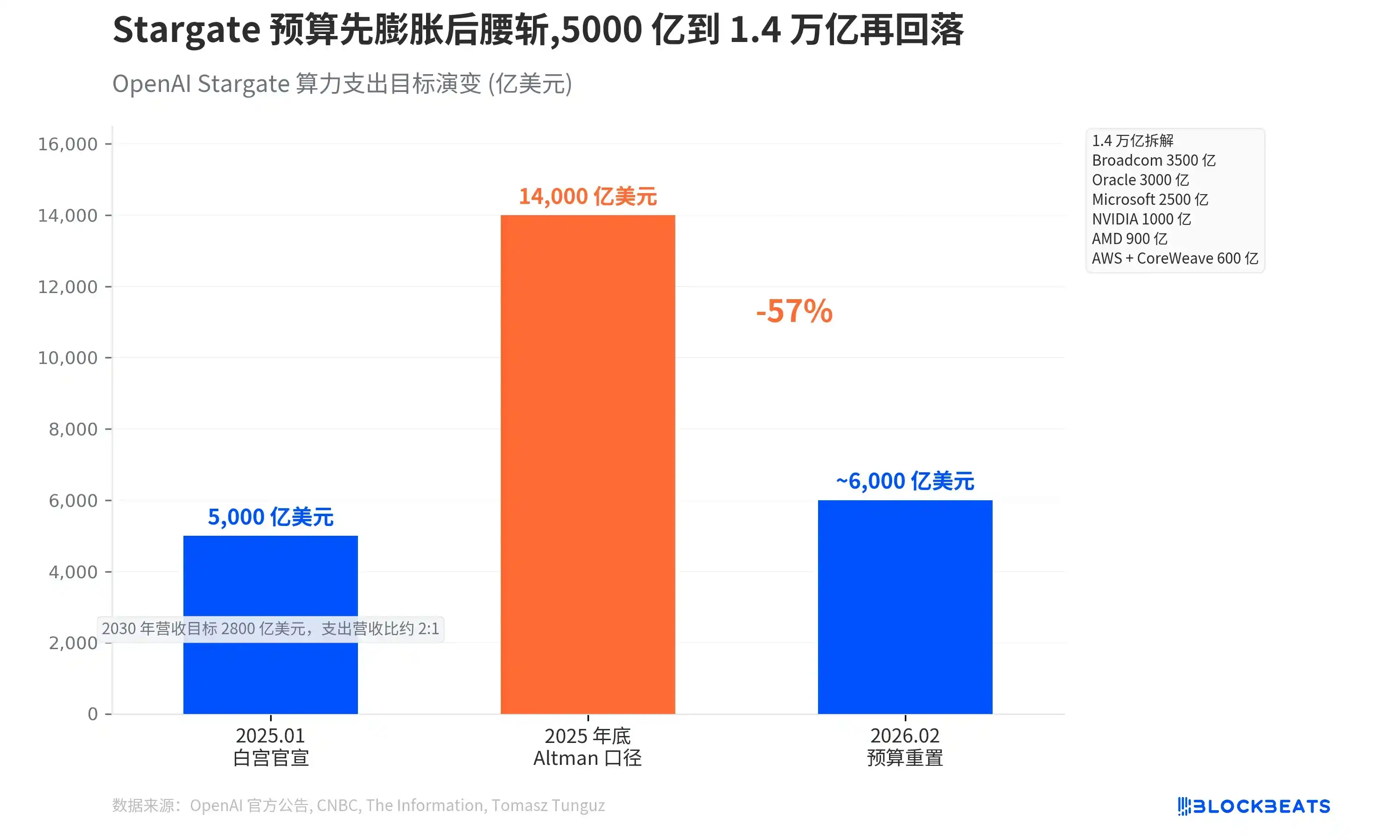

1.4 trillion dollars. This was the total value of the Stargate computing blueprint presented by OpenAI CEO Sam Altman to investors at the end of 2025. Fourteen months later, that number has been slashed to 600 billion.

