocurrency market, and vice versa.

-

Volatility Premium Compression: The volatility premium of cryptocurrencies relative to stocks, which was once their biggest attraction to retail, is now structurally compressing. Volatility is no longer a product feature with diversification characteristics in cryptocurrency investment.

-

Technology-Driven Factors: Some under-discussed technical reasons are accelerating this shift. For example, easier access to cryptocurrencies has dismantled the "closed audience" effect; meanwhile, large language model (LLM)-driven analysis is narrowing the cognitive advantage gap in the stock market, a phenomenon not yet occurring in the cryptocurrency space.

-

Traditional Indicators Fail: Traditional leading indicators for crypto risk appetite (such as M2 money supply) are failing. Investors should increasingly view cryptocurrencies through the lens of a multi-asset portfolio, similar to other mature asset classes.

Reversal Phenomenon

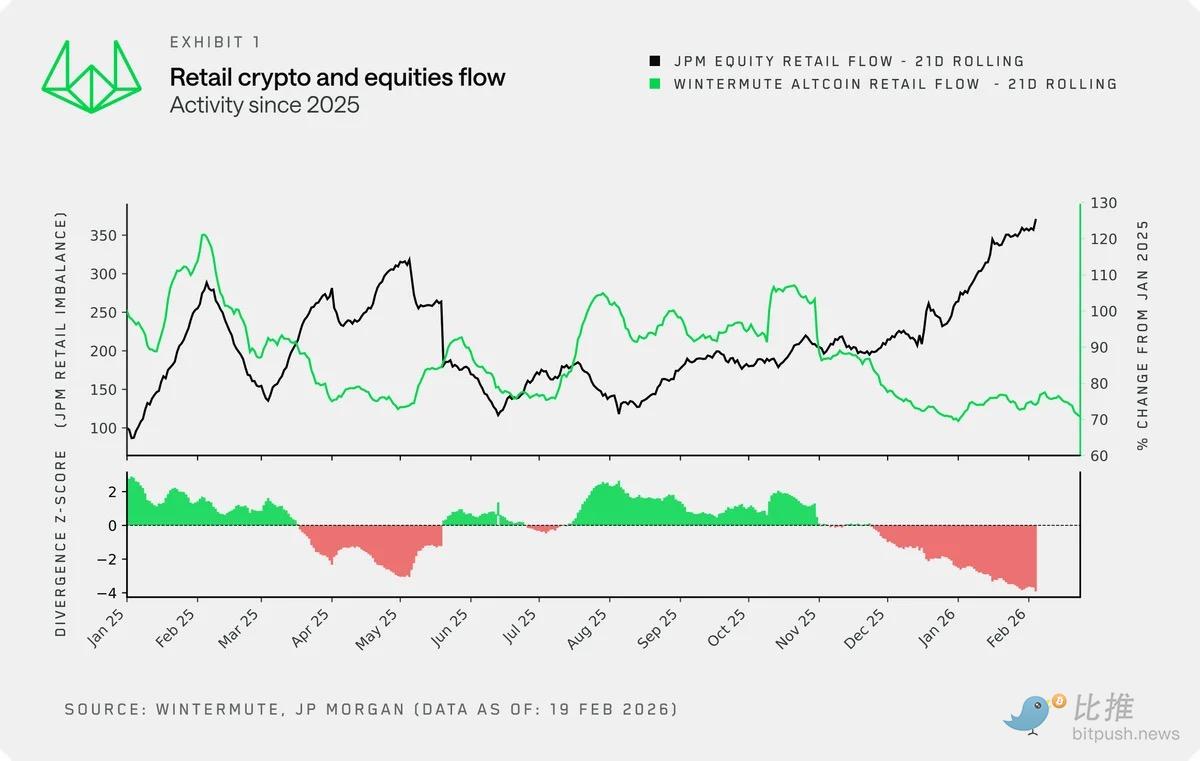

By overlaying Wintermute's proprietary crypto retail flow data with J.P. Morgan's retail stock inflow data, we gain a new perspective on the relationship between retail stock and crypto activity.

