Author: Sam Schneider

Compiled by: TechFlow Deep Tide

Deep Tide Guide: Prediction markets are becoming the new gambling infrastructure. Author Sam Schneider pulled all 203 million historical trades from Kalshi's public API and found that over 82% of contract volume comes from sports betting, with cumulative platform fee revenue reaching $545.6 million. This article deconstructs the business logic of this $11 billion valuation company, from its order book mechanism and fee structure to regulatory gray areas.

Full text as follows:

Suppose we go back to 2005, and you start a company called Meth Labs, Inc. You get customers, secure venture capital, and in the blink of an eye, you're listed on the New York Stock Exchange with the ticker $METH. People can buy your stock, sell your stock, or set up an iron condor strategy. The NYSE provides a centralized market where buyers and sellers transact at prices based on continuously released information.

The above refers to the NYSE, but there are many stock exchanges (NASDAQ, LSE, SSE, etc.), all facilitating the buying and selling of securities. In fact, markets are so crucial to society that even if you're not an avid day trader, you constantly interact with them. Uber connects drunk people with drivers, Facebook Marketplace connects people with second-hand furniture, and your dad is trying to connect you with a job.

Suppose you want to retire and sell your $METH stock to do charity. Who would buy it? For how much?

Markets do two things:

- Markets determine the price people are willing to buy and sell at (price discovery).

- Markets provide a trading platform because your next-door neighbor probably doesn't want to buy your $METH (liquidity).

But what if the market revealed not a price per share, but the probability of a specific event occurring? This is a prediction market.

Whether it's keeping track in an underground cockfighting ring with pen and paper or through centralized, large-scale, well-capitalized companies like Kalshi and Polymarket, prediction markets are fundamentally different from stock trading:

- It's binary. The event either happens or it doesn't.

- The contract settles when the specific event occurs, the outcome is determined, or the time expires.

You can't buy $METH stock through a prediction market, but you can bet that $METH's stock price will be between $122 and $124 on January 6th.

Today, we're going to sell a gun at Bass Pro Shops. Oops, sorry, Claude is hallucinating again. Today we're looking at: how billions of dollars are flowing into these markets, how FTX's legacy continues, what proportion is sports betting, and how much money Kalshi has actually made. Let's learn a new way to gamble.

History & Introduction

Kalshi and Polymarket launched in 2018 and 2020, respectively. While these two form the current duopoly, the history of prediction markets is longer. One of the originals is the Iowa Electronic Markets (IEM), which has been operating prediction markets since 1988.

Betting on one's "beliefs" can get people into trouble, but the wisdom of crowds remains a valuable predictive tool. Look at the 2004 paper by Wolfer and Zitzewitz:

"These markets predicted the vote shares of Democratic and Republican candidates with an average absolute error of about 1.5 percentage points... The final Gallup poll had a prediction error of 2.1 percentage points."

However... for all these years, one thing was missing... preventing us from collecting predictions, building markets, scaling to millions, and profiting from it. That missing piece was—capital-rich crypto web applications that give you free groceries and let you bet on whether the next Pope is transgender. Just as Hayek envisioned when he wrote "The Use of Knowledge in Society".

We'll focus on Kalshi next, but there are other projects and protocols in this space.

How Does This All Work?

Prediction markets expand the surface area of human gambling. For example, I might bet $10 that I can drink 10 beers before midnight, and my wife's boyfriend might not believe me. I say "yes," he says "no." Replace me with LeBron James, beer with points, midnight with the end of the game, and you have a real market tradable on Kalshi.

In Kalshi's system, a market refers to a binary market that ultimately resolves to "Yes" or "No." An event is a group of such markets, and a series groups similar but independent events together. For example:

- Miami's maximum temperature is a series.

- Each day in this series is an event.

- Each event contains multiple markets: [68° to 69°] or [69° to 70°].

Each market has a "Yes" and a "No," each with its own order book. What is an order book? Let's get some terminology straight first...

Caption: Diagram of core Kalshi trading terminology

Every trade on Kalshi is a match between a Maker and a Taker. Just like in our "purely fictional, absolutely did not happen" scenario, Makers and Takers on Kalshi are betting against another person, not against the platform. You're not buying a stock; you're buying a contract—it settles to $1 if correct, $0 if wrong.

