Author: Frank, PANews

Original Title: The More It's Banned, The More It Rises? Unpacking the Black and White Truth Behind XMR's Surge

XMR (Monero), one of the leading players in the privacy sector, hit a new all-time high on January 13, with its price peaking at over $690, reigniting discussions about privacy coins.

From January 2025 to now, over the past year, XMR has surged from around $200, achieving a maximum gain of 262%. Amid widespread weakness in mainstream altcoins, such a rise is exceptionally rare. More intriguingly, this rally occurred against a backdrop of unprecedented global regulatory tightening.

Due to compliance pressures, major centralized exchanges like Binance had already delisted XMR spot trading. Then, on January 12, the Dubai Virtual Assets Regulatory Authority (VARA) officially announced a ban on the trading and custody of privacy tokens throughout Dubai and its free zones. However, far from casting a shadow over XMR, this ban was met with defiance as the coin hit a new high, almost mocking the Dubai government.

So, who is the real driving force behind XMR's rise, caught between dwindling exchange liquidity and regulatory crackdowns? PANews peels back the surface to find the real demand behind this market movement.

Exchanges Are Not the Core Pricing Venue

Despite the hot market, it is not primarily driven by funds within exchanges.

In terms of spot trading, while XMR's recent trading volume has increased with the price rise, it has generally remained in the range of tens of millions to $200 million, without any particularly dramatic spikes. Looking back, the significant peak in spot trading volume was actually on November 10, reaching $410 million. This means that during this recent doubling rally, spot trading (or buying pressure on centralized exchanges) was not the main driver.

The situation is similar for futures. The volume peak also occurred on November 10. Until about a week ago, futures trading volume did not show a significant surge and even showed some signs of decline. Observing the open interest data, the change curve in USD terms almost perfectly overlaps with the price movement. The number of XMR positions in the market did not abnormally spike; the increase in open interest value was solely due to the rising coin price, not a large influx of new capital opening positions.

Clearly, mainstream exchanges are not the core pricing venue for XMR currently.

Undercurrents on the Supply Side: Miner Shake-up and Early Positioning

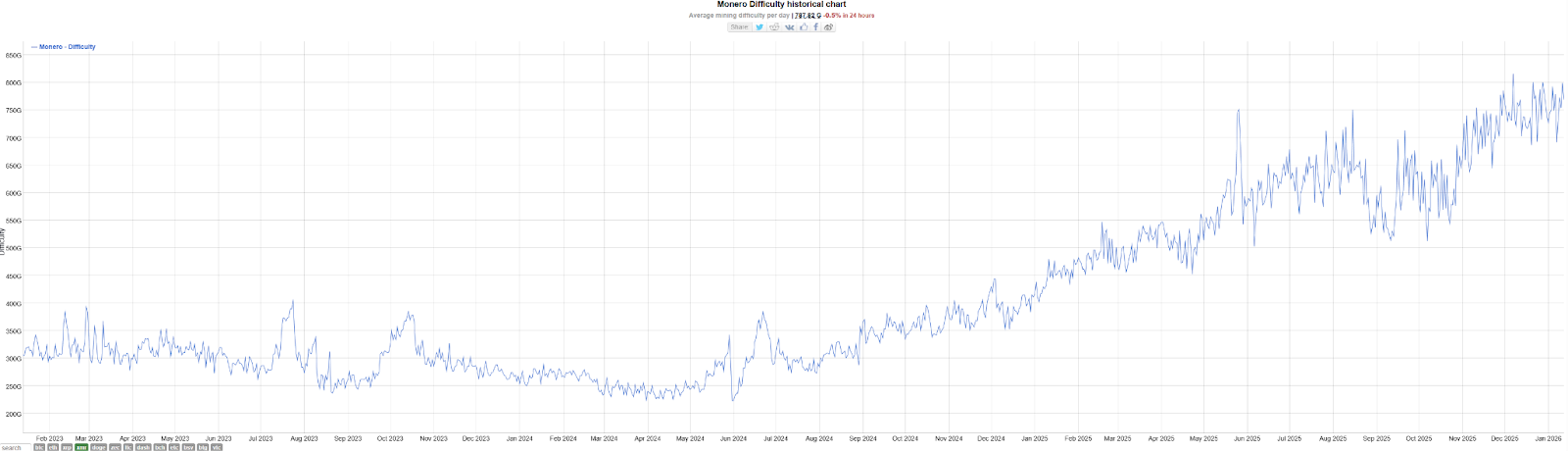

Since the "visible" funds are unremarkable, we need to turn to the "invisible" on-chain world. As the network with the strongest privacy, XMR offers very little information to mine, but changes in mining difficulty and mining rewards allow us to glimpse the capital布局 (layout) on the supply side.

