TL;DR

The recent decline in optical stocks, ostensibly triggered by a cooling of the CPO narrative, is fundamentally the market repricing a more sensitive question: Is the 2027-2028 volume ramp a period of actual earnings realization, or is it still merely an introduction/validation phase?

CPO (co-packaged optics) itself is not being negated. The bandwidth, power consumption, and switching density pressures within AI data centers continue to increase, and the physical limitations of copper cables and traditional pluggable optical modules haven't disappeared. The issue is that the previous rally in related stocks had priced in an aggressive timeline: after Nvidia pushes CPO into its commercialization window, segments like optical engines, lasers, silicon photonics, and switch chips would rapidly ramp into volume shipments around 2027-2028.

The report from SemiAnalysis on June 9 precisely struck at this pricing assumption. According to public summaries, the report suggests that Nvidia's 800V DC with CPO large-scale production might be delayed until around 2028-2029, with 400V DC still on track to ramp in 2026, and some NPO (near-packaged optics) projects possibly accelerating. Following the market volatility sparked by the report, optical and related supply chain stocks like AAOI, LITE, COHR, GLW, and MRVL saw high single-digit to double-digit pullbacks. The market isn't trading on "whether the CPO direction is valid," but on "how quickly CPO can translate into orders."

But this is not a one-sided bearish view. The "White-Haired Stock God" and AI supply chain analyst Serenity (@aleabitoreddit) subsequently rebutted SemiAnalysis, arguing that it overly relies on conservative engineering models and underestimates Nvidia's ability to compress hardware cycles. Based on her interpretation of signals from Nvidia, Lumentum, Foxconn, and others, she emphasized that CPO remains on track for ramps in the second half of 2026, the second half of 2027, and 2028.