As price-sensitive rational actors, I'm willing to bet $10 to win $20, and so is my wife's boyfriend. Both sides put up money, the implied probability for this event is 50% (10/20). In "event contract" terms:

- We break this into 20 contracts of $1 each

- Each contract locks $0.50 from each side

- At settlement, the winner takes the other's $0.50

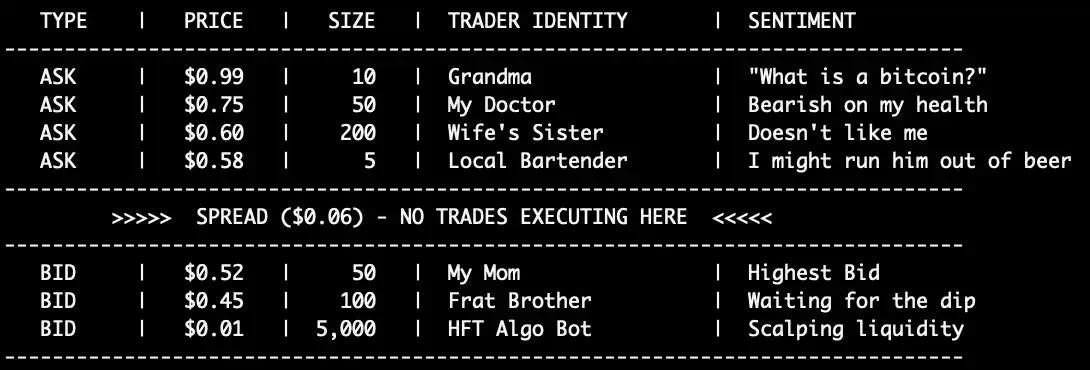

When trading volume scales up, tracking it with an order book becomes necessary.

Caption: Order book schematic showing buy and sell orders

Order books can be displayed in many ways. They typically show the order, whether it's a buy or sell, the quantity, and the time the order was placed.

Bids include everyone who wants to buy, asks include everyone who wants to sell. In the figure above, buy and sell orders are listed from best to worst price. The difference between the highest bid and the lowest ask is called the spread.

In liquid markets (like the Super Bowl), the spread might be just 1 cent. In illiquid markets, the spread can be wide because no one wants to take the other side. This is why Kalshi provides incentives for liquidity providers and market makers.

Back to the order book. When a Market Taker thinks $0.52 is a steal, they match with my mom for 50 contracts (you can see her on the buy side). The asset price "moves" to $0.52, and that buy order disappears from the book. This is price discovery, or more accurately, the market is pricing probability. The degens have updated my probability of liver failure to 52%. Let's see what a real Kalshi order book looks like:

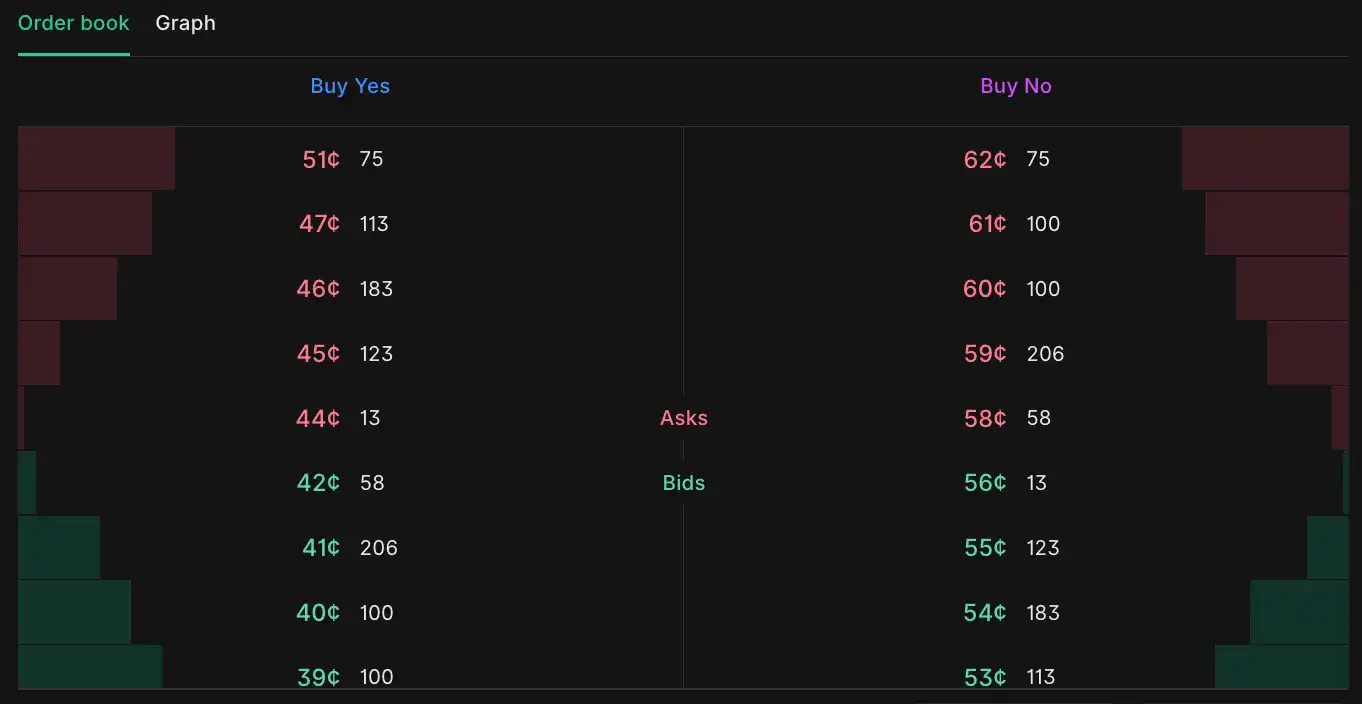

Caption: Real Kalshi order book interface, left side "Yes," right side "No"

You'll notice the order book has "Yes" and "No" sides. Contracts on Kalshi can resolve to "Yes" or "No," and traders trade both sides.