According to a March 16th report by The Information, OpenAI has significantly restructured the Stargate computing infrastructure project, abandoning plans to build its own data centers and fully shifting to leasing computing power from cloud service providers like Microsoft Azure, Oracle, and Amazon AWS. Stargate has been split into three functional teams, all managed by former Intel Chief Technology and AI Officer Sachin Katti.

The reason for the pivot is straightforward. Stargate was announced with great fanfare at the White House in January 2025, revealing a joint venture with SoftBank and Oracle to build large data centers, with an initial investment of $100 billion and a total investment of $500 billion over four years. However, more than a year after the project's launch, not a single employee had been hired, and no substantive development of a data center had begun. According to CNBC, lenders were unwilling to provide billions in construction financing to a company still reporting massive operating losses. OpenAI also recently withdrew from negotiations to expand the Oracle Stargate facility in Abilene, Texas.

Over a year, zero employees, zero construction started. The "build-it-ourselves" path for Stargate never truly began.

According to disassembled data from investor materials, the $1.4 trillion total commitment cited by Altman was distributed among seven suppliers. According to venture analyst Tomasz Tunguz's analysis of the investor materials, Broadcom accounted for $350 billion, Oracle $300 billion, Microsoft $250 billion, NVIDIA $100 billion, AMD $90 billion, with AWS and CoreWeave combining for $60 billion.

In February 2026, CNBC reported that this figure was reset to approximately $600 billion (by 2030), a 57% cut. The same report gave a slightly different but directionally consistent figure, with OpenAI expecting to spend $665 billion on cloud servers by 2030.

