Original Author: Kaori

On February 8, 1971, the Nasdaq system went live.

There was no trading floor, no bell-ringing ceremony; it was merely an electronic quotation terminal that connected over-the-counter dealers scattered across the United States into a network. The brokers at the New York Stock Exchange (NYSE) took a glance and didn't think much of it. For two hundred years, the rule of stock trading was that you walked into that building, stood on that floor, and shouted bids face-to-face. What could a screen possibly change?

Twenty years later, Intel, Microsoft, and Apple listed on Nasdaq one after another, and the era of tech stocks redrew the map of Wall Street. The NYSE began to catch up, acquiring the electronic trading platform Archipelago in 2006.

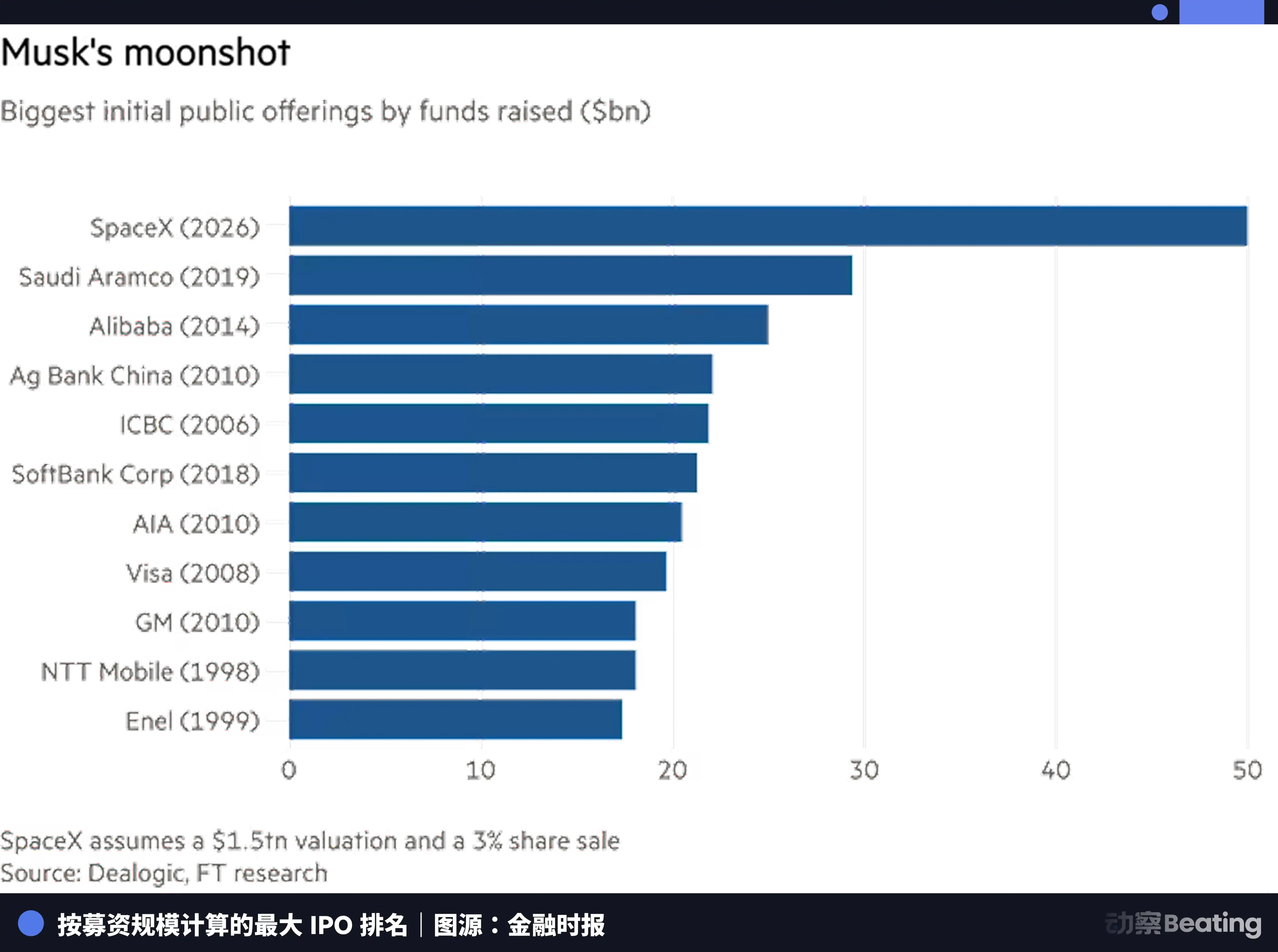

Another twenty years later, in 2026, SpaceX is negotiating with Nasdaq, demanding to be included in the Nasdaq 100 index within 15 trading days after its IPO. If that can't be done, it can go to the NYSE.

