Author: Yan Wai Zhi Yi, Wall Street Insights

In the past, silver was called "poor man's gold" not because it was truly cheap, but because the market never took its scarcity seriously.

Ample supply, adjustable inventories, and dispersed uses—for a long time, the market firmly believed that no matter how demand fluctuated, silver could always be quickly replenished. Because of this, it could be repeatedly traded as a shadow of gold but was almost never seriously allocated.

But this premise has been shattered by reality.

Since 2021, the global silver market has experienced a physical supply-demand deficit for several consecutive years. Unlike the short-term tightness amplified by previous financial cycles, this deficit stems directly from the industrial side: demand for silver in key sectors such as photovoltaics, electrification, and high-end electronics is expanding rapidly and simultaneously, while supply can hardly keep pace.

More critically, silver's supply system is highly unresponsive to price signals.

Over 70% of global silver production comes as a by-product of other metals, with production rhythms determined by the investment cycles of copper, lead, and zinc, not by the price of silver itself. This means that even if prices rise, supply cannot quickly increase; when buffer inventories are continuously depleted, the market faces not temporary fluctuations but sustained constraints.

It is at this moment that silver truly begins to break free from the "poor man's gold" narrative. It is no longer just a cheap alternative when gold rises but is becoming a material that is continuously consumed by key industries and is difficult to replace.

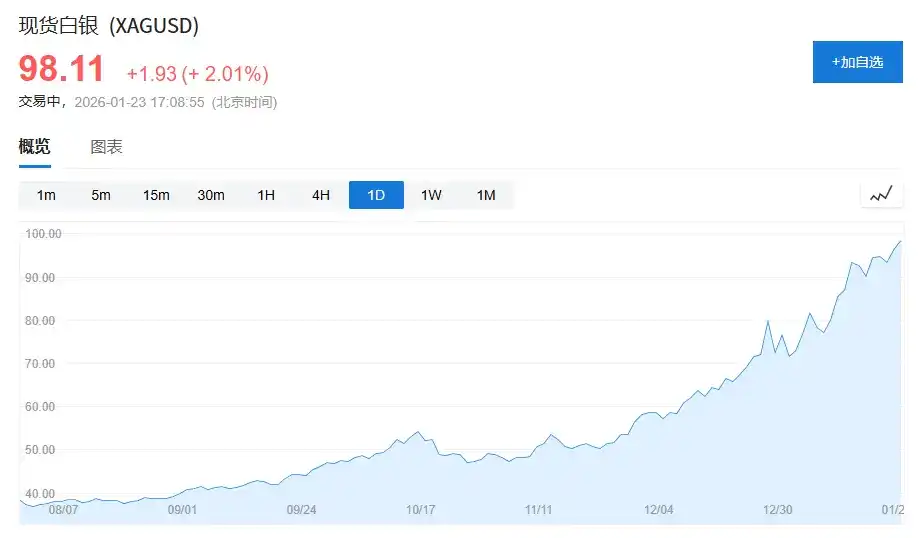

(Silver prices approach $100 per ounce. In mid-October last year, silver was only $50/ounce, nearly doubling in 3 months.)

1. Silver's "Identity Dilemma": Stuck Between Gold and Industrial Metals

To understand why silver has long been undervalued, one must first understand its "identity dilemma."

In the modern commodity system, assets can be broadly divided into two categories:

One is credit-based assets, typically represented by gold. Gold's value anchor does not come from industrial use but from the credit system and reserve demand. Even in the weakest years of demand, global central banks' net gold purchases still account for 15%–25% of total demand, providing a stable foundation for its price.

The other is growth assets, such as copper, crude oil, and iron ore. These metals have almost no financial attributes; their prices are mainly driven by economic cycles, infrastructure, and manufacturing investment.

Silver, however, is stuck between these two.

According to the "World Silver Survey 2025," global silver demand in 2024 was 1.164 billion ounces (approx. 36,200 tons), of which:

Industrial demand was 681 million ounces, accounting for about 58%;

Jewelry and silverware demand was 263 million ounces, accounting for about 23%;

Investment demand (bars, coins, ETFs) was about 191 million ounces, accounting for about 16%.

The problem is that these three types of demand have completely different behavioral patterns:

Industrial demand relies on the industry cycle, jewelry demand is highly price-sensitive, and investment demand is highly susceptible to macro sentiment.

This structural split has long left silver without a stable, single, dominant pricing anchor.

The result is reflected in the price: silver has long been forced to price itself relative to gold.

