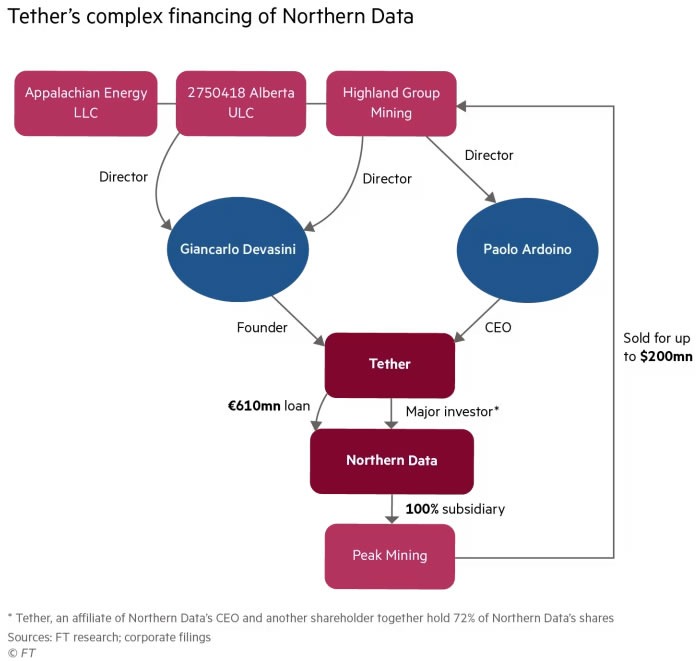

The Tether-backed data centre operator Northern Data reportedly sold its Bitcoin mining business, Peak Mining, to three companies run by Tether executives.

Northern Data was sold for up to $200 million to Highland Group Mining, Appalachian Energy, and an Alberta-based company, run by Giancarlo Devasini, Tether co-founder and chair, and its CEO, Paolo Ardoino, the Financial Times reported on Friday.

Filings reportedly show that Highland Group’s directors are Devasini and Ardoino, and the sole director of the Alberta company is Devasini, while it remains unclear who runs Delaware-based Appalachian Energy.

Northern Data initially announced the Peak Mining divestment in November, but did not identify the buyers, as it was not required by German regulators.

The deal also happened just before video-sharing platform Rumble, in which Tether holds nearly a 50% stake, agreed to acquire Northern Data.

Web of complex financial ties

It is also the second attempt to sell Peak Mining to a Devasini-controlled company. The first deal announced in August was with Elektron Energy for $235 million, but it fell through amid whistleblower allegations.

Northern Data faces investigation by European prosecutors for suspected tax fraud, and its offices were raided in September.

Related: Tether deepens AI bet, backs Italian firm’s humanoid robots

Tether has also agreed on a $100 million advertising deal with Rumble and plans to buy $150 million worth of GPU services from it as it delves deeper into Bitcoin mining.

Northern Data also currently has a 610 million euro ($715 million) loan from Tether.

The stablecoin issuer will receive half of the loan balance in Rumble stock as part of the acquisition, with the rest paid in the form of a new loan from Tether to Rumble, secured against Northern Data assets, the FT reported.

Tether branching out from stablecoins

Tether remains the world’s dominant player in the stablecoin sector with a 60% market share and $187 billion in circulating supply of USDT.

In addition to Bitcoin mining, AI, and video-sharing platforms, it is also eyeing sports teams.

On December 12, Tether launched a $1.1 billion bid to acquire the Italian professional soccer club, Juventus Football Club, but it was rejected by the club’s owners.

Magazine: Big questions: Would Bitcoin survive a 10-year power outage?