Each time, the rules yield to a force large enough. But this time is different.

The rise of Nasdaq in 1971 was a new type of exchange using technology to pry open the old rules. The transformation of the NYSE in 2006 was the old exchange surrendering to new technology. The scene in 2026 involves a company that hasn't even gone public yet, demanding that a market system with a two-hundred-year history change its procedures for it.

This is not just a story about SpaceX's IPO; it's a cross-section of the changing direction of gravitational pull in the capital markets.

The Funding Window Is No Longer the Sole Domain of IPOs

What is the purpose of going public? The textbook answer is fundraising.

This answer was accurate in the 1990s. Back then, public markets were almost the only place that could provide large-scale, long-term capital for companies. SoftBank's Vision Fund hadn't been created yet, sovereign wealth funds didn't touch tech stocks, and the private secondary market barely existed. If you wanted truly big money, there was only one path: knock on the exchange's door, undergo audits, scrutiny, pricing, and then pray for a smooth roadshow.

Microsoft went public on Nasdaq on March 13, 1986, raising $61 million, with a market capitalization of about $777 million. The company's annual revenue was less than $200 million at the time. It needed that money to expand its product line, recruit engineers, and seize the standard position in PC operating systems.

Forty years later, this logic is no longer the only answer.

SoftBank Vision Fund, Tiger Global, Coatue, a16z... an entire ecosystem of institutional capital has pushed the ammunition in the private market to an unprecedented scale. A company can grow all the way to a valuation of $50 billion or even higher in the private market, without ever touching the public market.

Revolut is the most direct proof. On November 24, 2025, this London-based digital bank completed a secondary equity round, reaching a valuation of $75 billion. Lead investors included Coatue, Greenoaks, Dragoneer, and Fidelity, with participants including a16z, Franklin Templeton, and even Nvidia's venture arm, NVentures.

With full-year 2024 revenue of $4 billion, up 72% year-over-year, and pre-tax profit of $1.4 billion. CEO Nik Storonsky, when asked about the IPO timeline, said: We are building the world's first truly global bank; an IPO is not a priority.

What does $75 billion mean? This figure exceeds the market capitalization of Barclays, Deutsche Bank, and Lloyds Bank on the public market. A private company obtained a higher valuation in a private transaction than listed banks.

And recently, there have been reports that Revolut is planning another secondary share sale in the second half of 2026, targeting a $100 billion valuation.

SpaceX completed a similar layout earlier; its private rounds covered the entire capital needs for rocket development, Starlink deployment, and deep space exploration. According to Reuters, SpaceX plans to IPO at a valuation of approximately $1.75 trillion. If it goes public, it would become the largest IPO in history by funds raised and immediately rank as the sixth most valuable company in the U.S., behind only Nvidia, Apple, Microsoft, Amazon, and Alphabet.

Then there's Stripe. This payments company processed $1.9 trillion in transaction volume in 2025, a 34% increase. In February 2026, through an employee stock buyback round, its valuation reached $159 billion. Co-founder John Collison was blunt in an interview: An IPO is just "a solution in search of a problem" for us.

These companies are not avoiding going public because market conditions are bad; it's because they no longer urgently need the public market's money. The private market provides capital on a similar scale,附带 fewer regulatory constraints and disclosure requirements.

But not needing money doesn't mean not needing to go public.

Index Inclusion, the Real Prize

Fundraising is only the first layer of motivation for going public; the second is liquidity for people.

SpaceX has thousands of employees holding options and RSUs. The company has allowed some employees to cash out early through tender offers in recent years, but this method has limits on amount, frequency, and the pricing is company-led, not market-priced.

For a company with tens of thousands of employees, this pipeline is too narrow. Only the public market can provide a real, continuous, market-priced liquidity exit.

The same pressure exists on the VC side. Revolut's shareholder list includes a16z, Fidelity, Coatue. The LPs of these funds need not paper valuation growth, but实实在在的现金回报 (real cash returns). The private secondary market can solve part of the exit demand, but its scale and efficiency are far inferior to the public market. When a fund matures, LPs want to take the money and leave; paper wealth doesn't count.

