Author: Ba Xiao Ling, Wu Xiaobo Channel

The suspense itself was not great, only the final push was needed.

After the expectation of "the Renminbi is about to break through 7" lingered for nearly a month, an analyst from Goldman Sachs provided a crucial assist.

Recently, Goldman Sachs released the "2026 Global Stock Market Outlook." When mentioning the Renminbi, according to its Dynamic Equilibrium Exchange Rate Model (GSDEER), Goldman Sachs calculated the fair value of the Renminbi, showing that it is undervalued by nearly 30% against the US dollar.

However, the slogan is more eye-catching than the numbers. The report stated:

The degree of undervaluation of the Renminbi exchange rate relative to the US dollar is comparable to that of the mid-2000s.

In 2000, the annual average exchange rate of the US dollar to the Renminbi was approximately 8.28. Subsequently, the Renminbi entered a nearly ten-year appreciation cycle, with its exchange rate against the US dollar rising to around 6.1.

Goldman Sachs' calculations gave the market more confidence to "be bullish," prompting the offshore Renminbi, which was already in an appreciation channel, to suddenly gain momentum.

On the morning of December 25, the US dollar to offshore Renminbi exchange rate quickly broke through the 7.0 mark, hitting a 15-month high and officially re-entering the "6 era."

2005—2025 USD/RMB Trend

Source: CnYES

At the same time, the onshore Renminbi exchange rate touched a low of 7.0053, just one step away from "breaking 7." The central parity rate of the Renminbi against the US dollar announced by the China Foreign Exchange Trade System was also raised by 79 basis points. Now, with the "shoe dropped," we can finally ask these questions:

Why was the Renminbi able to chart an independent course in 2025? What changes does the entry into the "6-era" exchange rate mean for our business operations and personal asset allocation?

Is "Breaking 7" Short-Term or Long-Term?

Looking at the whole year, the Renminbi exchange rate has performed unusually.

In April this year, the Renminbi exchange rate hit a low of 7.429, and the market was still worried about the risk of Renminbi depreciation. Unexpectedly, as the year-end approached, the trend of the Renminbi exchange rate reversed.

This is partly due to timing.

As a rule, near the end of the year, domestic export enterprises need to settle accounts with suppliers, converting the US dollars earned throughout the year into Renminbi for "closing the books" and distributing year-end bonuses, etc. This triggers seasonal foreign exchange settlement demand.

When more and more people "need" Renminbi, starting from the end of November, the "price" of Renminbi rose, and the timeline matches.

December 24, busy operations at a foreign trade container terminal

Moreover, due to the recent "pleasing surge" of the Renminbi, export enterprises that had previously hoarded US dollars, in order to avoid further losses from exchange rate fluctuations, more or less engaged in a rush to "settle foreign exchange," which further pushed up the appreciation of the Renminbi.

It is worth mentioning that this wave of demand this year is apparently larger than in previous years.

According to data released by the General Administration of Customs, in the first 11 months of this year, China's goods trade maintained growth, with the total import and export value reaching 41.21 trillion yuan, a year-on-year increase of 3.6%. In the first 11 months, China's trade surplus exceeded 1 trillion US dollars for the first time.

This means that some export enterprises have more foreign exchange income than in previous years.

Wang Qing, chief macro analyst of Oriental Jincheng, believes that as the year-end approaches, the increase in corporate foreign exchange settlement demand is also driving the seasonal strengthening of the Renminbi; especially after the recent continuous appreciation of the Renminbi against the US dollar, the accumulated settlement demand from the previous period of high export growth may be accelerating its release.

However, Huatai Futures wrote in its "Huatai Futures - Foreign Exchange Annual Report: Getting Better, Renminbi Enters Appreciation Channel": Due to the impact of the inverted China-US interest rate differential, the cost-effectiveness of foreign exchange settlement and holding foreign exchange has become more comparable, leading to a more differentiated and balanced corporate foreign exchange settlement strategy. Therefore, although the year-end "foreign exchange settlement wave" this year will provide marginal support for the Renminbi in stages, it does not constitute a trend-leading factor.

The appreciation of the Renminbi also has some geographical advantages.

In 2025, the Federal Reserve implemented three interest rate cuts, which directly led to the weakening of the US dollar index. As of December 25, the US dollar index fell by 9.69% this year, not only breaking below the 100 mark to close at 97.97 but also recording its largest annual decline in nearly 8 years.

December 10, the Federal Reserve's third interest rate cut

The exchange rate is a "seesaw." When the US dollar weakens, it means non-US currencies, including the Renminbi, strengthen, and the Renminbi achieves "passive appreciation."

Another contributing factor is that after Trump took office, he launched a global "tariff war," disrupting the long-standing global trade system based on existing rules.

When trade flows become uncertain, the cost of trade settlement and supply chain financing denominated in US dollars naturally increases, further shaking the foundation of the US dollar as an ideal trade settlement currency.