- On the "Yes" side, the lowest ask is $0.44 for 13 contracts, $0.42 can buy 58 contracts, spread $0.02.

- On the "No" side, the lowest ask is $0.58 for 58 contracts, $0.56 can buy 13 contracts, spread $0.02.

Wait... this doesn't look right. Why are the two sides perfect mirrors? Why is the quantity of "Yes" bids the same as "No" asks, and $0.42 + $0.58 equals exactly $1? Because buying "Yes" is equivalent to selling "No".

Got the orders figured out, how does matching work?

Kalshi uses a price-time priority matching algorithm on its Central Limit Order Book (CLOB). It sounds intuitive on the surface—sort by price, then by time for same price. But building an exchange and processing these orders at scale is far from simple. For a deep dive into matching engines, I recommend this article from DataBento. On Kalshi's exchange, all orders must be fully collateralized, so no margin trading for now.

For a while, MIAXdx, under MIAX, was Kalshi Exchange's clearinghouse. MIAXdx was originally called LedgerX, but MIAX acquired it through... drumroll please... FTX's bankruptcy proceedings and renamed it! Later, Kalshi decided "I'll build my own clearinghouse," so in August 2024, it registered Kalshi Klear with the Commodity Futures Trading Commission (CFTC) and got approval. Another closed loop—Robinhood recently bought... LedgerX from MIAX!

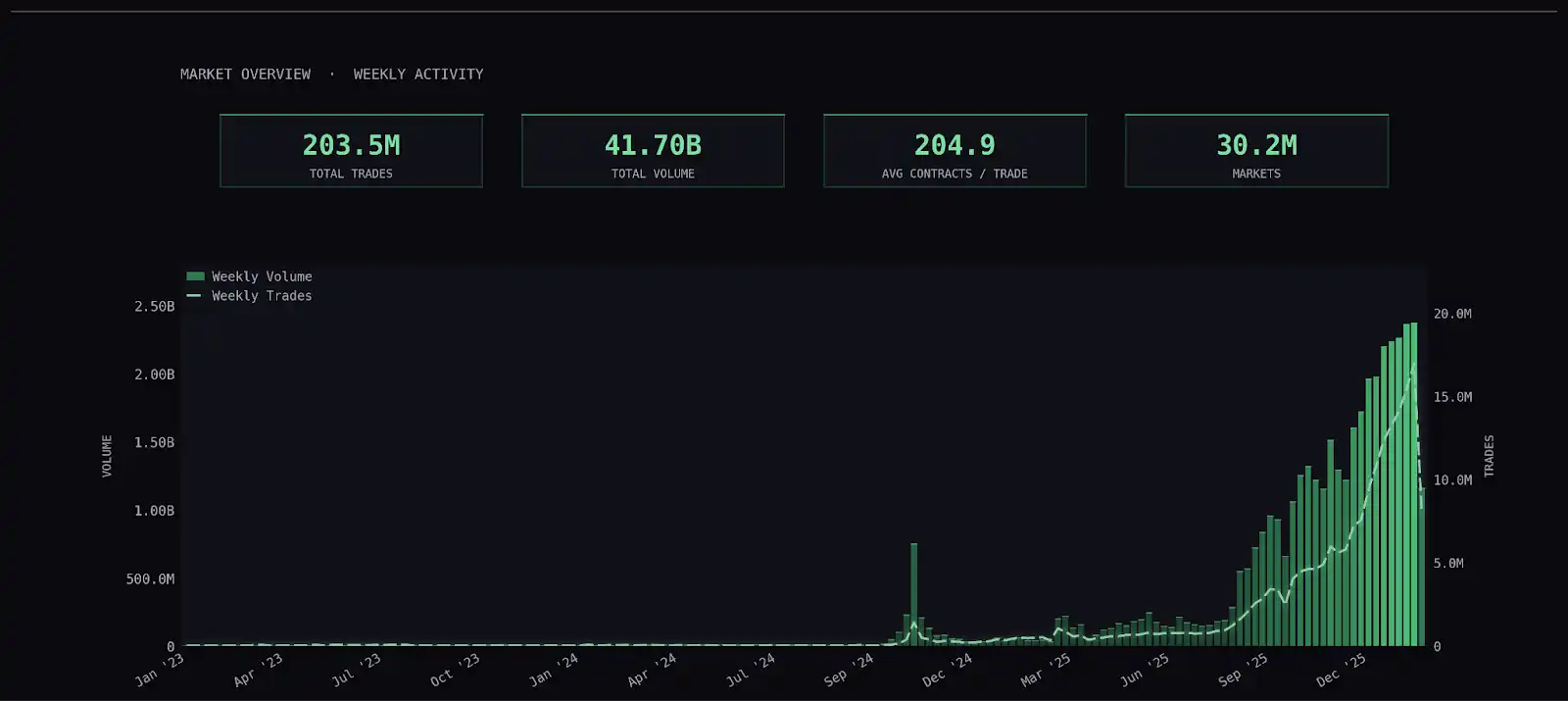

Data

I pulled historical data through Kalshi's Market API and Trading API—about 30 million markets, 203 million trades, total trading volume exceeding $41.7 billion.

