In the previous article, we introduced how Strategy brought new marginal buying pressure to Bitcoin through STRC.

However, two incidents occurring in the new ex-dividend cycle have made some traders uneasy about the "new paradigm of supply and demand dynamics" that STRC brings to Bitcoin.

Saylor Softens Stance

After market hours on May 5th, during the Q1 2026 earnings call for MicroStrategy, Saylor publicly acknowledged for the first time that the company might sell a portion of its Bitcoin to pay dividends.

Saylor's statement can be interpreted in three ways.

The first interpretation is that Saylor is trying to let the market know and digest this possibility in advance to avoid a violent reaction if it actually happens. This is a "public relations" move to provide a price buffer for BTC.

The second interpretation is straightforward: Saylor's promise to "never sell Bitcoin" is the cornerstone supporting MSTR's premium and the entire Bitcoin treasury narrative. Once Saylor himself opens a crack, the market will reassess the stability of the entire system.

The third interpretation: MicroStrategy's previous financing relied mainly on two tools: issuing MSTR common stock and issuing convertible bonds. Preferred stock has only become the main tool in the past year, but the issuance ceiling is still limited by the secondary market's absorption capacity. The only remaining tools that don't create future obligations and are large enough in scale are ATM (at-the-market) offerings of MSTR common stock. The problem is that MSTR's mNAV must be above 1.22x for new common stock issuance not to dilute the BTC per share. Currently, MSTR's mNAV is not far from this threshold. Saylor uses the relatively gentle method of "possibly selling Bitcoin" to attract market attention, making the relative cost of continuing to issue MSTR common stock seem more acceptable.

Looking at the balance sheet, MicroStrategy's current annual dividend and interest payments total about $1.5 billion, with monthly payments around $125 million. STRC accounts for about $978 million of this, or 65%. As of Q1 this year, the company had approximately $2.25 billion in USD reserves, which, according to management, can cover 18 months of dividend payments.

If STRC issuance stalls and the cash reserves are depleted, the only remaining option would be to sell BTC to cover dividend payments. At a BTC price of $80k and annual interest and dividend payments of $1.5 billion, Strategy would need to sell about 18,519 BTC per year, equivalent to 2.3% of its total holdings.

As long as BTC appreciates by at least 2.3% annually, this selling pressure can be absorbed by the increase in portfolio value. Over a multi-year horizon, BTC's compound annual return is often in the double or even triple digits, making 2.3% almost a non-constraint.

However, BTC has also experienced single-year drawdowns of -77% in 2018 and -65% in 2022. If Strategy sells 2.3% of its BTC holdings during a bottom, the company's balance sheet would deteriorate severely.

MicroStrategy has net purchased about 77,000 BTC through STRC so far in 2026. If a sell scenario is triggered and BTC falls back near Strategy's average cost of $75,537, selling 2.3% of the total holdings would be equivalent to 25% of the year-to-date purchase volume.

In other words, Saylor's selling in one year could offset four months of buying.

STRC "Weakens"

