By Su Yang

Edited by Xu Qingyang

Bloomberg, citing informed sources, revealed that AI startup Anthropic is in early-stage talks with investors, aiming to raise at least $30 billion in new funding at a valuation exceeding $900 billion.

Informed sources disclosed that this round of financing is expected to be completed as early as the end of May 2026, although the deal is not yet finalized, and no term sheet has been signed.

If the financing succeeds, Anthropic will not only surpass OpenAI (valued at $852 billion in March) but also challenge the market capitalizations of tech giants like Apple and Microsoft. It is noteworthy that early investors who backed the company have largely chosen to sit on the sidelines for this round.

Anthropic CEO Dario Amodei. This image was generated by AI.

01 $30 Billion in Annual Revenue and 40% Gross Margin

Why can a company's valuation skyrocket 15-fold in 14 months? The answer seems obvious: growth rate.

According to publicly reported data, Anthropic's annualized revenue surged from $1 billion in December 2024 to $30 billion by the end of March 2026. This means that over consecutive years, it has maintained a growth rate exceeding 10x.

This growth curve may be unprecedented in enterprise software history.

Eight of the top ten companies on the Fortune Global 500 list are already Anthropic's clients. Over 1,000 enterprise accounts spend more than $1 million annually on Claude. In particular, its developer-facing coding product, Claude Code, launched in May 2025, reached an annualized revenue of $2.5 billion by February 2026, with enterprise subscriptions quadrupling within the first six weeks of the year.

Calculated with a $900 billion valuation and $30 billion in annualized revenue, the price-to-sales ratio is approximately 30x. This multiple sounds extreme, but supporters' calculations bet on the future. They believe a company growing 10x annually cannot be valued conventionally. Its pricing logic assumes it can maintain a similar compound growth rate until 2028, making the current valuation reasonable in hindsight.

Regarding Anthropic's revenue, competitor OpenAI has raised its own doubts, suggesting that the $30 billion annualized revenue reported by Anthropic uses gross revenue accounting. That is, when customers use its models through platforms like Amazon Web Services or Google Cloud, it records the total end consumption as revenue and then lists the fees paid to the cloud platforms as expenses.

OpenAI estimates that after deducting these intermediary fees, Anthropic's true annual revenue is closer to $22 billion. This $8 billion gap is purely a methodological choice, but it will become a focal point for market and regulatory scrutiny during an IPO.

More noteworthy than revenue accounting are the costs.

Documents show that Anthropic plans to spend approximately $19 billion in 2026 on training and inference computing, a figure almost equivalent to its annual revenue. More critically, due to inference costs exceeding expectations by 23%, its business gross margin has been compressed to about 40%, a level far below that of most mature enterprise software companies.

Anthropic is not yet profitable and is expected to break even only by 2028. For a company nearing a trillion-dollar valuation, this combination of financial metrics is indeed unusual.

02 Valuation-Driven Computing Arms Race

Why does Anthropic need to raise so much money?

Nominally, it's for development and expansion, but in essence, this $30 billion financing is primarily to pay for the computing infrastructure it has already committed to but has not yet built. This appears to be a model completely different from traditional tech finance.

In the past, startups raised funds to refine products, expand markets, and then gradually match valuations with growth. But in the AI era, startups need to first raise funds at an extremely high valuation, use that money to lock in massive future computing power, and then hope this computing power drives a leap in model capabilities, leading to revenue growth that ultimately justifies the high valuation.

It's like the chicken-and-egg debate.

Now, valuations drive computing commitments, and these commitments require the next, even higher valuation to fund them. This cycle is constantly accelerating. Anthropic is the ultimate embodiment of this model.

Once this cycle starts, it's hard to stop. It can propel a company to the clouds or plunge it into an abyss in an instant.

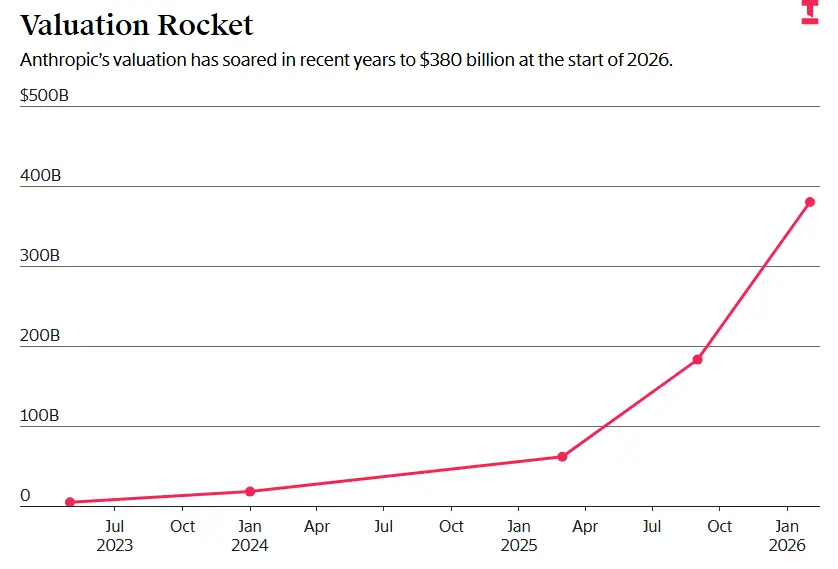

Anthropic's valuation surged to $380 billion in early 2026.