Historical mining difficulty typically represents capital's enthusiasm for participating in the network ecosystem. Data shows that XMR's mining difficulty began to climb rapidly at the end of 2024 and was in a state of rapid growth throughout the first half of 2025. Although it fluctuated between September and November, it recently began a new round of difficulty increase.

An interlude must be mentioned here: In September, the Qubic project claimed it controlled over 51% of XMR's total network hash rate and performed a "demonstration attack," causing a chain reorganization spanning 18 blocks on the XMR network. This event served as a wake-up call for the community, after which a large number of miners migrated their hash rate to the established mining pool SupportXMR. This incident was the main reason for the剧烈波动 (violent fluctuations) in mining difficulty around the end of 2025, but it also侧面印证了 (serves as side evidence of) the activity and resilience of the hash rate market.

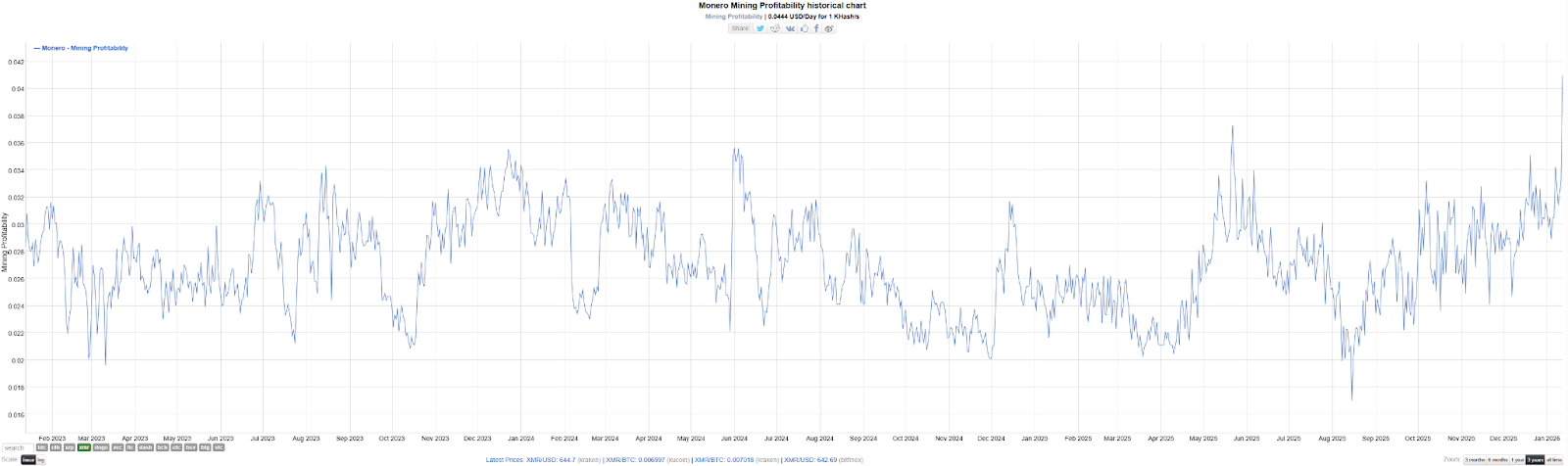

More noteworthy is the联动 (linkage) between the mining reward curve and the difficulty.

Before April 2025, the mining rewards on the Monero network experienced a significant drop. Correlating with the difficulty chart from that time, the hash rate rose sharply while the price remained震荡 (volatile). This divergence led to diluted rewards, likely forcing some smaller miners with higher costs out of the market. Data showing a回调 (pullback) in mining difficulty in April supports this猜想 (conjecture).

This was a classic case of "miner capitulation" and "筹码交换 (chips exchange/churn)." After this, as prices rose significantly, mining rewards and difficulty resumed同步上涨 (synchronous growth). Judging from the data changes in this phase, as early as the beginning of 2025, some large mining enterprises or capital with strong risk resistance might have started positioning early in Monero token mining despite the low rewards.