Coupled with the 35-day US government shutdown and Moody's, one of the three major rating agencies, downgrading the US sovereign credit rating, global capital began to seek safe havens, leading to a large-scale outflow of US dollar assets from the United States—the Renminbi and Renminbi assets thus welcomed their own "value reassessment."

According to data from global fund flow monitoring agency EPFR Global, during the period from May to October 2025, foreign capital focused on Hong Kong stock investment equity funds saw a cumulative net inflow of 67.7 billion Hong Kong dollars, completely reversing the net outflow trend during the same period in 2024.

The appreciation of the Renminbi is, most importantly, due to human factors.

On December 11, the World Bank, in its latest China Economic Brief, raised China's GDP growth rate by 0.4%, and the International Monetary Fund (IMF) raised China's GDP growth rate for this year by 0.2%, expecting it to reach 5%.

The simultaneous upward revision of China's economic expectations by two international institutions is clearly a full affirmation of China's current economic operation and long-term development potential.

Among them, the stability of exports provides the most fundamental confidence for the appreciation of the Renminbi exchange rate.

On one hand, the record trade surplus is a solid foundation for the Renminbi exchange rate. On the other hand, the quality of exports has also improved.

Similarly, data from the General Administration of Customs show: In the first 11 months of this year, China's integrated circuit exports reached 1.29 trillion yuan, an increase of 25.6%; automobile exports reached 896.91 billion yuan, an increase of 17.6%. This means that the mainstay of exports has shifted from traditional labor-intensive products to high-end manufacturing industries such as shipbuilding, integrated circuits, and new energy vehicles.

Export vehicles parked at the port

Guan Tao, Global Chief Economist of Bank of China Securities, believes: The increased diversification of export markets, the accelerated transformation and upgrading of domestic manufacturing, and the enhanced competitiveness of export commodities have affected China's commodity exports to maintain rapid growth, providing important support for the steady and rising share of China's exports in the global market.

Renminbi Appreciation and Personal Investment

Next, let's answer a question everyone cares about most—is this Renminbi appreciation a positive or negative for A-shares?

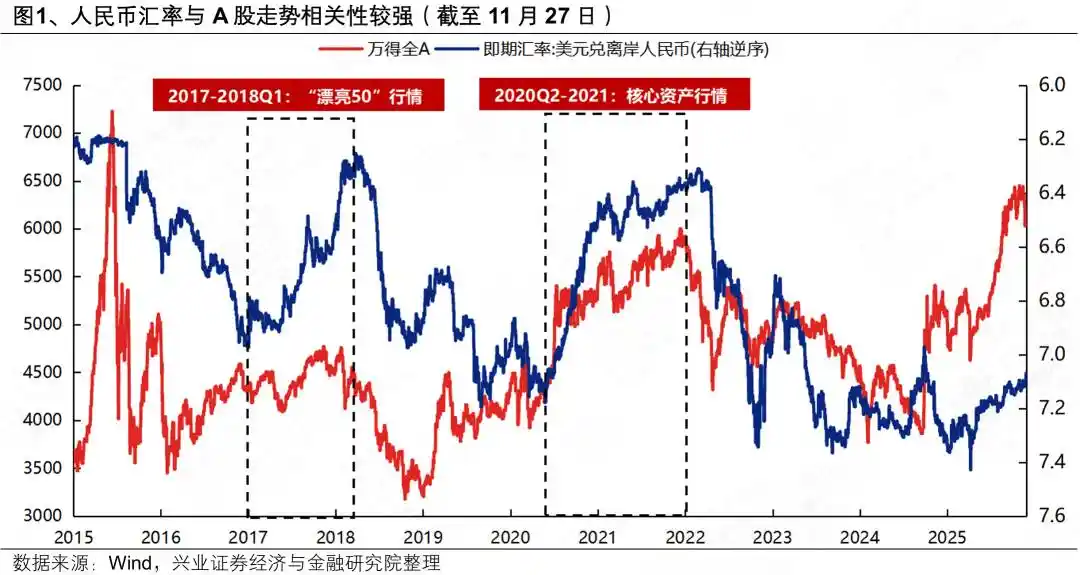

Regarding the impact of the exchange rate on A-share trends, there have been many studies over the years. The Xingye Securities Strategy Team led by Zhang Qiyao believes that after the 2015 exchange rate reform, the Renminbi exchange rate and A-share trends show a significant positive correlation.

From the chart of the correlation between the Renminbi exchange rate and A-share trends, we can also see that since 2017, the correlation between the Renminbi and A-share trends has become more obvious.

For example, during the "Nifty 50" period from 2017 to the first quarter of 2018, and during the Renminbi appreciation period from the second quarter of 2020 to 2021, A-shares were in a bull market. Correspondingly, foreign capital became an important incremental driver of the rise of the Chinese stock market.

In addition, Goldman Sachs once conducted a study on US stocks and concluded: When the fundamentals do not diverge, a 0.1 percentage point increase in the exchange rate leads to a 3%–5% increase in stock valuation.