Historically, the two have maintained synchronized trends until late 2024. At that time, high risk appetite sentiment drove simultaneous buying in both, as they both served, to some extent, as outlets for excess capital (see M2) and risk appetite.

However, since late 2024, this relationship has broken down: as retail floods into the stock market at an unprecedented pace, they are holding back on cryptocurrencies, and the divergence between the two has now reached historical extremes.

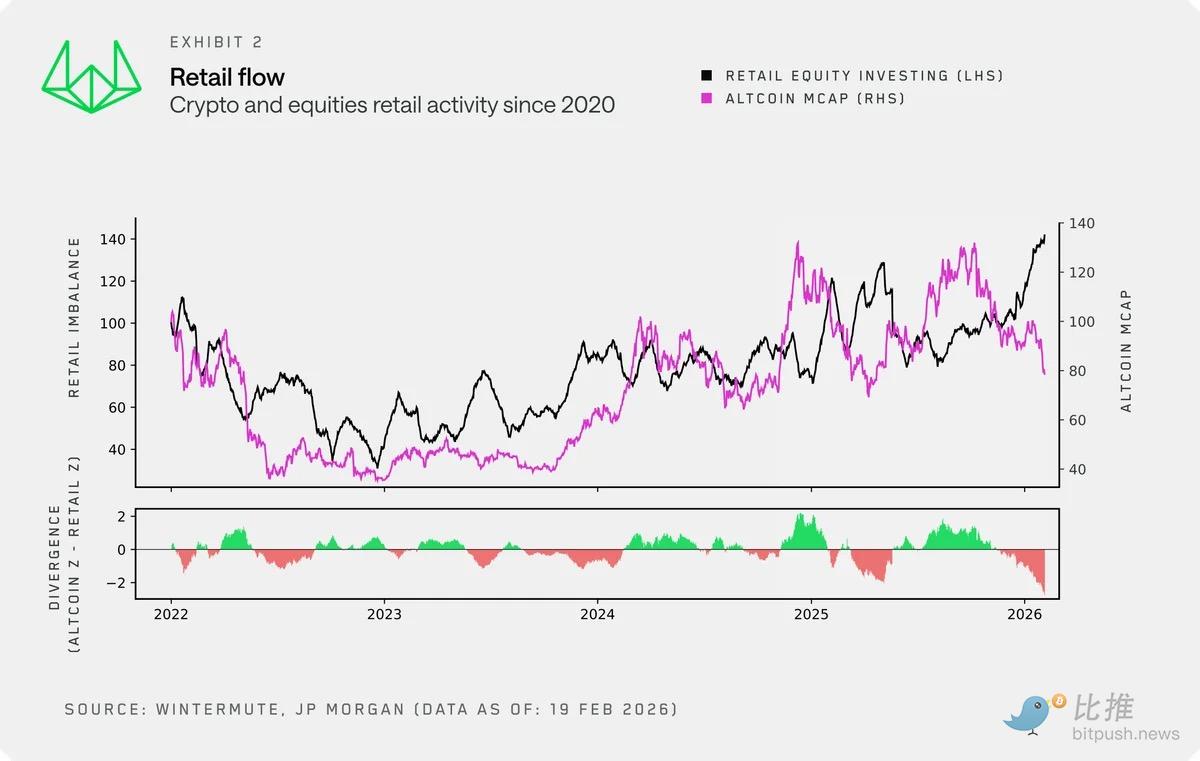

Zooming in, we use altcoin market capitalization as a long-term proxy indicator for retail crypto activity.

It closely aligns with our retail flow data and has an impartial and longer historical record. Between 2022 and late 2024, cryptocurrencies and stocks generally moved in sync, both viewed by the retail sector as a type of high-risk investment portfolio. The decoupling in late 2024 is very noticeable, also indicating that retail activity has become more short-term driven, volatile, and to some extent, lacking in structure.

