Written by: Liam 'Akiba' Wright

Compiled by: Saoirse, Foresight News

Key Takeaways

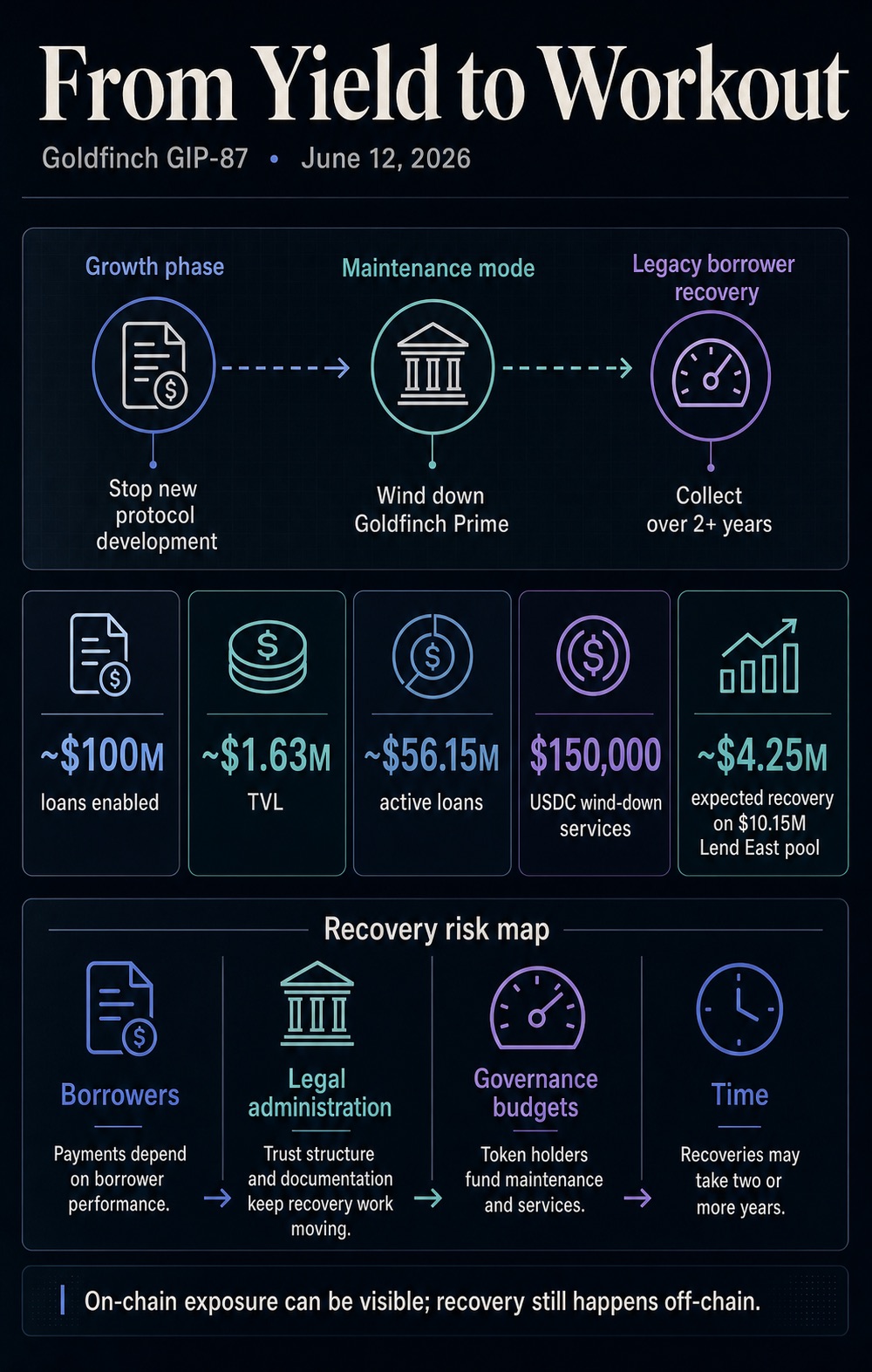

- Governance proposal GIP-87 plans to halt all new feature development, shut down the core product Goldfinch Prime, and allocate 150,000 USDC for subsequent asset recovery and disposition work.

- This proposal is of great significance: the protocol still has a large amount of outstanding loans, and the platform's existing value depends entirely on the execution of subsequent recoveries, post-lending services, and the actual repayment situation of borrowers.

- The community governance has not yet voted on the liquidation plan, and key matters such as the trust structure, user backend access permissions, and details for non-performing asset disposal remain undecided.