Of course, because the mechanism of influence between the exchange rate and stock prices is relatively complex, we cannot assert that as long as the Renminbi appreciates, individual stocks and the overall market will definitely rise. But based on various judgments, this Renminbi appreciation is expected to stimulate further rises in A-shares.

However, Renminbi appreciation will indeed have an impact on different industries, thereby affecting the stock prices of related listed companies.

The appreciation of the offshore Renminbi means that Chinese goods denominated in the local currency become more expensive in the international market, naturally weakening price competitiveness for foreign buyers, and export orders may decrease.

Especially for traditional export-oriented industries, such as home appliances and textiles, because these industries have relatively thin profit margins and are more sensitive to exchange rate fluctuations, the impact on their profits will be more obvious.

Everything has two sides. Renminbi appreciation is also a major positive for certain industries. For example, domestic import-dependent industries can directly benefit from this appreciation.

According to import and export data from the National Bureau of Statistics, China's "net import" industries, including energy, agriculture, materials, and other fields, directly benefit from this appreciation.

At the same time, industries with relatively high US dollar debt also benefit from Renminbi appreciation, such as those within the scope of the Hong Kong Stock Connect with a high proportion of US dollar debt in short-term liabilities, such as the internet, shipping, aviation, utilities, energy, and other industries.

In addition, Renminbi appreciation will also change the trading style of individual investors.

At the beginning of the year, "US dollar deposits" and US dollar treasury bonds were very popular. Some investors exchanged a considerable amount of Renminbi for US dollars for investment. As a result, with the sharp appreciation of the Renminbi, US dollar deposits became "negative yield," and even with a 5% yield on US dollar treasury bonds, the exchange rate loss would only make it roughly equivalent to the one-year fixed deposit interest rate.

Of course, some people ask, since the Renminbi is strengthening now, can they buy more US dollars and save them for future use while the Renminbi is appreciating?

For individuals, if it is for cross-border shopping, it might be a good choice. Renminbi appreciation is equivalent to enjoying a discount when consuming abroad, and when shopping overseas and settling in US dollars, paying in Renminbi will also be 5%–10% cheaper than before.

But if it is purely for speculation, it is better to be cautious. Because the probability of large fluctuations in the Renminbi exchange rate is not high, do not blindly chase rises and kill falls by converting Renminbi into US dollar deposits for speculation.

Where to Go After "Breaking 7"?

It is worth noting that the appreciation we are talking about now mainly refers to the Renminbi's appreciation against the US dollar, not a "comprehensive strengthening."

According to data from the China Foreign Exchange Trade System, from the beginning of this year to now, the Renminbi exchange rate against the CFETS Renminbi Exchange Rate Index, the BIS currency basket Renminbi Exchange Rate Index, and the SDR currency basket Renminbi Exchange Rate Index have all declined, with two major indices falling below 100.

These three indices are the "average report card" measuring the comprehensive value of the Renminbi against a basket of foreign currencies.

The weakening of the indices means that although the Renminbi has appreciated significantly against the US dollar, its overall value level against a basket of other foreign currencies, such as the British pound and the euro, is declining.

But there is a consensus among institutions, including Goldman Sachs, that with the continuous development of China's economy and the deepening of Renminbi internationalization, the "moderate appreciation" of the Renminbi is expected to become a major trend.

For example, Yuekai Securities believes that in the past two years, domestic prices have been low while overseas inflation has been high. The central level of the CFETS Renminbi Exchange Rate Index has even moved downward, and the Renminbi exchange rate has the momentum to catch up. In 2026, the Renminbi exchange rate against the US dollar will remain strong, and "6.8" might be a key point.

According to a summary by Bloomberg, experts from six major international investment banks generally believe that the US dollar will continue to weaken against major currencies. By the end of 2026, the US dollar index will fall by about 3%—this will form a trend of the Renminbi continuing to strengthen passively.

However, whether the Renminbi continues to appreciate or fluctuates in the future, it is unlikely to show overly unexpected trends.

The Central Economic Work Conference held not long ago has emphasized for four consecutive years the need to "keep the Renminbi exchange rate basically stable at an adaptive and equilibrium level."

In addition, as the central bank stated: "The medium- and long-term Renminbi exchange rate has a solid foundation. We will continue to adhere to the decisive role of the market in the formation of the exchange rate, maintain exchange rate flexibility, strengthen expectation guidance, prevent the risk of exchange rate overshooting, and keep the Renminbi exchange rate basically stable at an adaptive and equilibrium level."

Even Goldman Sachs said: "We expect Renminbi appreciation to be gradual and managed, but even so, we believe it is still expected to outperform forward pricing."

For individual investors, we should not focus on predicting the precise point of the exchange rate, but on understanding the trend, adapting to industrial upgrading, and making good use of hedging tools. We must seize the opportunities brought by appreciation while also guarding against the risks brought by fluctuations.