Zcash Open Development Lab, the company formed by the team formerly known as Electric Coin Company, has raised more than $25 million from a roster of heavyweight crypto investors including a16z, Paradigm, Winklevoss Capital, Coinbase Ventures, Cypherpunk Technologies, Maelstrom (family office of Arthur Hayes), Chapter One, David Friedberg, Haseeb Qureshi, Mert, Balaji and others.

What This Means For Zcash

The round lands just months after the ECC team regrouped under a new name, and gives the Zcash-focused builder fresh capital to expand its wallet and protocol work without leaning on the network’s development fund.

Josh Swihart, who now leads ZODL after previously serving as CEO of ECC, framed the raise as a bet on product traction rather than a brand reset. “The name is new, but our team has been building Zcash for a decade,” he wrote. “A couple of years ago, my team and I set out to change the trajectory of Zcash with an uncompromising focus on the user experience for shielded ZEC. We released Zodl (then called Zashi) and have never looked back.”

That pitch is backed by a set of numbers the team clearly wants the market to notice. According to ZODL, its wallet has helped drive adoption of the Zcash shielded pool by more than 400% since launch, while facilitating over $600 million in ZEC swaps since October 2025. Swihart said the company first shipped what he called a “normie-friendly wallet,” then layered in integrations with Flexa for retail spending, Keystone for cold storage and, more recently, NEAR-powered intents for ZEC swaps.

The capital raise is also meant to change how that work gets funded. “This funding allows us to bring these ambitions to life, without relying on Zcash dev fund grants to get there,” Swihart wrote. Alongside Zodl, the company said it is building Zallet, a full-node wallet that will serve as the foundation for new desktop software, with the longer-term goal of creating “a private, decentralized financial system as an alternative to legacy institutions.”

ZODL’s own announcement leaned heavily on continuity. The company said the full ECC team, including the engineers responsible for designing and maintaining some of Zcash’s core systems, moved over earlier this year. It added that protocol development remains central to the company’s work, but argued that future upgrades should stay tied to usability and product-market fit rather than protocol design in isolation.

Zcash founder Zooko Wilcox read the raise as something larger than a routine venture financing. “Twenty-five million dollars is a big investment! For a company that makes a wallet!?” he wrote in a thread reacting to the news. “This set of investors is a signal. They are big, sophisticated, long-standing, and reputable.”

He focused on what the deal does not appear to offer. There is no new token for investors to capture, he noted, and no control over the Zcash protocol itself. “There is no new token that the investors can get a cut of! The ZEC supply is locked in, with a 21M total supply cap, like Bitcoin,” Wilcox wrote. “The investors don’t get control of the protocol! Zcash is permissionless, open-source, and has a huge number and variety of stakeholders.”

From there, Wilcox sketched out a theory of the round: investors may see the wallet business as a monetizable entry point, but just as importantly, some may be underwriting broader ZEC adoption itself. He pointed to public disclosures from Cypherpunk Technologies, which he said already holds more than 1% of ZEC’s eventual supply, and argued that its equity stake in ZODL is smaller than its exposure to the coin.

His conclusion was blunt. “These people are betting that Zcash — not crypto, not privacy, not Bitcoin, not zero-knowledge-proofs — Zcash will be critically important for our civilization,” he wrote.

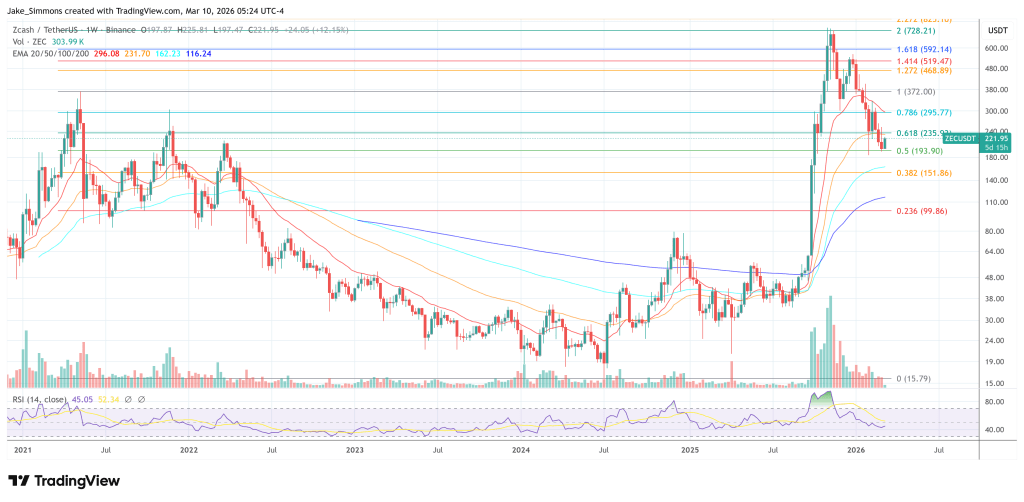

At press time, Zcash traded at $221.95.