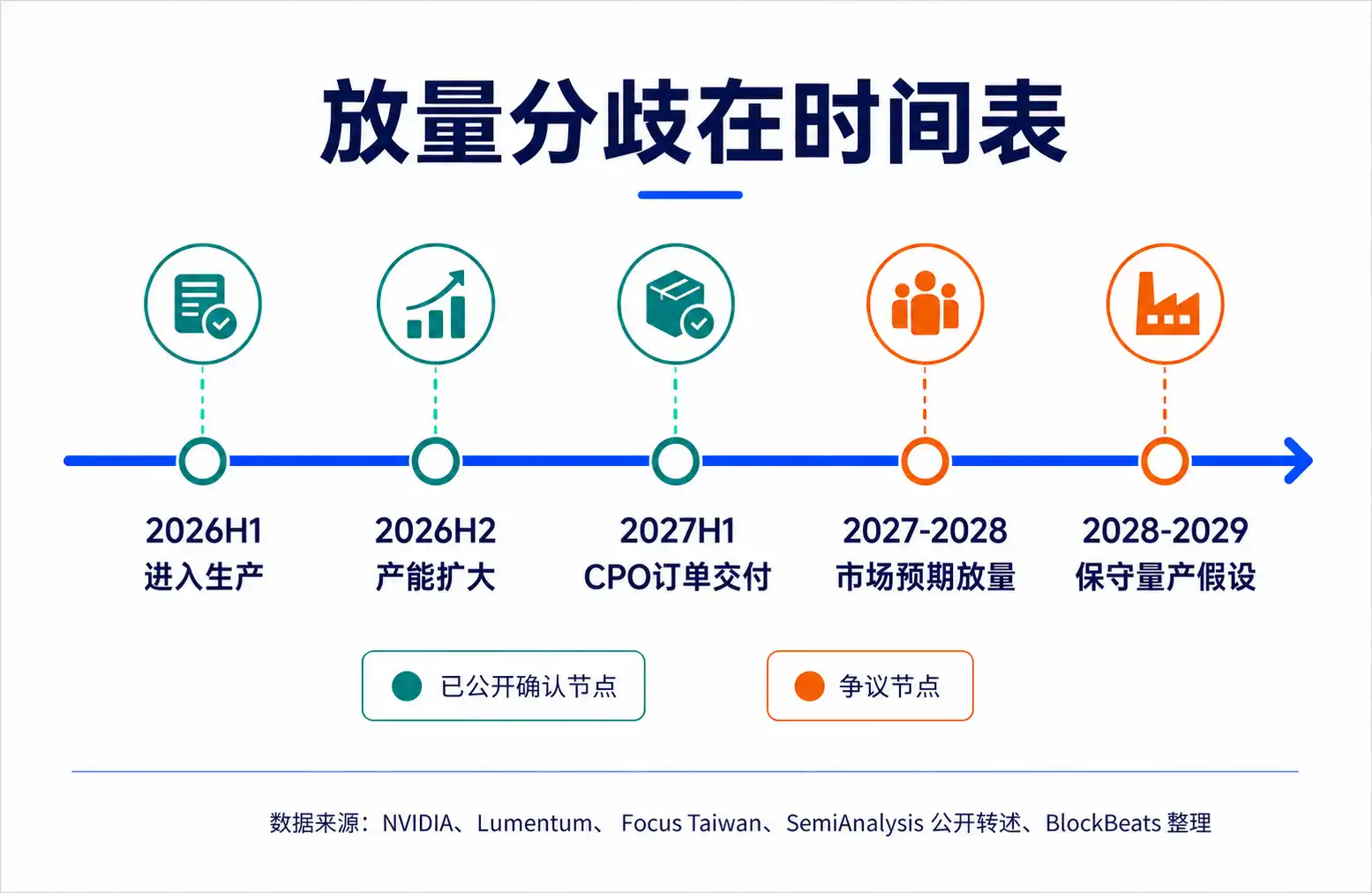

The value of this debate is not in determining who "won," but in shifting the valuation anchor for the optical supply chain from an ultimate-narrative back to a timeline verification: CPO will come, but the slope at which it arrives determines the value distribution between NPO, pluggable modules, light sources, and switch chips.

The Timetable Reassessment Behind the Optical Stock Decline

Over the past few months, the market's buying of the optical chain was based not on current revenue, but on the anticipated capital expenditure migration towards the next-generation network architecture for AI data centers.

As model training and inference clusters expand, communication pressure between GPUs, between racks, and within data centers continues to rise. The network is no longer just a supporting system outside the servers but increasingly a bottleneck for the efficiency of the AI factory. Higher bandwidth density and lower power consumption mean higher expansion limits for a given compute cluster, which is why CPO has been brought to the forefront.

CPO's theoretical appeal is straightforward: placing the optical engine as close as possible to the ASIC (application-specific integrated circuit), shortening the high-speed electrical signal path, and reducing the power consumption, signal loss, and integrity pressures from serializer/deserializer circuits and copper traces. Compared to traditional pluggable modules, CPO offers superior power consumption and density potential in the high-bandwidth era.

The market's problem is its tendency to prematurely trade "the right direction" as "certain volume ramp." Nvidia's official press releases state that the Vera Rubin platform will introduce Spectrum-X Ethernet Photonics, and that CPO switches have entered production for AI factory scale-out and cross-cluster deployment. According to Taiwanese media reports on June 3, Nvidia networking executives indicated that Spectrum-X CPO switches have been shipped to some partners, with capacity expected to expand in the second half of 2026.

These signals are sufficient to prove CPO is advancing, but they cannot be directly equated with risk-free realization of production-scale, large-volume orders. For capital markets, there is a significant valuation difference between "entering production," "shipping to some partners," "customer evaluation," and "mass production." The pullback triggered by the SemiAnalysis report is essentially the market starting to re-differentiate these qualifiers.

The Conservative Model from SemiAnalysis: CPO's Challenge Lies in Systems Engineering

SemiAnalysis is not saying CPO has no future. Its core judgment is more like: CPO's theoretical advantages are clear, but scaling its deployment will be slower than the market imagines.

The reason isn't just one or two components not being ready; it's that CPO concentrates complexity that was originally distributed across modules, boards, and systems into a more deeply coupled system. Higher integration yields more impressive single-point performance, but it also amplifies pressures on manufacturing, testing, maintenance, and supply chain resilience simultaneously.

Traditional pluggable modules benefit from modularity. If a module fails, it can be replaced, and switching between suppliers is relatively easy. CPO is different. The optical engine is placed closer to the ASIC, even integrated into the same packaging system. The power and density benefits come from this close coupling, but the radius of repair also expands. If an optical component fails, it no longer just affects an easily replaceable module but may involve the higher-value switch chip and the entire system.

SemiAnalysis's previous CPO Book repeatedly emphasized serviceability, reliability, yield, and supply chain maturity. Especially in the hyperscale cloud provider scenario, performance is not the only metric. Large customers have high demands for reliability and operational manageability. If production environment failure rates, repair processes, and replacement costs are not under control, even the best power consumption model could see delayed adoption.

InP lasers are another point of contention. Laboratory-level port runtime data can prove technical feasibility but doesn't equate to covering long-term operation, mass manufacturing, field maintenance, and supply chain redundancy in large-scale data centers. For investors, this distinction is crucial: lab validation proves the direction, field reliability determines the volume ramp.

In SemiAnalysis's framework, NPO and pluggable modules are not outdated technologies but more practical intermediate layers before engineering risks are fully resolved. CPO is theoretically superior, but if its comprehensive adoption requires more time, the market must reprice these "less-than-ultimate but easier-to-manufacture-and-maintain" solutions.

Serenity's Rebuttal: Nvidia Could Compress Hardware Cycles

Serenity's rebuttal does not deny CPO's engineering difficulties but argues that SemiAnalysis underestimates Nvidia's organizational capabilities within the AI hardware cycle.

Her logic is clear: ordinary hardware adoption can indeed be delayed by yield, reliability, and customer validation, but Nvidia is no ordinary customer. It is both the definer of GPU cluster architectures and the core driver of networking, switching, system integration, and supply chain cadence. When the expansion of AI factories is constrained by network power and bandwidth limits, Nvidia has a strong enough economic incentive and industry chain leverage to compress traditional adoption cycles.