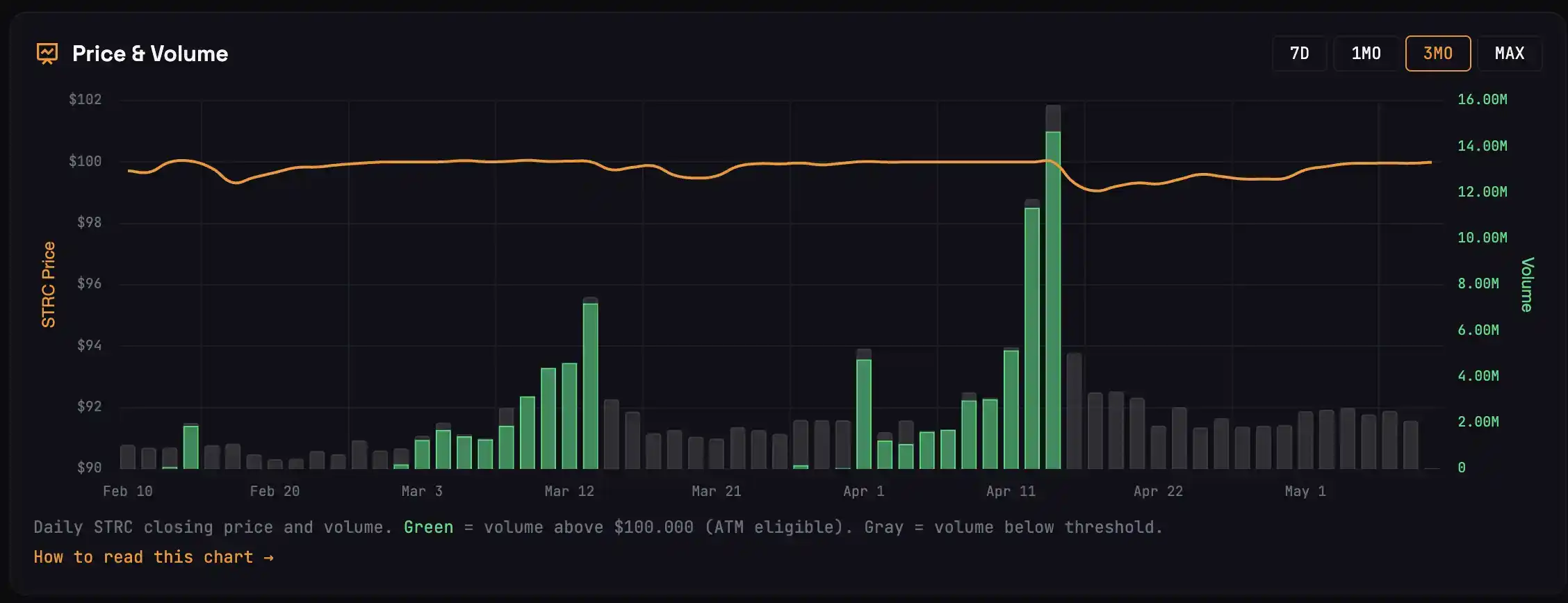

In the March ex-dividend cycle, STRC traded above $100 for 13 days before the ex-date, with cumulative volume of 3.42M shares, corresponding to about 22,000 BTC purchased. In the April cycle, STRC generated buying pressure for about 47,000 BTC.

Now, with only 5 trading days left before the May 15th ex-date, STRC has not returned to its $100 par value in the May cycle, meaning the corresponding BTC buying is 0.

To understand why this cycle is suddenly different, we can categorize STRC buyers into four types:

· The first type consists of arbitrageurs who rush in a few days before the ex-date. They buy STRC before the ex-date, collect the dividend on the ex-date, and then sell. The peak volume on the ex-date mainly comes from these funds, and their sell orders are the main driver of STRC's price decline after the ex-date.

· The second type consists of arbitrageurs who enter only after the ex-date. STRC typically falls to the $99.20 to $99.50 range after the ex-date. They buy and place sell orders around $99.95 to $99.99, waiting for STRC to return to par value. These funds don't need STRC to actually reach $100 to profit; their sell walls are the fundamental reason STRC lingers below par value.

· The third type consists of medium-to-long-term holders who treat STRC as a wealth management product. They don't actively arbitrage but may redeem small amounts when they need funds. These occasional sell orders join those of the second type, placing limit orders near the $100 par value.

· The fourth type consists of true long-term holders who do not sell. They have almost no impact on the price dynamics of each ex-dividend cycle.

If the source of funds leading to STRC issuance is arbitrageurs, the overall market behavior will lean towards "selling near the $100 par value."

This is what happened last month.

In March and April, Strategy raised nearly $5 billion through STRC. An inflow of this magnitude could only be contributed by arbitrageurs, as long-term holders wouldn't suddenly increase by that much.

This also led to stronger arbitrageur selling pressure in April than ever before.

Strong selling pressure means STRC fell deeper after the April ex-date and took longer to return to $100 than in previous cycles. A significant portion of the first type of funds didn't manage to exit in time and got stuck at lower prices. These funds, having taken a loss, might not participate in the May arbitrage.

Furthermore, the external environment is changing.

The S&P 500 continues to hit new highs, altering the opportunity cost for fixed-income funds to buy STRC. After all, many sectors in the U.S. stock market can see single-day gains exceeding STRC's annual yield (11.5%).

Strategy's management has foreseen this issue and submitted an amendment on April 17th to make STRC pay dividends twice a month. Semi-monthly dividends could reduce the decline on each ex-date and spread out the arbitrage profits. However, this amendment won't take effect until July 15th; next week's ex-date will still follow the monthly rule.

Reverse Flywheel

The previous article discussed Strategy's flywheel: Money buying STRC is levered threefold to flow into BTC; BTC's rise improves STRC's collateral quality; more funds flow into STRC. Each link pushes the next higher.

What if the flywheel spins in reverse?