So these companies still need to go public, but the combination of driving variables has changed. The need for fundraising has decreased significantly. Employee liquidity and VC exits are still rigid demands. And on top of these traditional motivations, a structural force that has been underestimated by most people over the past decade is rapidly increasing in weight.

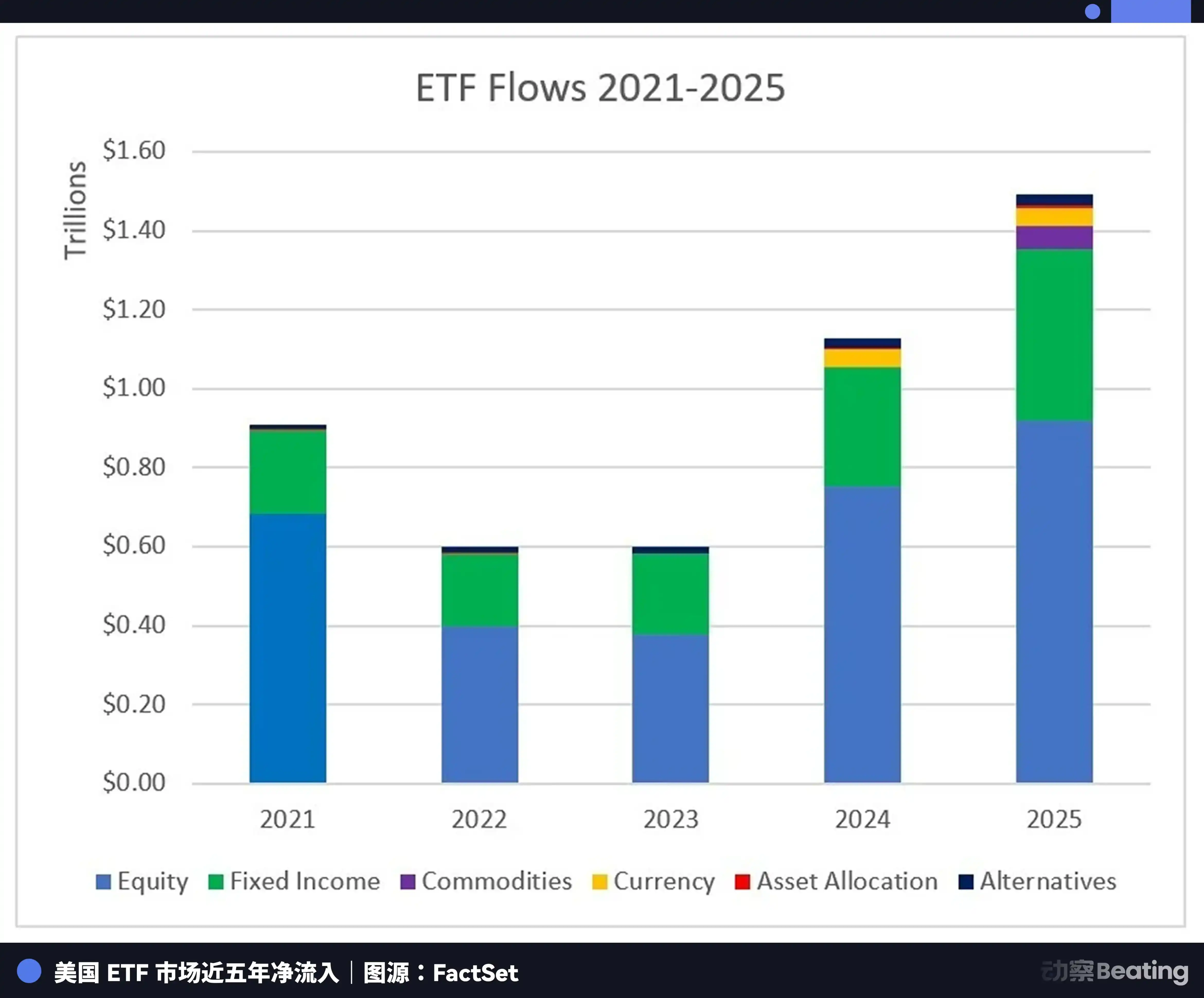

In 1975, John Bogle at Vanguard created the first index fund for ordinary investors, tracking the S&P 500. Wall Street's reaction was ridicule. Active stock picking was professional; passive following was a lazy strategy. No one wanted to buy a mediocre product.