Caption: Kalshi trading volume trend chart, total over $41.7 billion

Where does this volume come from? Kalshi's own website and App drive significant traffic. It also partners with some Futures Commission Merchants (FCMs), institutions that facilitate futures trades for clients. You might know them—Robinhood where you transferred your IRA, WeBull where teens trade crypto, and Coinbase where you keep your altcoins.

Ranked by trading volume, first is the 2024 US Presidential Election, over $535 million; second is the 2026 Super Bowl Champion, about $244 million.

Wait a minute... Super Bowl... isn't that just... sports betting?

Isn't This Just Sports Betting?

Kalshi is regulated by the CFTC (Commodity Futures Trading Commission), which oversees US derivatives markets. I say "regulated," but a more accurate term might be "largely unregulated." The Commodity Exchange Act (CEA) establishes the legal framework for the CFTC's operations. This framework gives the CFTC the power to ban onion futures trading, but it also allows 18-year-olds to trade contracts on Kalshi. Kalshi even boasts on its FAQ page that the "Minimum registration and participation age" is 18+ and directly compares itself to... sports betting platforms. Sports betting platforms are subject to state governments, some states completely banning sports gambling, others requiring bettors to be 18 or 21+ (usually 21+).

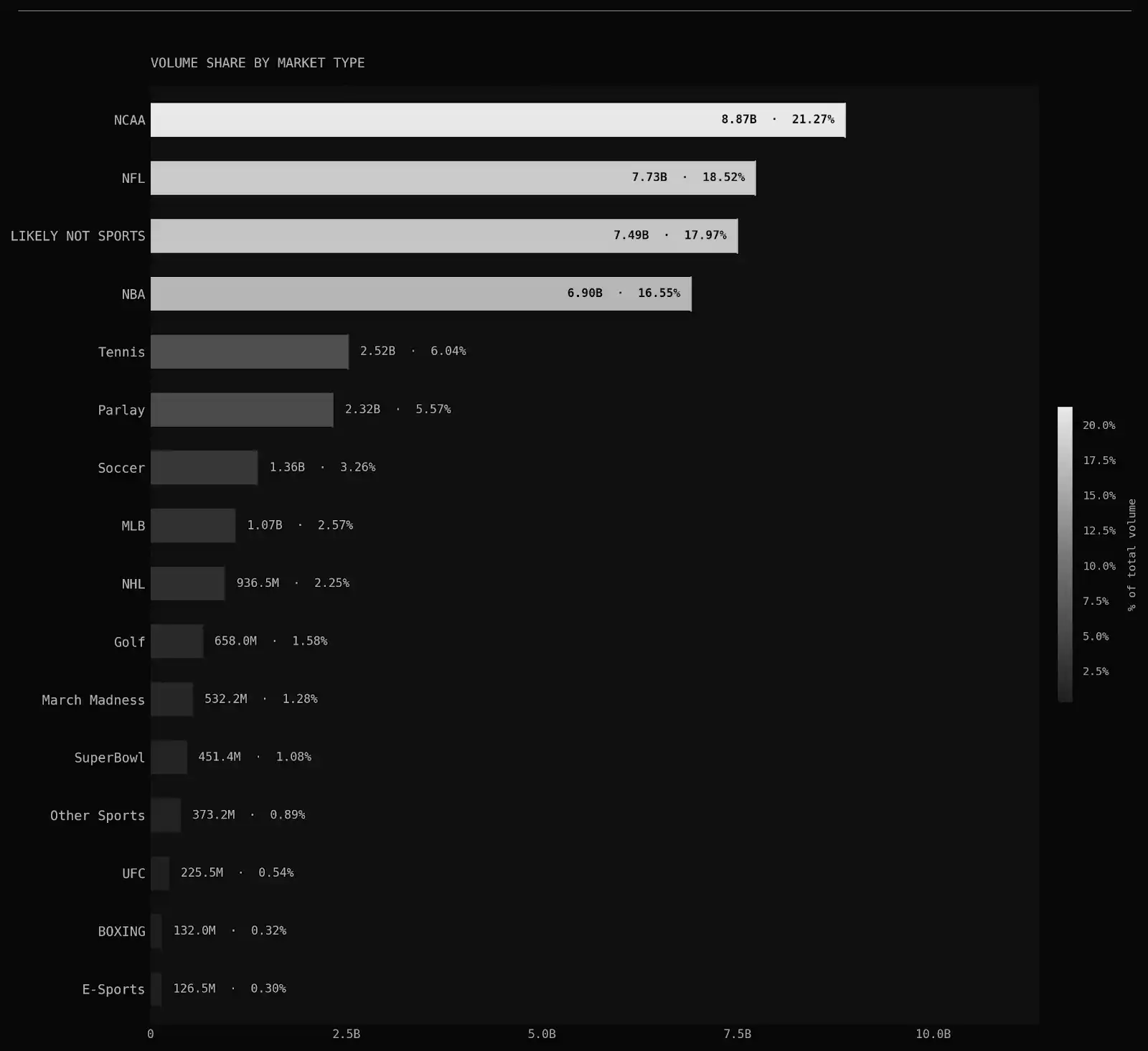

Okay, but... Kalshi is different. You're trading contracts with other people, and you can bet on anything. Not just sports, right? I'm not betting against the house, right?

Caption: Distribution of Kalshi contract volume by category, Sports over 82%