A clear indicator is the gold-silver ratio. Over the past half-century, the historical average of this ratio has been roughly 55–60; but between 2018–2020, it once exceeded 90, and at the peak of the pandemic shock, it even approached 120.

Even against the backdrop of silver's industrial demand hitting a record high in 2024, the gold-silver ratio has long remained in the 80–90 range, significantly higher than the long-term average.

This is not because silver is "useless," but because the market is still pricing silver using gold's financial logic.

2. Silver's Repositioning: From "Dispersed Use" to "Locked In by Industry"

The real change did not start in the financial markets but occurred quietly on the industrial side.

To summarize the current change in one sentence: Silver is shifting from an industrial metal with dispersed uses to a functional material locked in by key industries.

1. Photovoltaics: Silver Becomes "Indispensable" for the First Time

Photovoltaics are the most critical factor in the change of silver's demand structure.

In 2015, global new PV installations were about 50GW; by 2024, this number exceeded 400GW, an increase of over 8 times in less than a decade.

The industry is indeed continuously "de-silvering." Silver usage per watt has dropped from about 0.3 grams in the early days to around 0.1 grams with current mainstream technology.

But the expansion speed of installation scale is far faster than the decline in unit usage.

According to the "World Silver Survey 2025," the actual demand for silver from the PV industry in 2024 reached 198 million ounces, an increase of over 160% compared to 2019, accounting for about 17% of global silver demand.

More critically, silver's position in photovoltaics is not "easily replaceable." In terms of key indicators such as conductive efficiency, long-term stability, and reliability, silver remains the optimal choice overall. Technological progress changes the method of use, not the status.

This gives silver, for the first time, a source of demand that is large-scale, fast-growing, and price-inelastic.

2. Electric Vehicles and AI Infrastructure: Usage Not Exaggerated, but Extremely Difficult to Substitute

If photovoltaics bring certainty in demand scale, then electric vehicles and digital infrastructure bring a change in the nature of demand.

A traditional internal combustion engine vehicle uses about 15–20 grams of silver on average; a new energy vehicle typically uses 30–40 grams.

Against the backdrop of limited overall growth in global auto sales, the penetration rate of new energy vehicles has risen from less than 3% in 2019 to nearly 20% in 2024, structurally increasing silver demand.

Meanwhile, the demand for silver from data centers, AI servers, and high-end electronic devices is reflected more in its irreplaceability than in absolute volume.

In 2024, silver demand from electrical and electronic related fields reached 461 million ounces, setting new historical records for many consecutive years.

These application scenarios are relatively price-insensitive but are extremely sensitive to supply stability.

3. The Reality on the Supply Side: Silver Is Not a Metal That "Can Increase Production Just Because Prices Rise"

In stark contrast to the certainty on the demand side is the rigidity on the supply side.

In 2024, global silver mine production was approximately 820 million ounces, with a year-on-year growth rate of less than 1%.

More importantly, over 70% of global silver production comes as a by-product, mainly依附于 (attached to) lead, zinc, copper, and gold mines. This structure has hardly changed substantially over the past two decades.

Primary silver mine production is only about 228 million ounces, accounting for less than 30%, and is still in a long-term downward trend.

This means that silver production is not determined by the silver price but is主导 (led) by the investment cycles of base metals.

4. From Cyclical Shortage to Structural Tightness

Looking back at history, silver has experienced bull markets before, but past rallies were mostly derivatives of financial cycles.

The difference is that since 2021, the silver market has experienced a physical supply-demand deficit for several consecutive years.

According to the "World Silver Survey 2025," the average annual physical deficit in the global silver market from 2021–2024 was about 150–200 million ounces, with a cumulative deficit接近 (approaching) 800 million ounces.

And silver's visible inventories themselves are not ample. Current global流通 (circulating) inventories can only cover about 1–1.5 months of consumption, significantly below the 3-month safety line typically considered for commodities.

Once a large amount of silver enters PV modules, electrical equipment, and infrastructure, it is difficult to return to the流通市场 (circulating market).

5. Silver Is No Longer Just Gold's Shadow

Silver has not suddenly become scarce; it is just the first time it simultaneously satisfies three conditions:

Demand scale is real and sustainedKey uses are difficult to替代 (substitute)

Supply growth is highly constrained

In the past, these three points never appeared simultaneously.

While the market still understands silver as "poor man's gold," the industrial chain has already begun to re-examine it by the standards of a key functional material.

Silver may still be volatile, but it is certain that it is no longer just gold's shadow.

And this is the most important, yet most easily underestimated, underlying change in this round of market activity.