Goldfinch is a crypto lending platform with a business model connecting crypto investor funds with offline real-world borrowers. As the lending expansion boom fades, the platform truly reveals a major hidden risk in the industry: when business growth stagnates, the most difficult problem to solve is collecting debts from offline borrowers.

The GIP-87 proposal released on June 12th outlines the following: terminate all new feature development for the protocol, shut down the flagship product Goldfinch Prime, retain backend login access for existing users, establish a US-based trust legal framework, and pay the development partner Warbler Labs 150,000 USDC as compensation for the full suite of liquidation services.

At the time of writing, this proposal is still in the community governance review stage, with public discussion continuing until June 20th. Official results of the vote's approval or rejection have not been announced. However, this sends a unified signal to the entire industry: tokenized private credit businesses will transition from a growth phase of earning stable returns to a disposition phase involving debt restructuring and bad debt collection, with the underlying stock of loans persisting.

For Goldfinch itself, all work in the next stage will revolve around four major challenges: recovering debts from existing borrowers, deteriorating asset quality in multiple borrower pools, ongoing post-lending operational and maintenance costs, and a lengthy debt realization cycle.

This complete shift in business focus transforms decentralized private credit from an investment category promoting low barriers and high returns into a stress test for bad debt disposal. For ordinary investors, various lending protocols, and all RWA lending platforms, a core question arises: once lending scale stops growing, can the platform's entire system of pre-lending risk control, default handling, and debt collection operate normally?

From Scale Expansion to Bad Debt Disposal

The proposal document shows that the Goldfinch protocol has historically facilitated approximately $100 million in real-world loans, but several borrower pools have experienced severe asset quality issues. According to the plan, the protocol will enter a maintenance state, ceasing investment in new feature development and concentrating all operational resources on collecting debts from historical borrowers.

The operational logic of collection business is completely different from that of front-end lending business: new lending pursues approval speed, channel coverage, and fundraising efficiency; debt recovery relies heavily on complete written documentation, sufficient time, legal recourse methods, continuous follow-up with borrowers, and clarity on who bears the collection costs. Goldfinch is now essentially building a publicly accessible bad debt disposal channel for a bundle of private credit stock assets, visible to all token holders.

Recent public data shows that as of June 23rd, the total value locked (TVL) on Goldfinch's blockchain was only $1.63 million, but the scale of outstanding active loans on the platform far exceeds that figure. Specific data fluctuates in real-time, but the core contradiction is clear: the actual credit risk exposure borne by the protocol is much greater than the current liquidity funds remaining on-chain.

Industry statistical rules typically do not include outstanding loans in the TVL calculation, so the two sets of data reflect two different dimensions of the same risk: TVL only reflects the current weak capital size of the DeFi protocol, while active loans represent a large amount of credit that still requires continuous monitoring, maintenance, or collection.

This chart interprets Goldfinch's GIP-87 proposal: the project will stop new feature development, shut down Goldfinch Prime, and enter a maintenance phase, spending over two years collecting $56.15 million in outstanding loans. It reveals that RWA credit only offers transparency for on-chain claims, but repayments rely entirely on offline borrowers, law, governance funds, and lengthy cycles.

The lending platform's dashboard will continue to show the huge gap between TVL and outstanding loans, with the two indicators corresponding to different parts of the system. TVL represents idle funds currently held within the protocol; active loans are credit exposures requiring continuous operation, restructuring, or collection. The long-term significant gap between the two fully illustrates that the responsibilities and costs associated with loan collection will persist long after the platform's growth phase ends.

It is precisely this gap that strips tokenized private credit of its DeFi high-liquidity product facade, reducing its essence to a publicly accessible carrier for private credit collection services.

Past risk disclosure documents from the platform had already foreshadowed such risks: documentation related to senior pools explicitly warned that if borrowers default, participants would incur principal losses; if the USDC reserves in a pool were insufficient, investors would also face liquidity restrictions preventing timely redemptions.

This liquidation plan transforms the generic product risks on paper into practical operational issues for community governance to implement: how much operational funding to allocate, who is responsible for collection work, how existing users retain system login access, and what legal structure to use for handling overdue borrower claims.

The past case of the Lend East borrower pool makes these risks concrete. A community forum announcement in April 2024 showed that this pool, totaling $10.15 million, was estimated to recover only $4.25 million at that time, meaning investors would face a significant principal shortfall.

This data was only an estimated recovery amount at the time of the announcement, not the final actual disposal result, but it is sufficient to show that private credit bad debt recovery is a prolonged game filled with principal losses, multiple rounds of negotiation, and legal litigation, not a simple number balance on a data dashboard.

