Amid the uncertain situation of the Iran war, the crude oil market is experiencing significant volatility.

At the same time, a rare phenomenon has appeared on Trade.xyz's WTIOIL-USDC crude oil perpetual contract: the annualized funding rate has stabilized between -300% and -400%. This means that any trader willing to go long at this moment can receive profits equivalent to 1% of their principal daily from the shorts.

The market doesn't give away money for no reason. To understand this反常的 negative funding rate, we need to start with the basics of futures trading.

Rollover

Crude oil futures are a series of contracts arranged by delivery month. Contracts for May delivery, June delivery, July delivery, each with its own price. When the front month is about to expire, the market must switch from the old contract to the new contract; this action is called rollover.

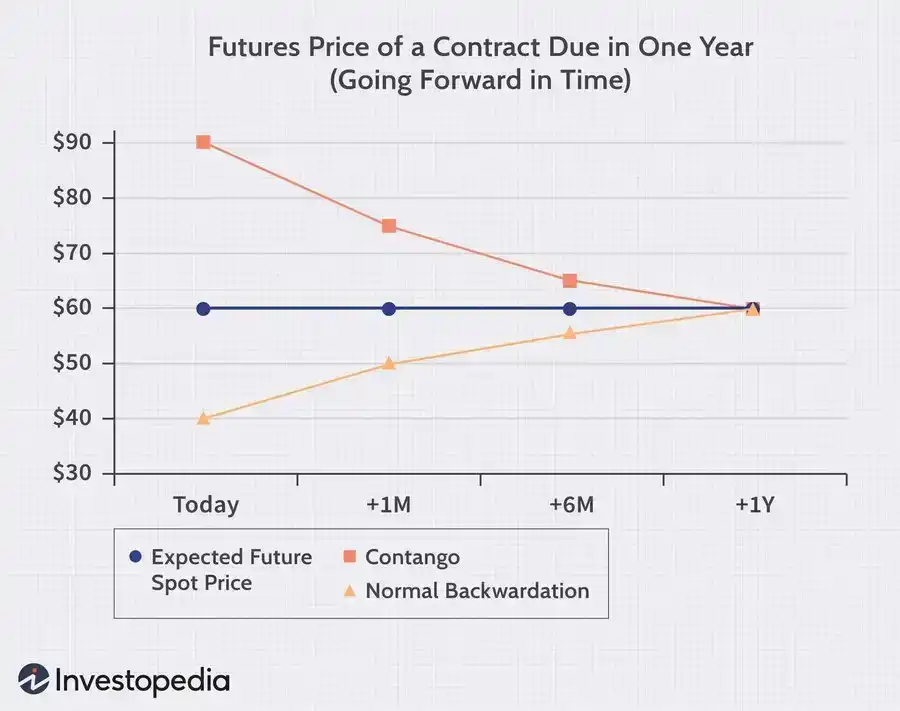

Under normal circumstances, back-month contracts imply that oil merchants will store the oil for several additional months, incurring extra storage costs. Therefore, the delivery price should logically be higher. The market phenomenon where future contracts are more expensive than the near month is called Contango. Conversely, the situation where the near month is more expensive than the far month is called backwardation. This usually occurs when there is a current shortage, and everyone wants to get the oil immediately.

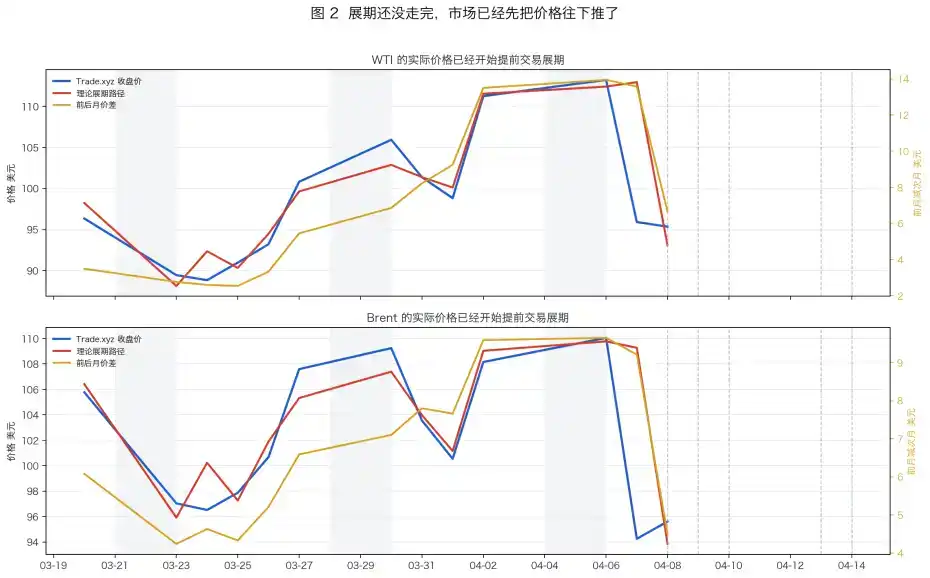

During this rollover period for Trade.xyz's crude oil, the crude oil futures market was in this near-high, far-low structure.

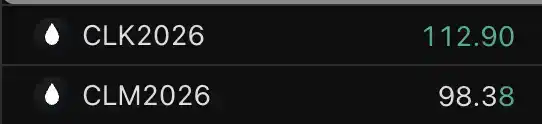

From late March to early April 2026, the WTI crude oil curve was in an extreme state of backwardation. As shown in the chart above, the price of the May contract (front month) remained consistently higher than the June contract (back month), with the spread widening to over $14 at one point.

The WTIOIL-USDC perpetual contract on Trade.xyz has its oracle pegged to this front-month May contract.

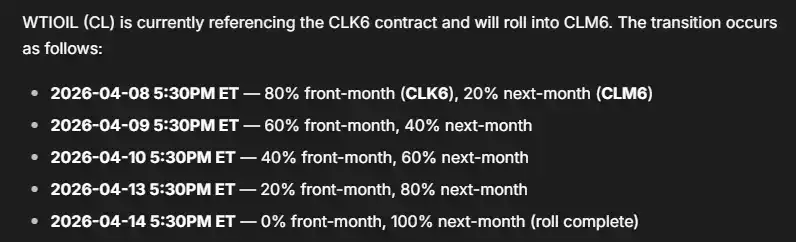

But we won't be trading this May contract forever. It must be rolled over to the next June contract. So how is the rollover accomplished?

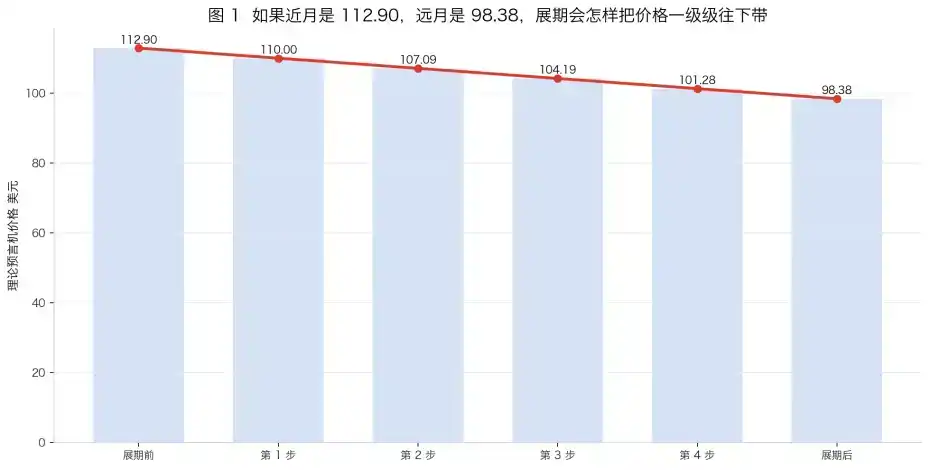

According to the Tradexyz documentation, the oracle will take 5 trading days to gradually shift the price weighting from 100% front-month contract to 100% back-month contract.

Against the backdrop of "backwardation," this means the oracle price on Tradexyz will drop from the front-month price to the back-month price over 5 trading days.

Market participants familiar with this mechanism have a clear expectation of the contract price after the rollover. Everyone knows it will fall, so they naturally rush to short. Shorts accumulate, the funding rate turns negative, and shorts start paying longs.

From an arbitrage-free principle perspective, this is normal. The spread between the front and back month gives short sellers a profit. The funding rate will reduce this profit. The larger the spread, the higher the negative funding rate the market charges.