Demand-Side Verification: Paying a High Premium for Privacy

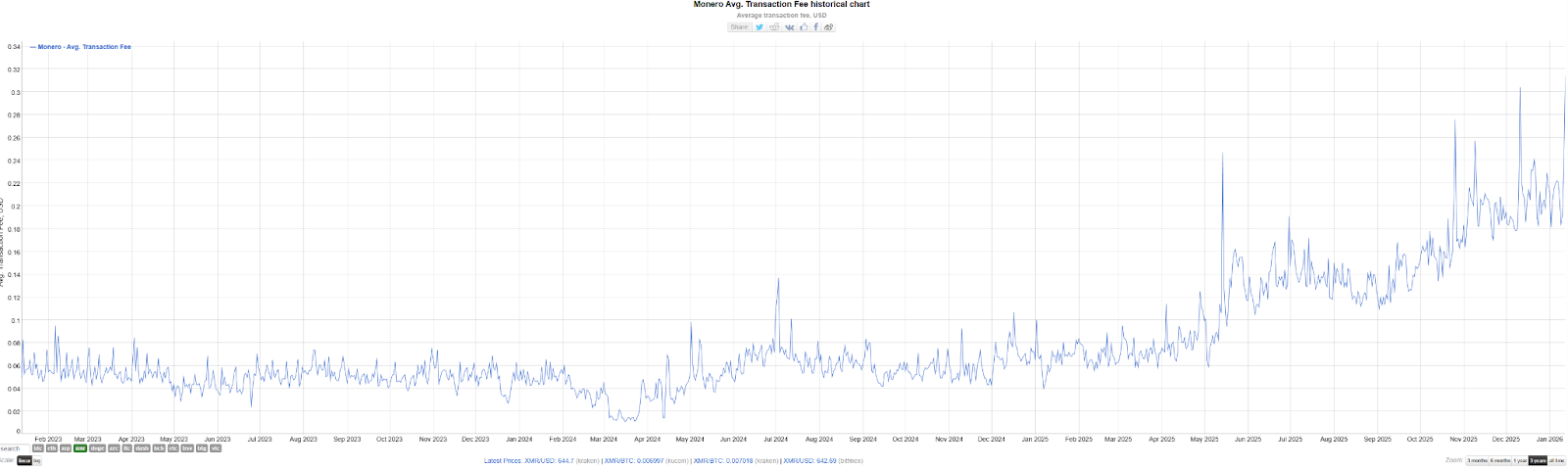

If miners represent confidence on the supply side, then the average transaction fee most accurately reflects demand on the user side.

Looking at the chart, Monero's average transaction fee was relatively stable before the first half of 2025, basically staying below $0.1. But starting in June, a growth trend emerged; by December 11, the highest average fee一度达到 (once reached) over $0.3, more than triple the level from six months prior.

Because Monero has a dynamic block size adjustment mechanism, a surge in fees means a large number of users are trying to send transactions quickly and are willing to pay high fees to compensate miners for the cost of block expansion. This侧面证明 (serves as indirect proof) that starting from the second half of 2025, the real on-chain transaction demand for Monero began to increase significantly.

However, we also discovered an interesting pattern: spikes in on-chain fees often coincide with sharp price increases.

For example, on April 28, XMR suddenly rose 14%, and the average transaction fee that day surged to $0.125; during the subsequent period of slow price爬升 (climb), fees fell back to a trough (lowest at $0.058 on May 4). This indicates that while market volatility can drive on-chain demand in the short term, when the volatility subsides, on-chain demand also returns to calm. Although sometimes they are not synchronized (e.g., fees rose on May 14 but the price didn't move), overall, during these more than six months, price increases briefly drove on-chain demand, and the growth in real on-chain demand in turn triggered market optimism about XMR, with the two互为因果 (being mutually causal).

The Truth in Black and White

Combining the above data, the truth behind XMR's surge likely has "black and white" aspects.

The so-called "white" truth is the "antifragile" rebound of privacy demand under high regulatory pressure.

The反向推动 (reverse driving effect) of regulation is becoming increasingly apparent. The VARA ban not only failed to crush XMR but made market participants realize: regulatory agencies can ban exchanges, but they cannot ban the protocol itself. As major exchanges退出 (exit) the XMR trading环节 (segment), the logic of pricing reliant on market makers and derivative contracts was rewritten. XMR returned to a model controlled by real users or certain heavyweight players. After脱离 (detaching from) the exchange system, privacy coins have developed an independent rhythm completely different from the mainstream market.

The so-called "black" truth is the capital game under information asymmetry.

Behind this opacity, there might be an "iceberg" of whales. The "unimpressive" trading data (even on January 13, when it hit a new high, futures open interest was only $240 million, and liquidation volume was just over $1 million) indicates that mainstream institutions almost failed to predict and participate in this rally in advance, only following along.

This information asymmetry, held by a few, leads to extreme price volatility. Especially when the market starts paying attention to such a rise, it often signals short-term emotional overheating. Referring to the privacy coin ZEC in November, it experienced a retracement of over 50% after its surge. Ultimately, in the privacy coin market, there is a large amount of "information asymmetry," which puts ordinary retail investors at an absolute disadvantage.

Amid the剧烈波动 (violent fluctuations) of privacy coins, on-chain data is perhaps our only reliable guide. But in the depths without transparency, the high premium of freedom always comes with unknown risks.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush