Written by: Anna Irrera, Bloomberg

Compiled by: Chopper, Foresight News

JPMorgan Chase invested hundreds of millions of dollars over more than a decade to develop blockchain systems, an innovative technology once touted as poised to revolutionize financial markets, yet it struggled to trigger industry-wide transformation. Today, however, banks and blockchain technology are finally achieving a substantial breakthrough in a key area: the repo market.

The nearly $13 trillion repo market is not the flashiest track on Wall Street, yet it serves as the financial lifeline that maintains the flow of global capital. In simple terms, a repurchase agreement (repo) is a transaction where an institution borrows cash, usually overnight, using government bonds as collateral. It provides the short-term funding foundation for trading, settlement, and market-making activities across the entire financial system.

Currently, JPMorgan and its Wall Street peers have found that the blockchain technology underlying cryptocurrencies is highly compatible with repo operations. It enables precise, customizable transactions, allowing funds and collateral to move faster and be deployed more flexibly, helping traders unlock idle capital, improve funding efficiency, and simultaneously hedge market risks.

Eddie Wen, JPMorgan's Global Head of Digital Markets, stated, "The logic for applying blockchain solutions to repo business is completely sound." JPMorgan is one of the largest banks in the repo trading space, and Eddie added that clients use this product daily.

Six years ago, JPMorgan officially launched its blockchain-based funding product. To date, the platform has cumulatively processed approximately $3 trillion in repo transactions. Currently, the platform handles billions of dollars in daily client repo financing volume, with cross-departmental daily transaction volume within JPMorgan reaching around $5 billion.

For this giant, whose traditional repo market daily trading volume reaches hundreds of billions of dollars, this volume, while still a small percentage, marks a crucial step in the industry leader's formal embrace of blockchain technology.

Industry-wide Rush into Tokenized Repo

Beyond JPMorgan, institutions including HSBC, market makers DRW Holdings and Virtu Financial, as well as financial infrastructure service providers like Broadridge and trading platform Tradeweb, are collectively intensifying their focus on the tokenized repo sector. Daily tokenized repo trading volumes across various blockchain platforms have now reached tens of billions of dollars. Although the depth of participation and transaction frequency vary among institutions, joining the fray has become an industry consensus.

Objectively, the market will not transform overnight, and the scale of blockchain repo trading still lags significantly behind the traditional market. To achieve widespread adoption, more banks, dealers, and financial infrastructure providers need to adopt compatible systems. Simultaneously, the industry faces new regulatory requirements like mandatory central clearing for repos, forcing most institutions to prioritize adapting to existing workflows in the short term.

But even in its early stages, the growth momentum is already established. While most other blockchain applications in capital markets remain in pilot or proof-of-concept stages, the scale of blockchain implementation in the repo market by institutions far surpasses most mainstream financial scenarios. Tokenized repo has thus become one of blockchain's most solidly implemented and potentially impactful applications within traditional finance.

Elisabeth Kirby, Head of Market Structure at Tradeweb, which launched its blockchain repo platform late last year, stated bluntly, "This is not a proof-of-concept, nor is it a pilot project to be shelved and observed. It is a genuine growth sector."

Why Is It Booming Now?

Over the past year, tokenized repo trading has noticeably accelerated, driven by multiple converging factors. Blockchain networks have moved from testing to real business implementation; regulatory acceptance for migrating repo activities onto blockchains has significantly increased. Given the crucial role of institutions like the Federal Reserve during market turmoil, the shift in regulatory attitude is vital. A more favorable digital asset policy environment under the Trump administration has also encouraged Wall Street institutions to increase their deployments.

Meanwhile, a growing number of clients are experiencing the tangible advantages of blockchain, leading to a complete shift in industry perception: blockchain is no longer just a niche tool for the crypto world, but a universal financial infrastructure capable of optimizing transaction processes and reducing operational costs.

Yuval Rooz, CEO of digital asset firm Digital Asset Holdings, said, "The biggest change is that the industry is no longer debating whether the technology works, but focusing on how fast we can scale implementation." The company, backed by giants like JPMorgan, Goldman Sachs, DRW, Citadel Securities, and Virtu, has built the Canton Network, now one of the most mainstream blockchain foundations in traditional finance.

In February this year, the Canton Network completed several cross-border repo transactions using tokenized UK government bonds as collateral; its technology also underpins Broadridge's distributed ledger repo platform, serving institutions like UBS, HSBC, and Societe Generale.

Bloomberg L.P., the parent company of Bloomberg News, recently partnered with data service provider Kaiko to integrate Bloomberg data into the Canton Network, serving tokenized US Treasuries and on-chain repo transactions.

Operating Logic: Traditional Repo vs. Tokenized Repo

Models differ slightly across platforms, but the core distinction lies in how funds and securities flow.

The traditional repo market has fixed opening, order placement, and closing times, halting overnight and on weekends; operations heavily rely on intermediaries to handle collateral and settlement processes, involving numerous middlemen and high fees; ad-hoc changes often require phone coordination. Cross-border transactions are particularly cumbersome due to time zone and holiday mismatches, leaving idle funds tied up for hours; they are also frequently interrupted or canceled due to missed deadlines, insufficient collateral, or system failures.

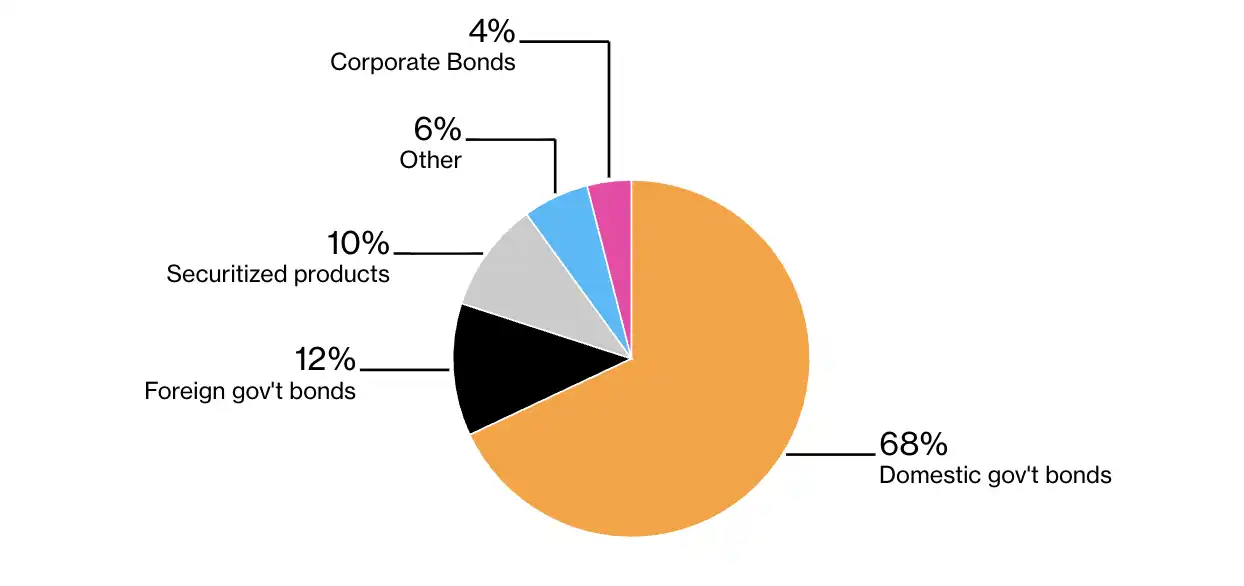

Composition of collateral types in global repo transactions

Tokenized repo perfectly addresses these pain points. A borrower initiates a funding request via a digital interface, and after confirmation by the lender, both cash and securities collateral are mapped as on-chain tokens; both parties confirm and the transaction is recorded on the chain, with terms automatically executed as agreed, and the entire process is auditable and traceable. The most significant advantage is 7x24 continuous tradability, unrestricted by traditional business hours.

Sonali Das Theisen, Head of Fixed Income, Currency, and Commodities (FICC) Electronic Trading and Market Strategy at Bank of America, commented, "Blockchain can effectively reduce friction in capital flows. The industry's movement in this direction is an inevitable trend."

Tangible Financial Benefits

For repo market giants, blockchain implementation delivers real financial gains. Banks like JPMorgan not only save on fees and transaction time but can also reduce the regulatory capital requirements for their trades.

A recent Broadridge analysis shows that if a large bank migrates 15% of its repo business onto blockchain, its daily liquidity buffer funds could decrease by 8%–17%. Specific savings depend on the institution's size, business region, asset structure, and risk appetite, but overall it can significantly unlock idle capital.

The Broadridge research report cites data from an unnamed major European bank, which needs to reserve approximately €1.1 billion (equivalent to $1.3 billion) daily to meet intraday liquidity needs. If the buffer funds were reduced by 15%, about €175 million could be freed up for other business uses or to reduce reliance on external financing.

Horacio Barakat, Global Head of Digital Innovation at Broadridge, stated, "The scale of capital savings is considerable. Even a modest optimization can save tens of millions of dollars annually in costs." The company's platform reported a daily average repo trading volume of $368 billion in April, with monthly volume nearing $8 trillion, and a 268% year-over-year increase in daily trading volume.

The industry ecosystem is also moving towards unification. DTCC, Wall Street's core clearinghouse, recently announced it will tokenize highly liquid assets held in its custody, covering US Treasuries, Russell 1000 constituent stocks, and ETFs. This move will significantly expand the pool of eligible collateral for tokenized repos, allowing institutions to directly reuse their existing custodied assets on blockchain ledgers, greatly lowering the barrier to entry.

Enabling 24/7 Trading for Traditional Assets

Industry insiders say that new financing models like tokenized repo are crucial infrastructure supporting the move toward 24/7 continuous trading for traditional assets. Nasdaq has announced plans for 24/7 trading, and the New York Stock Exchange is also developing a tokenized continuous trading platform.

DRW founder Don Wilson pointed out, "For markets to move towards 24/7 trading in the future, the ability to borrow cash at any time is essential. On-chain repos are precisely the core infrastructure supporting this transformation." As an early investor in Digital Asset, DRW has completed several tokenized transactions on the Canton Network over the past year.

DRW Founder Don Wilson

Any new technology faces similar challenges, and the large-scale application of blockchain in repo trading is no exception. While Canton has become mainstream, the industry still consists of multiple independent on-chain systems that are not interconnected. Institutions must adapt to multiple platforms and invest significant manpower in maintenance, with trading volume fragmented across them. Secondly, blockchain systems have not yet endured a full market cycle and extreme stress tests. The traditional repo market has weathered multiple risk shocks since 2008, while on-chain systems have not been tested in real-world scenarios like late-night failures or extreme market volatility.

Furthermore, traditional traders are long accustomed to existing inefficient yet established processes, with rules, error tolerance mechanisms, and post-event contingency plans becoming routine. On-chain transactions follow the principle of "code is law," leaving no room for flexibility.

Sandy Kaul, Head of Innovation at asset management giant Franklin Templeton, admitted, "Traditional business leaves a lot of room for flexible buffers. On-chain, there's zero tolerance for error. Everything is hard-coded; you can't negotiate for a few extra minutes."

Nonetheless, the prevailing industry view is that these are implementation issues to be solved, not reasons to turn back. "We are at a critical inflection point. Blockchain's entry into the traditional financial repo market has officially begun."