Authored by: Tiger Research

Compiled by: AididiaoJP, Foresight News

A recent in-depth report from Tiger Research points out that the tokenized real-world asset market is growing rapidly, yet many jurisdictions still lack a well-established regulatory framework. Local financial institutions face strategic choices between waiting for domestic legislation, conducting limited experiments using regulatory sandboxes, or proactively entering overseas mature markets.

Before formally entering, institutions must make thorough preparations in six core areas, including jurisdiction selection, license acquisition, asset definition, target investor scope, as well as the design of settlement mechanisms and operational arrangements. The core objective is to accumulate practical operational experience as quickly as possible by choosing the path most suitable for their specific circumstances. There are two main paths: directly entering jurisdictions with mature regulations, or adopting the technology route of natively on-chain platforms.

Wait, Experiment, or Go Global?

As of the first half of 2026, the tokenized real-world asset market has reached approximately 250 to 360 billion US dollars. This market has achieved significant efficiency improvements through tokenization—including automated interest payments and redemptions, shortened settlement cycles, and expanded customer bases—attracting substantial attention from institutional investors.

However, financial institutions still face the practical obstacle of regulatory gaps. While there is no explicit prohibition of tokenization, the legal framework for distributed ledger records to gain legally binding force remains incomplete, and investor rights lack sufficient protection. In this context, financial institutions generally adopt three strategies:

- Waiting for domestic legislation: This approach is favorable for risk management but may lead to missing opportunities to capture early market share.

- Using regulatory sandboxes: Allows for experimentation within a limited scope, but typically only for small-scale scenarios like fractionalized investments, making it difficult to expand to standardized securities issuance.

- Proactively entering overseas markets: Issuing digital bonds in jurisdictions with mature regulations, accumulating performance and track records offshore to build a competitive advantage.

Since real-world asset businesses are inherently global, financial institutions need to build operational capabilities across different regulatory environments. For jurisdictions where regulations are not yet well-developed, institutions have even more reason to accumulate practical experience in overseas markets ahead of time to gain a lead over peers.

Tokenization is Not Magic

International real-world asset operations are not the result of isolated decisions but a series of interlocking choices. Tokenization is not magic; it is the process of migrating existing financial instruments to new infrastructure. This process demands higher precision than traditional issuance, not lower.

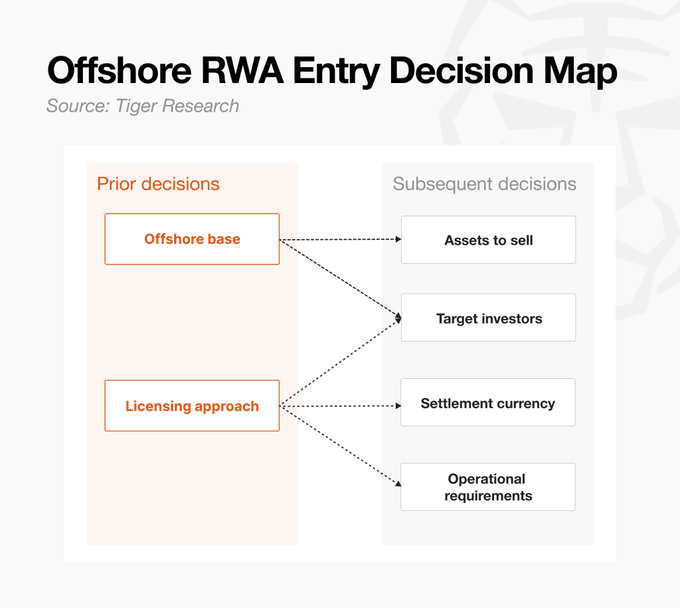

Before deciding to enter, institutions should honestly assess their preparedness in the following six areas:

- Establishing an offshore base: Determine how to leverage key jurisdictions like Hong Kong, Singapore, or the US—whether through existing entities, setting up new ones, or partnering with local companies. A new entity offers stronger control but requires significant resource investment; a partnership allows faster entry but with limited internalization of core capabilities.

- License acquisition: Meet licensing requirements in target sales jurisdictions. Options include direct application (time-consuming and costly) or leveraging existing platform licenses (faster, but requires designing the issuance structure to platform specifications).

- Asset definition: The type of asset chosen for tokenization determines the entry barrier. Standardized securities like bonds have mature structures and are relatively easy to implement; non-standard assets like real estate or trade receivables require more time for legal review and structural design.