Shortly after the company completed its last $30 billion funding round, Anthropic CEO Dario Amodei told Fortune magazine that if AI progress were delayed by 12 months, Anthropic would go bankrupt.

For a company valued at $900 billion, the distance between "extraordinary success" and "operational bankruptcy" might be just a few bad quarters.

This precarious balance may be why sensitive early investors have largely refrained from participating in this round.

03 Early Investors Collectively Wait-and-See

According to Forbes, some of Anthropic's early backers—those who invested at a $4.1 billion valuation in 2023 or a $61.5 billion valuation in March 2025—have almost no willingness to participate in this round.

The reason is simple. Bankers privately estimate that if Anthropic goes public as early as October 2026, its public market valuation might land between $400 billion and $500 billion. This means that if someone invests at a $900 billion valuation in the final private round, theoretically, before the shares even unlock and become tradable, that investment would already be underwater on paper.

Such an inversion, where late-stage private valuations are significantly higher than expected IPO valuations, is extremely rare in the history of tech financing.

It's a signal, indicating either that this company is severely overvalued in the private market, or that the public market will offer a completely different pricing. Either possibility is fraught with uncertainty.

And that decisive event on the horizon is the IPO itself.

We previously mentioned the key figure behind Anthropic's IPO and financing—the company's financial helmsman, Krishna Rao.

The Information reported that at the time, Anthropic's computing lifeline was essentially tied to Google alone. Rao felt this was untenable—you can't put all your eggs in one basket. He championed a new strategy internally and among investors: computing suppliers must be diversified.

According to The Information citing informed sources, Rao discussed this strategy in depth with investor Byron Deeter of Bessemer Venture Partners. Deeter later commented that it was Rao who made the company realize that having multiple partners would allow for faster development.

Looking back now, Anthropic moved faster than OpenAI. They have already signed deep agreements with all three cloud computing giants: Amazon, Google, and Microsoft. At the chip level, they have also incorporated NVIDIA GPUs, Google's self-developed TPUs, and Amazon's chips, forming a diversified supply network.

But signing agreements is not enough; the core is ensuring suppliers actually deliver the computing resources. In late 2025, Rao spearheaded two major deals: one committing $30 billion to use Microsoft's cloud servers running NVIDIA chips, and another securing up to 1 million Google TPUs.

By early April 2026, Anthropic went further, signing new agreements with Broadcom and Google, locking in several gigawatts of data center power supply capacity. These moves are no longer simply "buying" computing power but are large-scale "reservations" of future infrastructure.

Since joining, Rao has helped the company complete multiple funding rounds totaling $60 billion. By January of this year, the company's valuation had risen to $380 billion.

It can be said that under Rao's forceful drive, Anthropic's computing infrastructure and financial firepower have reached unprecedented scale.

04 Is There a Bubble? The Answer in Six Months

Following the current pace, if this round of financing proceeds as intended, Anthropic is expected to seek an IPO between October 2026 and the first half of 2027. Goldman Sachs, JPMorgan Chase, and Morgan Stanley are reportedly in discussions about the matter.

At that time, the market's core focus will no longer be "Can Anthropic sustain growth?" but will turn into a public referendum on the entire AI industry's valuation logic over the past three years: Was the private market's pricing of AI correct?

Ultra-large-scale corporate capital expenditure commitments, multi-year computing reservation contracts, 40% gross margins, the debate between gross and net revenue accounting, and that accelerating "valuation-computing-revaluation" cycle—all these complex issues that could be ambiguously handled in the private market will, at the IPO, be placed under the public market's microscope.

If the public market is willing to give Anthropic a valuation of $1 trillion or even higher, then the entry price at a $900 billion valuation might look like a generous early bet. But if the market only offers $500 billion, the situation for the last batch of private investors would be very awkward.

A third possibility, perhaps with more profound implications, is that Anthropic's IPO will serve as a key data point to validate or disprove the entire AI finance structural hypothesis.

Remember Michael Burry, the inspiration behind *The Big Short*, who recently warned about "tech stocks" and "chip stocks" bubbles in his paid newsletter again. Once the AI finance hypothesis is disproven during Anthropic's listing, it could be the moment the bubble bursts.

So, whether for Anthropic itself or for the entire AI industry accustomed to soaring valuations over the past three years, the stress test has just begun, and will soon be given the most real, most ruthless pricing by a stock trend curve.

Special contributor Jin Lu also contributed to this article.