Over 82% of contracts are... Sports. Kalshi is a business that lives on trading volume; the more contracts traded, the more fees it earns. Even better, it's the first platform where 18-year-olds can legally participate in gambling. Oh, and they offer parlays, accounting for over 5% of total trading volume!

As for not betting against the house... quoting Kalshi's article titled "Who am I trading with?":

"Another important participant on the Exchange is Kalshi Trading. Kalshi Trading is an entity separate from Kalshi Exchange... They are a regular participant on the Exchange, just like everyone else."

Smells like a bookmaker, trades like a bookmaker, it probably is a BANG—gunshot, author down.

Back to Data!

The trading volume of these markets follows a power law distribution. Grouping the total volume (USD) by order of magnitude makes this clear.

Caption: Power law distribution of market volume, grouped by order of magnitude

Among markets with $0 volume, 80% are Combos (Parlays). Each combo is a separate market, quoted through Kalshi's RFQ system, and many simply can't find a counterparty.

Using the same volume grouping and splitting by settlement outcome shows: the higher the volume, the higher the percentage of markets that settle to "Yes".

This suggests that for any given market, the base probability should be biased towards settling "No". The volume effect also makes sense—events containing many sub-markets see volume分散 across those sub-markets, with ultimately only one or a few settling "Yes".

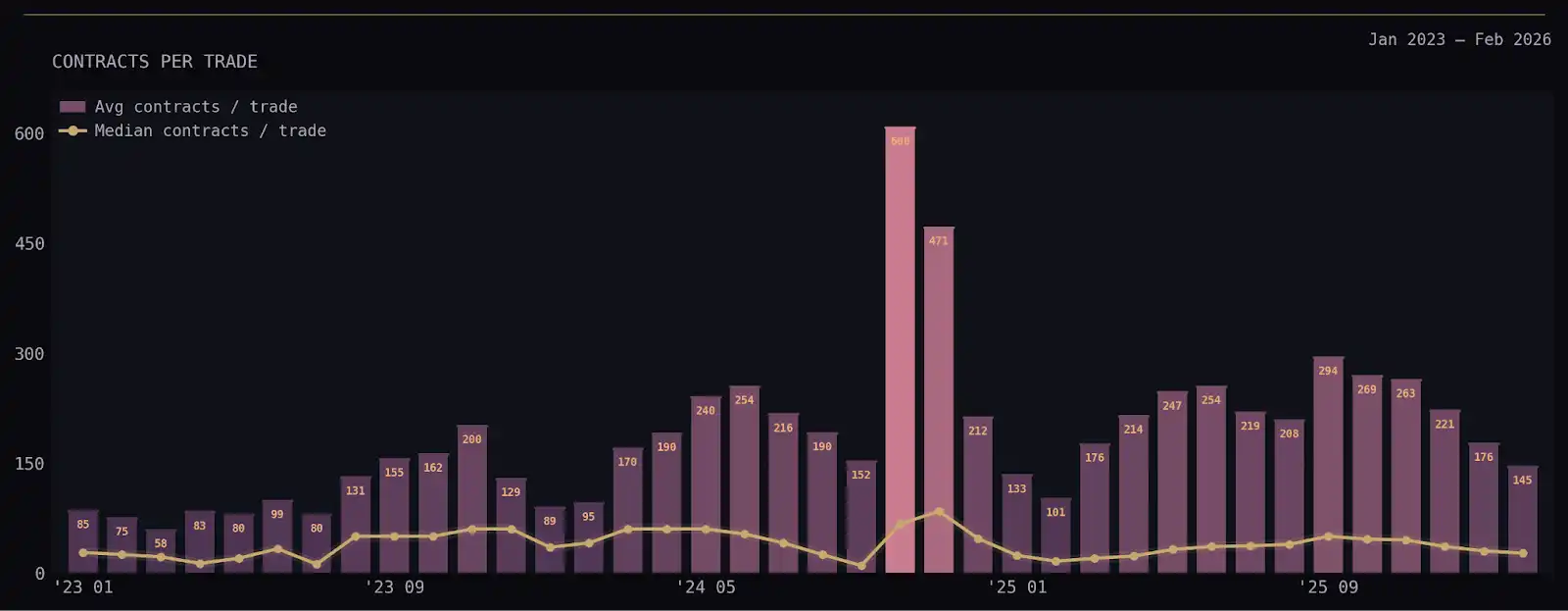

In these markets, the average number of contracts per trade is between 150-250. There was a huge spike in 2024 due to a 1 million contract order placed during the US election. The median is much lower than the average, mostly under 50 per month.