Serenity's cited evidence comes in two layers. The first is publicly cross-verifiable company statements, including Nvidia's official information about Spectrum-X Photonics entering production, and Lumentum's Q2 FY26 comments regarding CPO order and delivery schedules. Lumentum mentioned receiving incremental CPO orders worth hundreds of millions of dollars for delivery in the first half of 2027, and company materials also noted CPO-related business is expected to begin a broader ramp in the second half of 2026.

The second layer is her interpretation of supply chain signals, such as Foxconn shipping optical switches to Nvidia early. However, the specific scale of these signals and whether they represent test samples or production-level orders still require more public information for confirmation.

This is also the core of the divergence between Serenity and SemiAnalysis: SemiAnalysis believes systems engineering variables will naturally lengthen the cycle, while Serenity believes Nvidia's supply chain execution capabilities will steepen this curve.

These two judgments are not entirely contradictory. Nvidia could bring CPO into production and customer validation earlier, possibly driving adoption in some scale-out scenarios first, but this doesn't automatically mean all AI data center networks will rapidly switch to CPO by 2027. Scale-out, single-rack scaling, intra-rack, inter-rack scenarios, and different customers' reliability tolerances and cost models vary, potentially leading to layered adoption rhythms.

Serenity is rebutting the overly conservative conclusion that "CPO will be significantly delayed," not proving "CPO is already comprehensively risk-free." For the market, this is enough to support a bounce-back logic from an oversold position, but not enough to directly rewrite the aggressive 2027-2028 revenue curve back into certainty.

Why NPO Suddenly Became Important

NPO became important in this debate because it sits precisely between the logics of SemiAnalysis and Serenity.

It is not the opposite of CPO, nor a simple continuation of traditional pluggable modules. The basic idea of NPO is to place the optical engine on a pluggable socket substrate near the ASIC, shortening the electrical path to gain some power and density benefits while retaining better testability, replaceability, and supply chain elasticity.

If SemiAnalysis's conservative model proves closer to reality, and CPO's deep packaging is slowed by yield, repair, and reliability issues, NPO would become the more realistic choice for a longer period. It allows hyperscalers to gradually accumulate optical interconnect operational experience without taking on the full CPO risk too soon, and also leaves a longer window for existing optical module and engine suppliers.

If Serenity's judgment about Nvidia's execution is more accurate, NPO may not disappear either. A more likely scenario is the parallel existence of NPO, CPO, pluggable modules, and copper interconnects across different network layers. Nvidia's own roadmap indicates that scale-out CPO can proceed first, while some single-rack scaling scenarios may still rely on copper or hybrid architectures into 2027-2028.

The implication for investors is that they cannot price the optical chain solely with a "CPO wins, everything else loses" mentality. Different technology paths benefit different segments: CPO favors highly integrated optical engines, laser light sources, silicon photonics, and the switch chip ecosystem. A prolonged window for NPO and pluggables could mean continued order and margin support for existing optical module makers, connectors, materials, and some light source suppliers.

The market's previous mistake was prematurely translating a technological endpoint into the earnings trajectory of a single path. What has now reopened is the valuation space for the intermediate paths.

Production-Level Data Is the Next Verification Point

This debate will not be resolved by one report or a series of posts in the short term. SemiAnalysis reminds the market that CPO's difficulty lies in systems engineering. Serenity reminds the market that Nvidia's supply chain organizational capabilities could alter traditional hardware adoption rhythms. The true divergence between the two will need to be verified by production-level data from the second half of 2026 through 2028.

The most critical factor going forward is not "whether shipments are happening," but the qualification of those shipments. Delivery to some partners, customer evaluation, initial production, volume ramp, and large-scale deployment are completely different phases. Future statements from Nvidia regarding Spectrum-X / Quantum-X Photonics production scale, and comments from optical suppliers like Lumentum and Coherent on orders, capacity, and margins in their earnings reports will be more important than the wording of a single conference.

Equally important to watch will be field reliability and maintenance data. If CPO's failure rates, replacement procedures, yield curves, and total cost of ownership in production environments prove sufficiently stable, SemiAnalysis's conservative model will be adjusted. If this data remains confined to labs or small-batch validation, the window for NPO and pluggable modules will continue to be priced higher by the market.

The optical chain is now trading not on CPO's life or death, but on the slope of the timetable. The next verification point will lie in whether "entering production" translates into sustainable volume ramp, and the speed at which this ramp is ultimately reflected in orders, margins, and customer deployment qualifiers.

Although SemiAnalysis expressed concerns about the CPO technology over the next couple of years, they still identified five semiconductor sub-sectors they are optimistic about, namely:

Copper / AEC / ACC;

Pluggable Optics / DSP;

CPO Test Equipment;

Power Gray Space / UPS Continuation;

Board-Level VRM / Silicon-Based Power / Passive Components.

The specific related stock tickers are included in the image below for readers' reference.