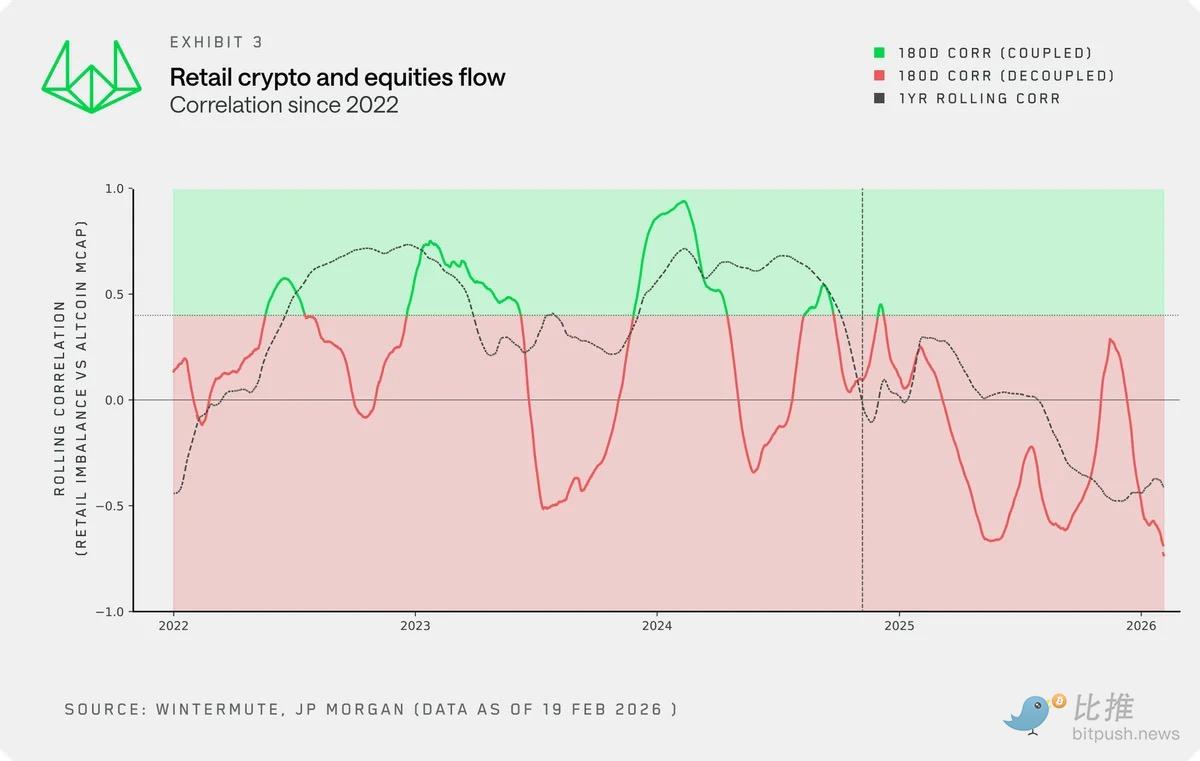

The rolling correlation between retail activity and altcoin market capitalization confirms this shift. The once volatile but generally positive relationship has turned negative. Retail is now allocating between the two, rather than injecting funds into both simultaneously.

