Author: Max.s

For a long time, many natives of the crypto world have been intoxicated by a grand narrative: Web3 will launch a revolution against Web2. By moving Nasdaq stocks onto the blockchain and replacing the NYSE's matching engine with smart contracts, they believe they can ultimately reshape global finance with RWA (Real World Assets).

Watching the constantly flickering K-line charts, we need to remember this date when looking back: November 10, 2023. On this day, due to strong market expectations for the approval of the first spot cryptocurrency ETF, institutional funds massively entered through compliant channels, causing a surge in open interest on CME and surpassing Binance.

CME data that day: Open interest reached approximately 111,100 BTC, with a notional value of about $4.08 billion (accounting for roughly 24.7% of the total network open interest at the time).

Binance data: Open interest was approximately 103,800 BTC, with a notional value of about $3.8 billion.

We must admit a harsh reality: This will be a one-sided devouring!

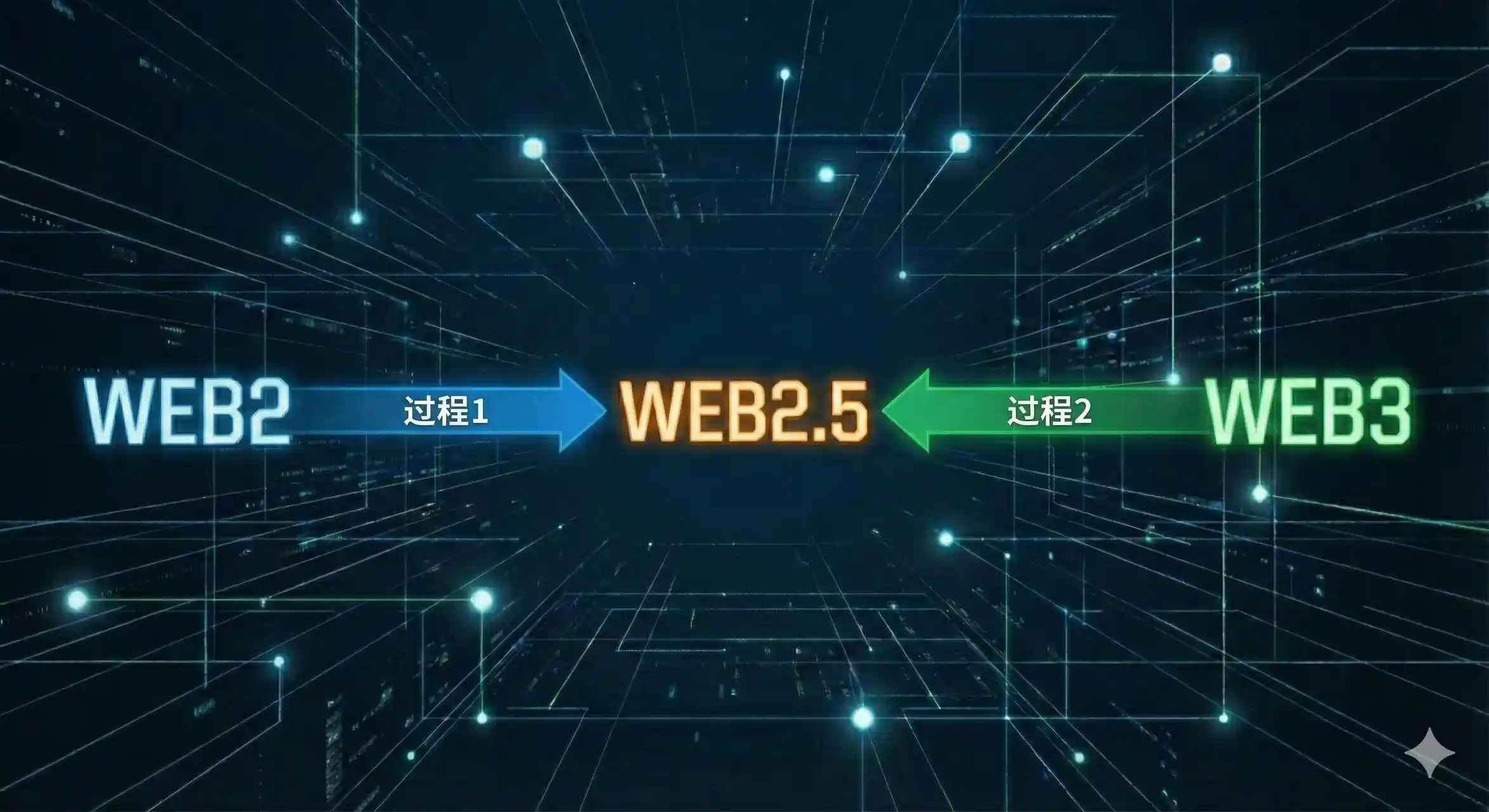

Look at the chart below

Process 1 in the chart represents the expansion of traditional finance (TradFi) into the crypto space, such as CME listing futures and BlackRock launching ETFs. Process 2 represents the penetration of crypto finance into traditional assets, such as tokenized U.S. stocks and RWA.