Caption: Average vs. Median contracts per trade

Fee Comparison: Traditional Sportsbook vs Kalshi

If traditional sports betting is like roulette, where the house makes money through odds, then Kalshi is like poker, where the platform makes money through rake, indifferent to who wins or loses.

On traditional sportsbook platforms, you see "even money"—a 50/50 probability bet, like a coin toss for the Super Bowl. The platform doesn't give you true 50/50 odds; it gives both sides a 52.4% probability, higher than the actual probability.

- In a fair market, you bet $10 on a coin toss, win $10 if correct. But on a sportsbook platform, due to the skewed odds, you only win $9.09 if correct.

On a traditional sportsbook platform, two people each bet $10 on heads and tails, one takes home $19.09, one takes $0, the sportsbook takes $0.91, which is 4.5% of the total bet. This 4.5% is the jargon vig, juice, hold, etc.

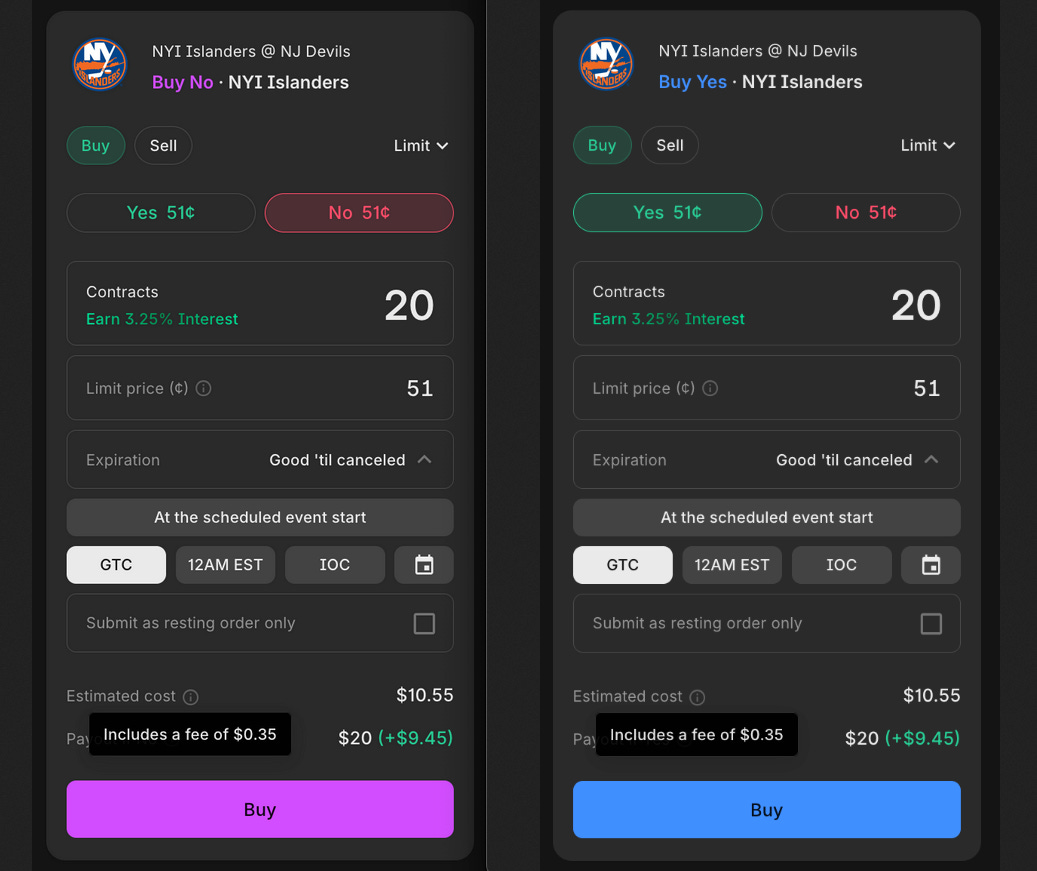

For example, an Islanders vs Devils game, which happens to be 52.4%/52.4% on the sportsbook. On Kalshi, the contract trades at $0.51 (51%). So you should trade on Kalshi, right, because 51% is better odds than the sportsbook's 52.4%?