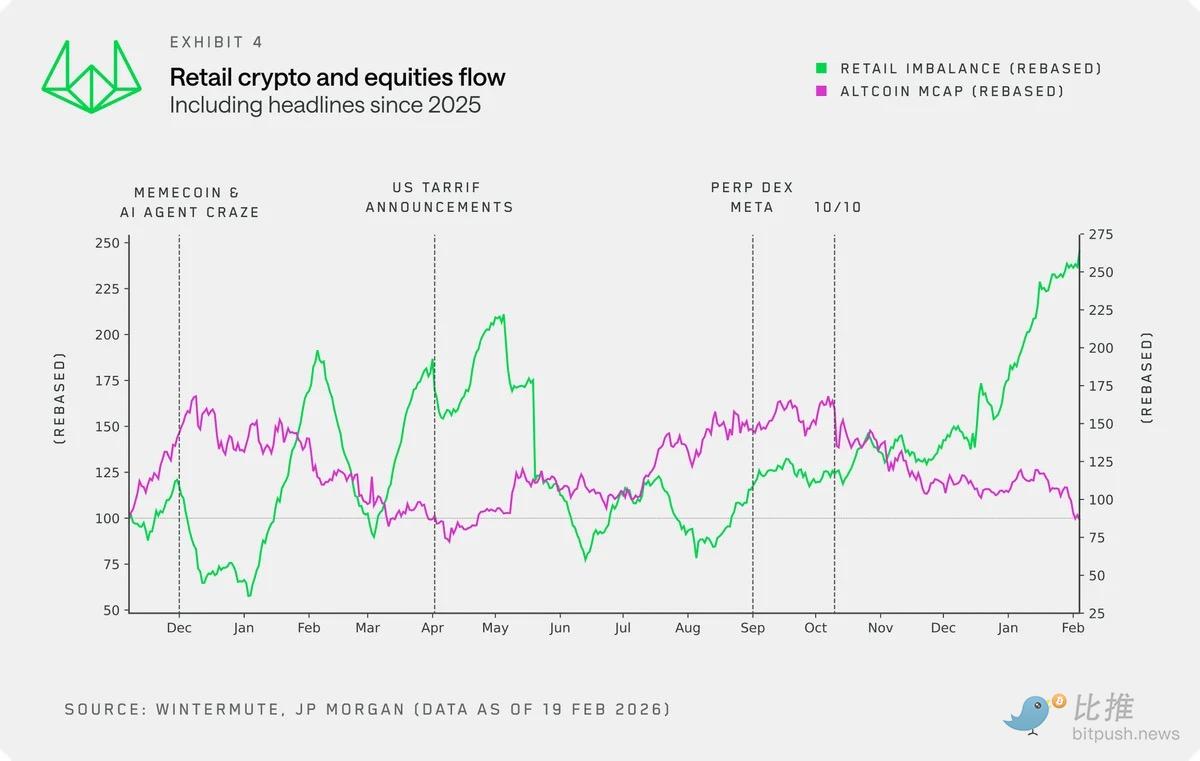

Focusing on 2025 and overlaying key catalysts makes this dynamic clearer. Several points are noteworthy:

-

Memecoins and AI agents had their moments in the spotlight when stock market activity stalled, as retail found speculative outlets elsewhere.

-

Retail continued to aggressively buy the dip in the stock market, both during the tariff policy announcement in April 2025 and in recent market volatility.

-

After October 10th, the market almost completely shifted towards stocks, and this trend continues currently.

Causality

The rolling correlation between retail activity and altcoin market capitalization confirms this shift. The once volatile but generally positive relationship has turned negative. Retail is now choosing between the two, rather than investing in both.

This new data also confirms this. Retail activity in the stock market has become a new variable that cryptocurrency investors should closely monitor to identify windows of opportunity where retail funds might more sustainably flow into cryptocurrencies.

Volatility = The Product Itself

One reason retail is attracted to and remains active in cryptocurrency is the asset's volatility characteristics. Volatility is the product. It was the initial force that drew retail into the crypto space.

However, although the actual volatility of cryptocurrencies still far exceeds that of the stock market, a trend of structural contraction has formed, and this trend is difficult to reverse in the short term. The volatility ratio of BTC to the Nasdaq Index (NDX) continues to decline, even compressing to below 2x in the first half of 2025.

Thoughts on key drivers:

-

Market Maturation: With the increasing presence of sophisticated investors and new liquidity tools like ETFs and DATs, the reflexive volatility peaks that defined earlier cycles have been smoothed out.