Half a century later, the lazy won.

As of March 2025, U.S. passive funds (including mutual funds and ETFs) managed assets reached $15.96 trillion, accounting for 51% of all mutual fund industry assets, surpassing actively managed funds for the first time. In the full year 2025, the U.S. ETF market saw net inflows of $1.49 trillion, a historical record, with equity ETFs absorbing $923 billion.

Behind these numbers lies a mechanical logic. Once a stock is included in an index, all funds tracking that index must配置 (allocate to) it according to its weight. No subjective judgment, no waiting for the right time, mandatory buying. And as long as the company remains in the index, the fund holds it perpetually.

It's important to clarify: passive funds are price takers, not price setters. Price discovery for stocks is still primarily done by active capital: analyst research, institutional trader博弈 (games), hedge fund bets.

But what passive funds do is equally crucial: they provide a huge, stable, non-discretionary holding base. This base won't panic sell because of a missed quarterly earnings report, won't slash positions because the CEO tweeted something; it's ballast.

For a company of SpaceX's caliber, the value of this ballast is quantifiable.

SpaceX's expected IPO valuation is about $1.75 trillion, which would directly place it in the top six of the Nasdaq 100. Under current rules, newly public companies typically need to wait up to a year to be eligible for inclusion in major indices like the S&P 500 or Nasdaq 100. This waiting period was originally designed to verify whether the company could withstand the liquidity pressure from large-scale institutional buying.

But for SpaceX, this waiting period means that funds tracking the Nasdaq 100, including the over $400 billion Invesco QQQ, cannot allocate to one of the world's top ten most valuable companies for a whole year. The tracking error would become unacceptable.

The pressure isn't on SpaceX; it's on the index funds themselves.

Nasdaq therefore proposed the "Fast Entry" rule: if a newly listed company's market cap can place it within the top 40 of existing index components, it can be加速纳入 (accelerated for inclusion) 15 trading days after listing. This rule is still under review, but Nasdaq itself admits it was designed to attract highly valued private companies like SpaceX, Anthropic, and OpenAI.

SpaceX made rapid inclusion a prerequisite for choosing an exchange. It has the leverage to do so because the inherent demand of the passive index system gives it bargaining power.

Some might ask, if the core goal is index inclusion, why not do a direct listing? Direct listing saves underwriting fees,同样能挂牌 (also allows listing),同样能进指数 (also allows index entry).

The answer lies in scale.

SpaceX's IPO is expected to raise over $25 billion. It needs to create a sufficiently large float on the first day of trading to meet the liquidity threshold for passive fund allocation. A direct listing has no new share issuance; the first-day float depends entirely on how many existing shareholders are willing to sell. For a company with a $1.75 trillion market cap, if the first-day float is too small, passive funds simply cannot complete their position building, causing severe price distortions.

The structured issuance of an IPO is precisely the tool to pave the way for large-scale passive capital entry. This logic also explains, in reverse, why Revolut and Stripe are in no hurry.

Revolut's $75 billion, placed in the Nasdaq 100, would have limited weight,撬动 (leveraging) a disproportionate amount of passive buying power. And its delay has other practical reasons, such as its banking license still being finalized, and management wanting a few more quarters of profit data to solidify the valuation narrative.

But the arithmetic of index weight is also part of the calculation. Stripe's $159 billion valuation is already significant, but John Collison says an IPO is not a priority. The underlying judgment might be similar: wait until the valuation grows further and the weight upon index inclusion becomes more meaningful, then the structural benefits of an IPO can be maximized.

The value equation of going public is being rewritten.

Fundraising has taken a back seat. Employee liquidity and VC exits are the fundamentals. And the perpetual holding base brought by index investing is becoming a new variable determining the timing of an IPO. It's not the only variable, but its weight has been rising steadily over the past decade. And in the case of SpaceX, it has been publicly placed on the negotiating table for the first time.

So, what is the role of the exchange in this game?

Ambushed by the Hyperliquids

Nasdaq changed its index inclusion rules for a company that hasn't even gone public yet.

And ICE, the parent company of the NYSE, invested $2 billion in the prediction market platform Polymarket in October 2025, at a valuation of about $8 billion. In March 2026, ICE又 (again) took a stake in the crypto exchange OKX at a $25 billion valuation, gaining a board seat.