- Target investor scope: The common strategy is to target all jurisdictions except the United States. Selling to non-US investors can rely on Regulation S offshore exemption; if including US investors, additional requirements like Regulation D are needed, increasing structural complexity. Furthermore, many Security Token Offerings (STOs) and real-world asset platforms are limited to qualified or institutional investors, so the sales strategy must be determined concurrently with the investor scope.

- Settlement currency and payment process: Decide whether to accept local currency, US dollars, stablecoins, or wholesale central bank digital currencies for settlement. This concerns not just currency choice but also directly impacts investor accessibility, custody structure, and final revenue. For example, accepting stablecoins introduces exchange requirements and potential additional costs.

- Other operational requirements: Depending on the structure, numerous other matters need consideration, such as blockchain choice, custody, on-chain operations, and post-issuance governance. It is particularly important to clarify who controls interest payments and redemptions, registry management, and the ability to forcibly transfer or freeze tokens in case of events—these requirements are similar to those for traditional financial instruments.

Even after structural design is complete, the work is not over—the securities must be successfully sold and investors found.

Choosing the Operational Location

Jurisdiction selection is a strategic decision requiring simultaneous consideration of regulatory fit and operational efficiency.

For institutions with existing offshore presence, the most efficient starting point is to first assess their current jurisdictions. If the primary goal of an offshore tokenization strategy is to accumulate practical experience as early as possible, establishing a completely new jurisdictional base has relatively high time and capital barriers.

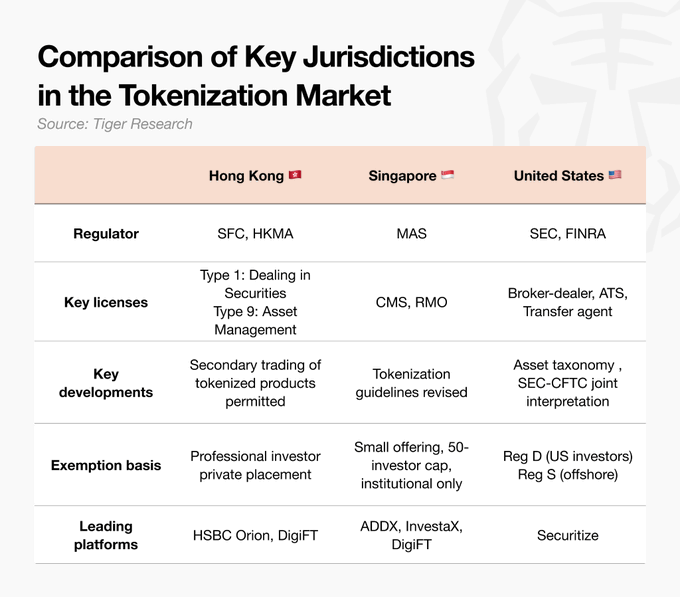

- Hong Kong: Leading in regulatory completeness and enforceability. Security tokens are regulated within the existing Securities and Futures Ordinance framework. The SFC circular in April 2026 allowed secondary trading on licensed virtual asset exchanges, completing the issuance and distribution loop. Infrastructure like HSBC Orion is operational, with strong policy support, including subsidies for issuance costs from the HKMA. Note: If the planned legislation introducing new virtual asset trader and custodian licenses proceeds in 2026, compliance issues regarding transitional provisions deserve attention.

- Singapore: Precise framework, clear regulations. Singapore strictly adheres to the "same activity, same risk, same regulation" principle. The MAS revised its tokenization guidance in December 2025, providing clearer direction. The Variable Capital Company (VCC) structure facilitates asset segregation and is suitable for fund setups. However, even for businesses targeting offshore clients, licensing requirements are relatively strict, creating a higher entry barrier.

- United States: Clear regulations, efficient market access. The joint interpretation by the SEC and CFTC in 2026 clarified the asset classification framework. Directly obtaining a license as an issuer is costly, but operating through vertically integrated platforms like Securitize allows for efficient use of Regulation D (for US accredited investors) and Regulation S (for offshore investors) exemptions. BlackRock's BUIDL fund is a typical example of this path.

Each jurisdiction has mature platforms that can accelerate local market entry. These licensed operators provide regulatory coordination, in-platform fundraising investor networks, and operational infrastructure covering the entire lifecycle from issuance to settlement. When evaluating entry into a specific jurisdiction, meeting with leading local platforms to test commercial feasibility is often more efficient than reading extensive regulatory documents first.

The Natively On-Chain Path to Bypass Jurisdictional Constraints

The previous section discussed the direct approach of establishing a legal and physical presence and obtaining necessary licenses in a specific jurisdiction. This section introduces a fundamentally different method: the natively on-chain path, designed from the outset around the on-chain environment for issuance and distribution.