Caption: Same game, Sportsbook vs Kalshi fee comparison

No! The sportsbook odds are slightly worse, but Kalshi's Taker fee of $0.35 offsets this advantage:

- Kalshi: Bet $10.55 (buy 20 contracts, total $10.20 + $0.35 fee), win $20

- Sportsbook: Bet $10.55, win $20.14 (same bet amount, wins $0.14 more than Kalshi)

But this isn't the full picture, as Kalshi offers liquidity incentives and volume incentives. Also, the fee structure isn't uniform across all markets, and Kalshi pays yields on holdings, accrued daily.

Fees: The Math Part

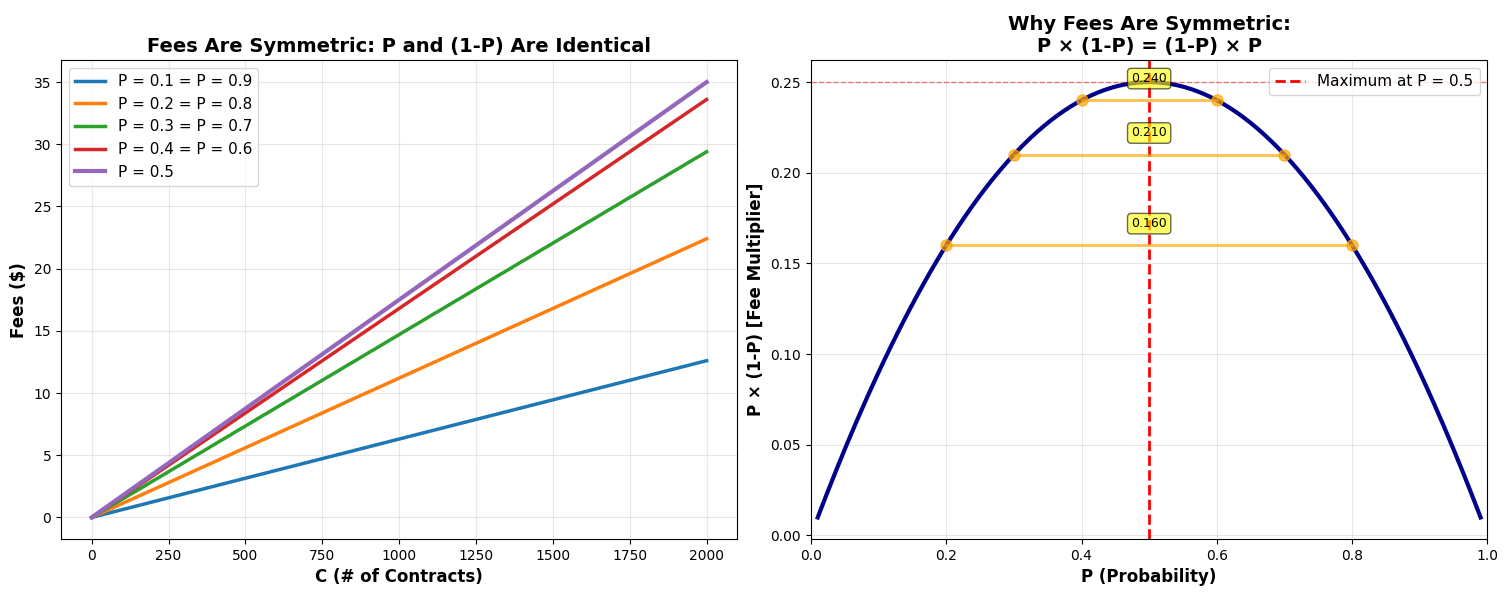

How much does Kalshi collect in fees from this volume? First, look at Taker fees. The formula is:

Fee = RoundUp(0.07 × C × P × (1-P))

Where C is the number of contracts, P is the price (ranging from $0.01 to $0.99).

Plotting the fee as a function of P and C. The price increases linearly with the number of contracts; P×(1-P) controls the shape of the fee curve—you can see that fees are lowest when the implied probability is far from 50%. Contracts with very high or very low probability have the lowest fees.

Caption: Fee vs. Implied Probability and Contract Count, right chart shows P(1-P) curve

What we've found here is essentially the Bernoulli distribution. The Bernoulli distribution models a single "yes/no" event (a market in our scenario).

- Variance can be expressed as P(1-P), where P is the "Yes" probability, corresponding to the Y-axis on the right chart.

- Variance ranges from 0 to 0.25.

- Entropy (uncertainty or randomness in the probability distribution) is maximized at P = 0.5.

Why doesn't Kalshi use a fixed fee? Likely due to trading considerations:

- If a contract price is 98 cents, the maximum potential profit is 2 cents. If Kalshi charged a fixed 2-cent fee, the profit would be 0, and no one would trade.

The Maker fee curve has the same slope, just scaled down overall because the multiplier is 0.0175 (a quarter of the Taker's): Fee = RoundUp(0.0175 × C × P × (1-P)).