On the surface, these two things are competitive strategies, but at their core is the same anxiety: the scarcity of the gatekeeper is disappearing.

There was once an unwritten boundary between the NYSE and Nasdaq. Traditional industries went to the NYSE; technology and emerging industries went to Nasdaq. This boundary held for decades, with both sides maintaining monopolies in their respective lanes.

This默契 (tacit understanding) is now broken.

The structure of ICE's investment in OKX is worth a closer look. OKX's 120 million users will gain access to ICE's U.S. futures market and tokenized trading of NYSE-listed stocks. ICE, in return, gains OKX's real-time cryptocurrency pricing data for developing regulated crypto futures products.

ICE Vice President Michael Blaugrund was blunt: in the future, ICE's competitors might not necessarily be traditional institutions like CME or Nasdaq, but could be DeFi protocols or super apps. He named Robinhood and Uniswap.

A company that owns the NYSE, publicly admitting that its future opponents could be a decentralized protocol. This statement itself is a signal.

The logic behind the Polymarket investment is similar. ICE isn't buying a prediction market platform; it's buying an entry point to an on-chain trading infrastructure. The cooperation includes institutional distribution of Polymarket data and future tokenization projects.

In the 1990s, Nasdaq used electronic trading to break through the NYSE's floor monopoly. The weight shifted, but the structure didn't disappear. Today, on-chain infrastructure is replaying this script,蚕食 (nibbling away at) the share of derivatives and alternative assets on the fringes of the exchanges.

Hyperliquid provides the most specific cross-section.

This decentralized exchange had a total trading volume of $2.95 trillion in 2025, with a daily average volume of about $8.34 billion, annual revenue of $844 million, and over 600,000 new users. For reference, Coinbase's trading volume during the same period was about $1.4 trillion. An on-chain protocol without a corporate entity, without a CEO making public appearances, had twice the trading volume of the Nasdaq-listed company Coinbase.

More noteworthy is the change in its user structure.

In 2025, Hyperliquid launched on-chain perpetual contract trading for the S&P 500, Nasdaq index, gold, crude oil, Nvidia, Tesla, and other global stocks through its HIP-3 protocol. Among the top 30 markets on its tokenization platform trade.xyz, crypto trading pairs accounted for only 7. On March 15, the total open interest in HIP-3 markets hit a record high of $1.43 billion, increasing 100-fold in six months, with trade.xyz alone accounting for ninety percent.

In March, escalating tensions in the Middle East caused sharp fluctuations in oil prices. Traditional futures exchanges were closed on the weekend, and a group of professional traders flooded into Hyperliquid. These were not retail investors; they were professional futures traders attracted by 24/7 non-stop trading, on-chain transparency, and higher capital efficiency. While traditional exchanges were operating on a fixed open/close schedule, on-chain markets had turned the concept of "all-weather liquidity" into a reality.

These numbers and the exchanges' current IPO business are not on the same track; direct competition between the two is very limited. But ICE's worry isn't about today; it's about the trend.

When on-chain infrastructure can handle perpetual contract trading for global stocks, when professional traders start using on-chain tools for hedging and speculation, when the liquidity of tokenized stocks gradually approaches that of traditional exchanges, the moat of the exchanges is being bypassed bit by bit.

The NYSE chose to invest in on-chain players; Nasdaq chose to change its own rules. Both actions point to the same conclusion: the era of relying on垄断 (monopoly) to maintain position is over; active expansion is the only option.

Epilogue

In 1971, no one thought Nasdaq's electronic quotation terminal was a threat. In 2006, no one thought the NYSE would主动拆掉 (actively dismantle) its own trading floor. In 2026, no one knows how far Hyperliquid and the on-chain infrastructure it represents will go.

But after each rule concession, the old structure didn't disappear; it was重新分层 (re-stratified).

The NYSE still exists today, still powerful, but no longer独占 (monopolizes) pricing power. Nasdaq will become stronger after SpaceX's IPO; that perpetual holding base will continue to grow with expanding market capitalization. The logic behind ICE's investments in OKX and Polymarket is the same: if on-chain trading is inevitable, then become the infrastructure provider for the on-chain world, rather than waiting to be bypassed.

The on-chain system won't disappear either; it will likely grow stronger, becoming the new infrastructure.

In a world where two systems coexist, where will the next company large enough and confident enough to set conditions go knocking? Or, to put it another way, will it even need to knock?