This is also the core point of conflict between decentralized private credit and traditional private credit: blockchain can make claim positions, token circulation, and protocol activity clearly traceable, but whether loans are ultimately repaid still depends on offline borrower compliance willingness, professional post-lending management, complete compliance documentation, and channels for legal recourse in case of default.

Governance Mechanism Becomes Part of the Credit Risk Control Process

Compared to Goldfinch's hundreds of millions in lending scale, the 150,000 USDC liquidation fee allocated to Warbler Labs is not high, but it brings the hidden cost of bad debt collection into the open. During the business expansion phase, community governance budgets are typically used for product development, user incentives, cross-chain integration, and market expansion.

Entering the liquidation phase, governance funds must be used to maintain system operations, ensure normal user backend access, handle legal and administrative work, and cover the human resource costs generated by dedicated follow-up on outstanding debts.

This directly changes the core content of token holders' voting decisions: they no longer vote on ecosystem expansion plans, but rather judge how the platform's stock of credit assets should be continuously operated after all growth funds have withdrawn.

The plan to establish a US trust structure and retain existing user login access in the proposal both point to the same operational phase: the platform must retain basic operational capabilities to support repayment and collection business, while cutting all new business unrelated to the existing loan stock.

For all RWA lending platforms, this incident brings an unavoidable lesson: tokenized private credit platforms cannot just prove they have the ability to lend and acquire customers; they must also establish a sound borrower screening mechanism, standardized information disclosure rules, mature bad debt disposal processes, sustainable collection incentives, and a supporting governance control system.

If there are shortcomings in any of these areas, blockchain will only publicly and transparently display asset losses without simplifying the debt recovery process.

Previous reports from CryptoSlate have covered growth-related information in this sector: some private credit institutions use AI to compress months-long paper-based approvals into one-day on-chain loans; the industry commonly discusses how tokenized assets can adapt to DeFi's composability constraints.

Goldfinch's proposal fills in the latter half that all expansion narratives deliberately avoid: a rapid lending business model must be paired with a reliable mechanism to handle various issues such as delayed repayments, overdue defaults, and debt disputes.

This stark contrast also highlights the research value of the Goldfinch case. This governance proposal fully demonstrates the transformation of the entire operational logic of the credit business after the lending boom subsides; of course, looking at the entire sector, the overall market demand for RWA lending is far beyond this single Goldfinch project.

Although claims are registered on-chain, the debt recovery process still relies on offline borrower compliance, legal procedures, written documentation, and governance budgets continuously supporting manual disposal work.

Core Capabilities RWA Lending Platforms Must Next Prove

Goldfinch is just a single case in the tokenized private credit sector. Data from DeFi data platform DefiLlama shows that the entire RWA lending sector's total value locked (TVL) and on-chain active loan scale are far larger than Goldfinch's current size. The overall demand of the sector cannot be defined by a single protocol entering a maintenance phase.

But this incident provides a highly valuable industry conclusion: the tokenized private credit sector simultaneously experiences two completely disconnected market cycles. The first cycle is the capital deployment phase: continuous capital inflow, market buzz about annualized returns, corresponding to tokens freely trading on secondary markets. The second cycle arrives years later: borrowers fail to perform on schedule, debt recovery cycles lengthen, community governance needs continuous funding allocation to maintain the entire collection system's operation.

This also makes Goldfinch not just a DeFi protocol, but more like a bad debt disposal investment vehicle. Its future value no longer depends on new feature iterations, but on the actual repayment amounts from borrowers, standardized collection operations, and whether the newly established trust structure can retain sufficient operational capacity to recover all remaining claims.

Going forward, the market will focus on tracking several key signals:

- Whether community governance formally passes the GIP-87 liquidation proposal, determining the subsequent operational roadmap;

- Announcements from the newly established trust institution and asset disposal manager to assess whether collection work has formed a stable process;

- Disclosure of borrower repayment progress to confirm whether outstanding claims can be converted into actual cash recoveries or remain stuck in prolonged negotiation deadlock;

- How all other RWA lending platforms improve rules for disclosing overdue assets, reserve funds for collection operations, and protect investor rights after the yield attributes of credit products disappear.

The Goldfinch case bluntly points out the core dilemma of bad debt disposal: on-chain private credit can only simplify the tracking and statistics of risk exposure, but debt recovery is always constrained by offline borrowers, legal processes, governance budgets, and long time cycles.

High-yield promotion can attract massive capital inflow, but it is the bad debt disposal phase that truly tests whether the quality of the underlying credit assets is reliable.