-

Market Capacity: At a market capitalization of $2.3 trillion (even 40% below the all-time high), the capital flow required to move the market is far greater than five years ago.

As volatility compresses, the core selling point of cryptocurrencies to retail is also eroding. The "excess volatility" that defined the 21-22 cycle and attracted a generation of retail investors is gone. For retail seeking volatility, stocks are becoming increasingly attractive.

Technology-Driven Factors

In addition to crypto-specific market structure, some under-discussed technical factors are also accelerating this shift.

-

Crypto Access: The integration of crypto trading by fintech and traditional brokerage platforms (or the integration of stock trading by crypto-native platforms) has lowered the entry barrier, but the more profound impact is on "exit." In previous cycles, funds were effectively locked into the crypto space due to on-ramp friction, leading to organic rotation between tokens. Now, the same seamless on/off-ramps mean funds can easily flow between crypto and stocks without significant obstacles.

-

Cognitive Iteration: Retail seems increasingly attracted to the stock market, partly due to a new sense of cognitive advantage unlocked through AI. Large language models have significantly enhanced retail's analytical capabilities, creating a sense of a "level playing field."

-

This feeling is missing in the crypto space. Although analysis based on data is possible, cryptocurrencies lack a consensus valuation framework and token value capture mechanism, coupled with an ever-expanding investable universe, making it difficult for retail to gain that sense of cognitive advantage.

Conclusion

Retail investors, once the most reliable source of self-reinforcing demand for the crypto market, are increasingly satisfying their risk appetite elsewhere.

The stock market not only offers increasingly competitive volatility but also provides a growing sense of analytical advantage, and allows seamless switching to stock trading through apps already on retail investors' phones.

Cryptocurrencies still have a place in retail portfolios, but they are now just one of many choices, no longer the main battlefield for speculation.

This shift should also reshape how investors view the market Some proven traditional indicators have already failed. For crypto investors, merely finding leading indicators for risk appetite combined with a crypto-native framework is no longer sufficient to win. Investors need to increasingly examine cryptocurrencies from a cross-asset portfolio perspective, as is standard practice in stocks and fixed income.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush

İlgili Sorular

QAccording to Wintermute, what major shift in retail investor behavior has occurred since late 2024 regarding stocks and cryptocurrencies?![]()

ASince late 2024, the relationship between retail investment activity in stocks and cryptocurrencies has reversed. Instead of moving in the same direction, they now show an inverse relationship: when retail investors buy stocks, they are inactive in the crypto market, and vice versa.

QWhat is one of the key technical factors accelerating the shift of retail attention from crypto to stocks, as mentioned in the report?![]()

AOne key technical factor is the integration of AI and large language models (LLMs), which have significantly enhanced retail investors' analytical capabilities in the stock market, creating a perceived 'level playing field' and a sense of cognitive edge that is currently missing in the cryptocurrency space.

QHow has the volatility premium of cryptocurrencies, a major attraction for retail investors, changed structurally?![]()

AThe volatility premium of cryptocurrencies relative to stocks is structurally compressing. While crypto's actual volatility is still higher, the ratio (e.g., BTC vs. NDX) has been declining and even compressed to below 2x in early 2025, eroding a core selling point that attracted retail investors in previous cycles.

QWhat does the report suggest about the traditional leading indicators for crypto risk appetite, such as M2 money supply?![]()

AThe report states that traditional leading indicators for crypto risk appetite, like the M2 money supply, are failing. Investors now need to view crypto through a multi-asset portfolio lens, similar to how they approach other mature asset classes, rather than relying on these outdated metrics.

QWhat conclusion does Wintermute draw about the future role of cryptocurrencies in retail investors' portfolios?![]()

AWintermute concludes that while they still have a place, cryptocurrencies are now just one choice among many for retail investors and are no longer the main arena for speculation. Retail risk appetite is increasingly being satisfied elsewhere, particularly in the stock market.