The current market gives a clear answer: Process 1 is advancing irresistibly, while Process 2 is struggling to make progress. The core of this difference lies not in technology, but in a "compliance cost"-induced dimensional打击 (dimensional strike/attack) on liquidity.

nWhy can Wall Street giants easily cut into the heart of the crypto circle, while we find it difficult to attack their城池 (strongholds/cities)?

Marginal cost in economics can explain everything.

For CME, CBOE (Chicago Board Options Exchange), EUREX (Eurex Exchange), or SGX (Singapore Exchange), the marginal cost of listing Bitcoin derivatives is almost zero.

These financial behemoths possess clearing licenses that have been operational for decades, extremely mature risk control models, and dedicated network lines connecting to the world's top hedge funds. For them, Bitcoin is just another ticker code after gold, crude oil, and soybeans. They don't need to rewrite underlying code, rehire compliance teams, or even re-educate clients. They just need to file a document with the CFTC (Commodity Futures Trading Commission), adjust some parameters, and a new, compliant market capable of carrying trillions in liquidity is born.

In contrast, look at Process 2. When crypto exchanges attempt to "tokenize U.S. stocks," they face an insurmountable chasm.

Remember FTX's once-proud equity tokens? That was not only one of the triggers for its downfall but also an original sin in the eyes of regulators. For a crypto-native platform to compliantly allow users to buy Tesla stock with USDT, it needs to obtain securities broker licenses, clearing licenses, resolve cross-jurisdictional securities law conflicts, and implement extremely complex KYC/AML processes. The compliance cost here is not linear; it's exponential.

For crypto-native enterprises, this is a war that was over before it even began. Traditional finance is not only inherently compliant; they are the rule-makers themselves.

Why is compliance cost so important? Because compliance directly determines safety, and safety determines the entry threshold for capital.

Retail investors in the crypto market often misunderstand the source of "liquidity." True liquidity doesn't come from the few thousand U in散户 (retail investors') hands; it comes from pension funds, endowment funds, sovereign wealth funds, and large market makers.

These behemoths face extremely strict Fiduciary Duty. This explains why the approval of the Bitcoin spot ETF in 2024 became a historic turning point.

Before the ETF, a traditional family office wanting to allocate Bitcoin had to go through extremely complex approvals: Who manages the private keys? What if the exchange explodes? How is auditing done? ETFs and CME futures perfectly solve this problem: no need to manage private keys, no need to trust offshore exchanges, everything is done within a U.S. stock account.

The record-high open interest in CME's Bitcoin futures is not driven by retail speculation, but by Wall Street institutions engaging in basis trading and risk hedging. Top high-frequency trading firms like Jump Trading and Jane Street have lower latency in CME's server rooms than on AWS.

As CBOE plans to re-enter the crypto derivatives market, and as SGX and EUREX begin laying out compliant derivatives channels in Asia and Europe, we see a clear trend: The pricing power of crypto assets is shifting from offshore, unregulated exchanges (like the early BitMEX, or some current offshore CEXs) to regulated traditional financial exchanges.

Just as crude oil futures don't require the owner to actually transport crude oil, future crypto finance won't require investors to actually use decentralized wallets.

In this process, cryptocurrency itself is stripped of its "currency" payment attributes, stripped of its "censorship-resistant" ideology, and refined into a pure, highly volatile financial instrument. It is packed into ETF capsules, bundled into futures contracts, and stuffed into traditional 60/40 asset allocation portfolios.

The conclusion seems inevitable: Web3 finance (especially the secondary market part) will most likely be integrated into Web2 finance, becoming a trading category within traditional finance.

This might sound unpleasant to crypto purists, but it is precisely a sign of the asset's maturity.

The future landscape might look like this: The underlying blockchain technology (Web3) will still be responsible for asset generation and title verification, like BTC mining. But in the vast financial superstructure of trading, clearing, and derivatives, the Web2 giants, with their low-cost compliance advantages, will still occupy the main seats at the table.

For investors, seeing this clearly is crucial. Where the liquidity is, the Alpha is. And right now, liquidity is irreversibly flowing back to those in suits.