STRC fails to return to par, Strategy's at-par issuance (ATM) window closes, no new cash buys BTC, BTC loses marginal buying pressure, price comes under pressure, STRC's collateral base weakens, fixed-income investors demand higher credit spreads. Widening spreads either force MicroStrategy to raise the dividend rate (increasing interest burden) or investors continue selling STRC, making it harder for the price to return to the $100 par value.

Each link pushes the next lower.

Saylor's statement about "possibly selling some BTC" is essentially pre-pricing the end of this reverse cycle.

In concrete numbers: In April, Strategy's net BTC buying via STRC was about $4.1 billion. If STRC issuance in May falls back to the range of $1 billion, and simultaneously BTC appreciation doesn't reach the 2.3% threshold, triggering Strategy's sell-BTC-for-dividends plan, the monthly net contribution could plummet from $4.1 billion to just a few hundred million dollars, a contraction of over 90%.

The market's argument over the past few months that "STRC buying" provides bottom support for BTC would be disproven, and BTC's price would face a sharp correction.

It must be acknowledged this is only one possible path. If STRC smoothly returns to $100 next week and the issuance scale is substantial, all the aforementioned concerns will be postponed.

Optimistic Signals

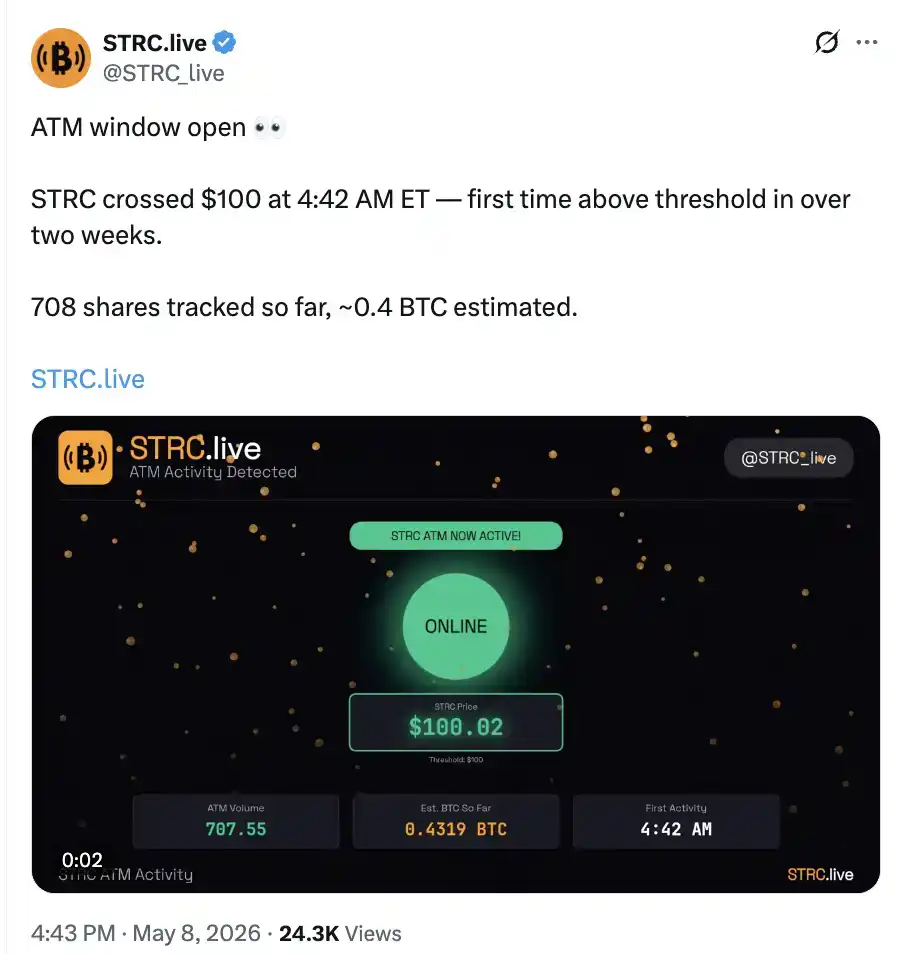

During the pre-market session on May 8th, STRC saw its first issuance in this ex-dividend cycle, corresponding to 0.4 BTC purchased.

The absolute scale is negligible, but the significance lies in the shift from zero to one.

Simultaneously, the Coinbase premium briefly turned positive and returned to April's levels.

Whether BTC, which appears to be losing upward momentum, will fall back to February's range or attack $90,000, STRC's performance next week will play a key role.