Author: Yaroslav Writtle

Compiled by: Deep Tide TechFlow

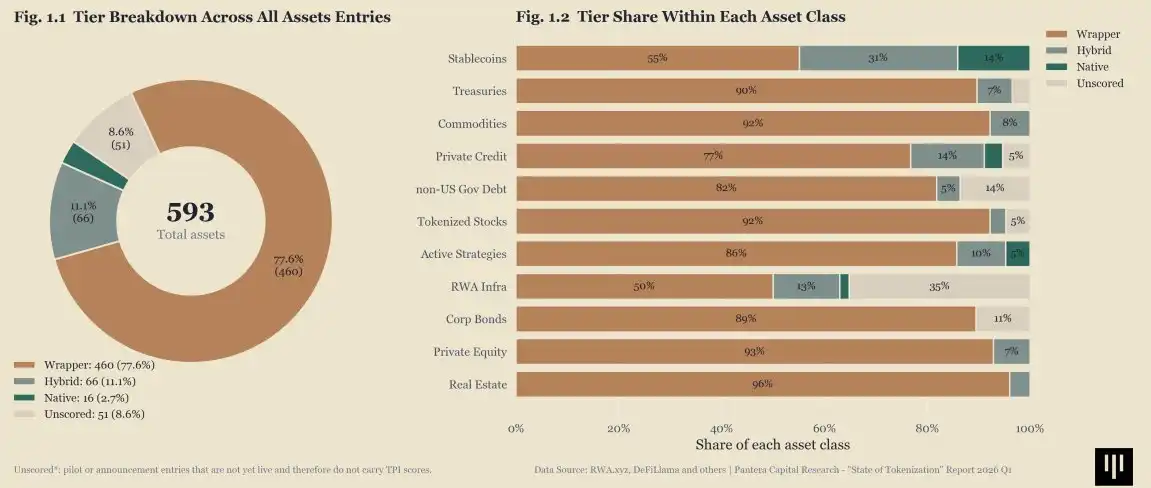

Deep Tide Guide: The RWA sector has been discussed for so long, yet 77.6% of tokenized assets are still just "on-chain wrapping paper" — the token is on-chain, but issuance, redemption, and custody are entirely off-chain. What's truly worth attention are the 11.1% of "hybrid" assets, which are moving part of their lifecycle on-chain. This explains why stablecoins feel far ahead of other RWAs: they are genuine on-chain financial primitives, not just digital shells for traditional processes.

Market Size Growing Faster Than Market Maturity

An effective way to understand this market is not to look at whether it's tokenized or not.

Instead, look at:

- Wrapped

- Hybrid

- Native

A 2026 market survey covering 593 tokenized assets showed that 460 assets, or 77.6%, were still classified as wrapped. Only 66 assets, or 11.1%, were hybrid, and a mere 16 assets, or 2.7%, had reached a native state.

This is the true shape of the market.

Wrapped Remains the Default Form

Most tokenized assets improve distribution, not infrastructure.

The token exists on-chain.

Most of its lifecycle does not.

Issuance, redemption, custody, transfer permissions, pricing, and investor access still heavily rely on off-chain systems.

So surface growth may be real, but on-chain autonomy remains low.

Hybrid Is Where Real Transformation Begins

Hybrid is the part of the market worth watching.

This is where certain parts of the lifecycle begin migrating on-chain:

- Transfer logic

- Settlement processes

- Yield accrual

- Partial compliance or access controls

Not fully native.

But no longer just wrapping paper.

This middle category is still small, which is why the market feels like it's moving faster than it actually is.

Native Is Rare for a Reason

Native assets are rare because the bar is high.

To reach that level, it's not just about the token being on-chain.

The operating model must also be on-chain.

This includes:

- Issuance and redemption

- Transfer execution

- Custody assumptions

- Composability with other systems

Very few assets truly meet this standard today.

Stablecoins Still Feel Ahead of Other Assets

This also helps explain why stablecoins still feel structurally ahead of most RWAs.

They are closer to being true on-chain financial primitives.

Many other tokenized assets still resemble digital wrapping paper for traditional processes, rather than assets that genuinely operate within an on-chain financial system.

What Matters Next

The market doesn't need more proof that assets can be tokenized.

A more useful question now is: which parts of the lifecycle have truly migrated along with it?

This is where the next round of differentiation will occur.

Not between tokenized and non-tokenized.

But between assets that are still distributed on-chain, and assets that are beginning to operate on-chain.