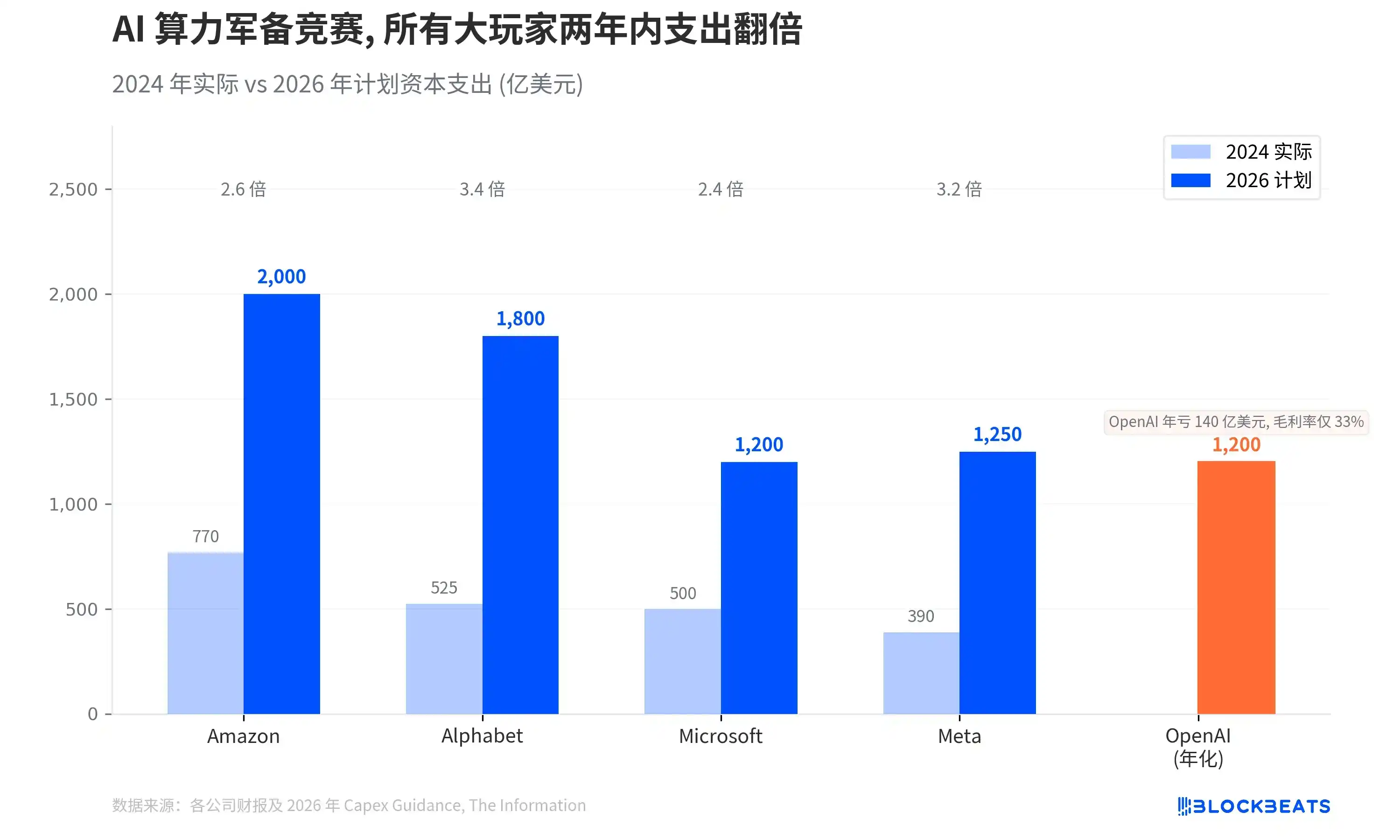

$600 billion is still a number that needs context. According to internal OpenAI forecasts, the company's revenue target for 2030 is $280 billion, meaning the cumulative spending-to-revenue ratio over five years is about 2:1. And according to internal financial data cited by ainvest, the company's projected loss for 2026 is $14 billion, with a gross margin of only 33% as reported by multiple media outlets (Note: Gross margin reflects the profitability of the product itself, while net loss is the final result after deducting all costs like R&D and management; the two can coexist).

Placing OpenAI's spending target within the panorama of the Big Tech computing arms race makes the proportions clearer.

According to company financial reports and public Guidance, Amazon's planned capital expenditure for 2026 is $200 billion, Alphabet's is $180 billion, Meta's is $125 billion, and Microsoft's is approximately $120 billion. These four companies have seen their expenditures roughly double or triple within two years, totaling over $650 billion, with about three-quarters flowing into AI infrastructure.

OpenAI's $600 billion is a five-year cumulative target, annualized to about $120 billion, which is comparable to Microsoft's single-year capital expenditure. The difference is that Microsoft's annual revenue exceeds $240 billion, while OpenAI's annualized revenue has just reached $25 billion and is not expected to achieve positive cash flow before 2030.

The Stargate restructuring is more than just a change in budget numbers; the organizational adjustments reveal a deeper shift in direction.

The restructured Stargate is divided into three lines. The Epic business partnership group is led by longtime OpenAI employee and former Deloitte manager Peter Hoeschele, managing cloud contracts with Microsoft, Oracle, Amazon, and transactions with chip manufacturers. These deals include a multi-year contract with AMD (using up to 6 gigawatts of chips, costing up to 10% of AMD common stock) and an agreement with chip startup Cerebras Systems.

The technical engineering and design group is co-led by former Meta and Google engineer Chris Malone and former Microsoft engineering lead Adrian Caulfield, responsible for redesigning the AI server clusters used by OpenAI. The physical facilities operations group is led by former Google data center director Nick Saddock, replacing Keith Heyde who left weeks ago.

The semiconductor team led by former Google chip executive Richard Ho falls outside Katti's jurisdiction and reports directly to OpenAI President Greg Brockman. This team is collaborating with Broadcom to develop in-house chips, which OpenAI hopes will eventually reduce the inference costs of running products like ChatGPT.

The name "Stargate" remains, but what it refers to has completely changed. In January 2025, it was a joint venture with SoftBank and Oracle to build data centers. In March 2026, it is OpenAI's broad strategy for bringing gigawatt-scale server capacity online. It has gone from "I want to build my own power plant" to "I want to sign the best leases." The total planned capacity for all sites remains nearly 7 gigawatts, with a three-year investment total still exceeding $400 billion. OpenAI is shifting its computing direction towards NVIDIA's Vera Rubin platform, aiming to achieve the first gigawatt-scale capacity online in the second half of 2026.