Once the negative funding rate reaches a certain level, this seemingly obvious arbitrage opportunity will be eroded. The cost for short sellers will completely cover the profit.

Strategies

How to make money in such a market context? Here are three common strategies.

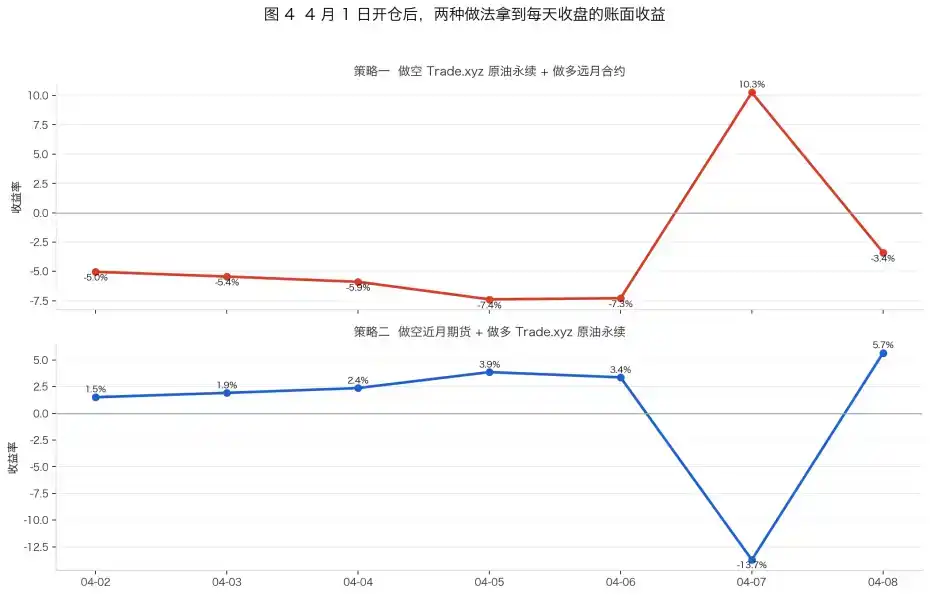

1. Short the crude oil contract on Tradexyz at the current price, while simultaneously going long the back-month contract on CME.

This seems like a risk-neutral strategy to stably earn the spread, but it fails to consider several factors.

Suppose you short Trade.xyz's WTI contract at $95.352 on April 8th, while going long the June futures contract at $87.75, each with a notional principal of $10,000. If both sides eventually converge, you could theoretically get a spread of $7.60, about $797 in profit. But on April 8th, the daily funding rate for the short position was already 1.42%. Based on the remaining 6 days until rollover completion, the funding fee would cost $851. At this point, the net profit is only -$53. This doesn't even include transaction fees and slippage.

Abraxas capital implemented this strategy starting on March 19th, after the last rollover was completed. Their Brent crude oil position on tradexyz accounted for 20% of the open interest in that market and yielded huge profits early on when the funding rate remained relatively neutral. However, as more arbitrageurs flooded in, the funding fee has devoured 80% of their arbitrage profits.

The massive position also means they find it difficult to exit and are forced to pay passively.

2. Short the back-month futures contract, go long the xyz front-month contract, and close the position before the rollover begins.

This trade is almost the counterparty to Strategy 1, betting that the market is over-arbitraged. After April 1st, this strategy could indeed yield profits.

3. Short the funding rate for the xyz contract on Boros before the rollover begins.

Boros is a market developed by the Pendle team specifically for trading rates (funding rates). In Boros's crude oil contract market, what is traded is the market's expectation of the funding rate for Trade.xyz's crude oil contract over the coming period. If users believe the negative funding rate will deepen further, they can short the market's funding rate contract.

However, limited by slippage costs, position limits, transaction fees, and extremely low capital efficiency (only supporting 0.2x leverage), this trade also struggles to achieve the ideal high returns.

Conclusion

The rise of RWA trading platforms like Trade.xyz is forcing a group of "crypto traders" to become "futures traders." DeFi players are also starting to learn the CME rollover calendar, calculate front-back month spreads, and make decisions based on the funding rate curve on Boros.

Trading platforms are continuously iterating, and market participants are also adapting to new infrastructure.