This approach avoids investing significant time and capital in establishing a physical base. Instead, it leverages or borrows from existing on-chain platform structures with built-in regulatory compliance, lowering market entry barriers. The jurisdictional path asks, "Where will we operate?" The natively on-chain path asks, "How will we structure the transaction?"

Typical examples include:

- Ondo Global: Tokenizes US securities through a bankruptcy-remote Special Purpose Vehicle (SPV) registered in the British Virgin Islands, leveraging the Regulation S offshore exemption to reduce friction with US securities regulations. It also operates its own secondary market, Ondo Global Markets, directly handling trading of its issued tokens.

- Plume Nest: KDAB, Plume's Bermuda subsidiary, holds a Class M DABA license from the Bermuda Monetary Authority, operating a regulated on-chain vault. The Plume Nest platform is accessible only to investors who have passed KYB and KYC screenings. The SEC transfer agent registration of an affiliated company provides a second layer of assurance for ownership registry management and distribution. Due to the platform's decentralized design, tokenization outside the licensed structure is possible, but this path is less suitable for regulated financial institutions.

The natively on-chain strategy is substantively similar to jurisdictional tokenization but differs significantly in execution. Its main advantages are speed of entry and broad reach: institutions can leverage proven infrastructure to enter markets faster without being tied to a specific base. Another advantage is that unlike closed ecosystems of jurisdictional platforms which may limit secondary market liquidity, natively on-chain platforms built around extensibility can naturally connect to DeFi liquidity pools.

However, the complexity of structural design is a trade-off risk. The openness of these platforms allows for a wider range of product types but lacks the existing regulatory guidance found in the direct jurisdictional path for core structural decisions (like issuance design). Since different platforms employ different structures, they may also create operational burdens for traditional financial institutions, warranting assessment of whether the platform has local points of contact in the target region.

Don't Wait for Regulation, the Market Won't Wait

Major US financial institutions are already leading the market, either building proprietary platforms or accumulating direct experience on networks like Canton, Solana, and Ethereum.

For financial institutions in jurisdictions where regulation is not yet well-developed, launching offshore real-world asset businesses requires redesigning the entire local value chain, from establishing a base to distribution. The preparation period typically ranges from six months to over a year. The report uses "Company A," a medium-sized securities firm with an existing Hong Kong entity, as an example to detail the process of tokenizing short-term investment-grade bonds for offshore institutional investors:

- Step 1: Assess existing base and licensing status. Utilize the existing Hong Kong subsidiary to avoid the time and cost of setting up a new entity. Legal counsel reviews current authorized scope, conducting preliminary consultations with regulators (e.g., Hong Kong SFC) if necessary to confirm if changes to license conditions or additional filings are needed.

- Step 2: Select platform and infrastructure. To reduce the time for direct license application, consider operating through a mature platform like DigiFT. Due diligence covers platform license validity, supported asset range, custody partners, and investor restrictions. During the contract stage, legal review is conducted to handle issuance structure design compliant with platform specifications, liability allocation, and governing law.

- Step 3: Regulatory compliance and product design. Finalize the product structure of the bond to be tokenized, including underlying assets, investor rights, and governing law. Standard practice is to target offshore institutional investors outside the US, utilizing the Regulation S exemption. Legal opinions are required on compliance with local securities laws in each target jurisdiction, and the logic for excluding local residents must be validated under securities laws before proceeding to prospectus drafting and approval.

- Step 4: Design custody structure and on-chain operations. Establish a dual custody arrangement: a global custodian bank for the physical asset and specialized infrastructure for on-chain tokens. Obtain legal opinions via external counsel. Simultaneously finalize operational details, including interest payment schedules, settlement currency (USD or stablecoin), and redemption mechanisms.

- Step 5: Issuance, execution, and verification. Execute the actual issuance and sales according to the final structure, and confirm that operational procedures like interest payments and redemptions run as designed. Structural design is just the starting point; the business is only complete after investors are won over and sales are concluded.

This offshore tokenization strategy is not limited to the direct path of establishing a base in a specific jurisdiction. Flexible approaches like the natively on-chain path, which bypass jurisdictional boundaries, mean the choice of viable paths is essentially open.

In any path, legal review is the most time-consuming and expensive threshold. However, waiting for a complete regulatory framework is not the only answer. Quickly planning a viable path and accumulating experience through execution is more important than anything else, because the substance of the tokenization business lies not in technical design, but in completing the full sales process.

No one can predict when regulation will finally be finalized, and the market will not wait. Now is the time to act.