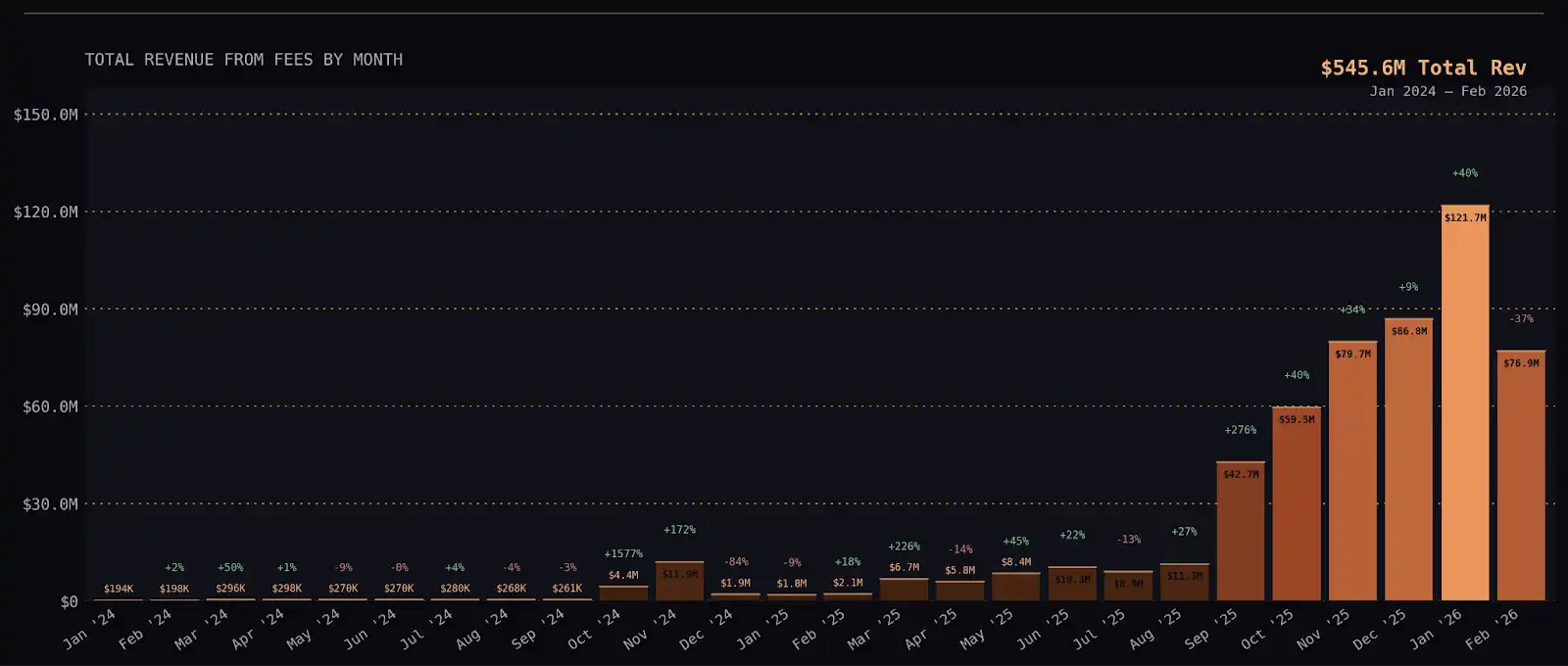

After downloading all 203 million historical trades from Kalshi, I know the exact execution price for each contract. Plugging P and C into the formula allows calculating Kalshi's total revenue from all contracts—$545.6 million.

Kalshi's monthly trading volume distributed by implied probability:

Caption: Monthly trading volume distributed by implied probability

Kalshi's monthly fee revenue:

Caption: Kalshi monthly fee revenue trend

The popularity of these markets is exploding, and DraftKings, FanDuel, and Fanatics are scrambling to join the party. The party's name is: "We're doing basically the same thing as sports betting, but it's pseudo-regulated and 18-year-olds can play".

Settlement

An interesting settlement case: Dallas and Green Bay tied in an NFL game. The market settled 50/50 instead of "Yes" or "No," 100 or 0. Prediction markets don't have the concept of pushing or voiding bets. In ambiguous situations, Kalshi intervenes. In the data, Kalshi labels such outcomes as "scalar," with over 170,000 markets tagged this way.

Kalshi's market settlement seems quite manual. They have a markets team that carefully reviews outcomes. Each market has an authoritative reference source. For example, the Super Bowl lists several data sources and specific rules. Nonetheless, they couldn't figure out if Cardi B performed, eventually settling that market at the last traded price.

Polymarket, on the other hand, stated "Yes, she performed," which also highlights their different settlement approach—using UMA's optimistic oracle. A topic for another time.

Conclusion

That's it, I have 9 more beers to drink, and I'm already way over the word count.

Legal aside: There's another prediction market called PredictIT, focused on political predictions. PredictIT is operated by a company called Aristotle, which does data mining for political campaigns. It launched in 2014 as a non-profit educational project by Victoria University of Wellington in New Zealand. To operate legally, they obtained a no-action letter from the CFTC, similar to what the IEM got, conditional on adhering to certain restrictions and serving academic purposes. Then in 2022, PredictIT got hit by the CFTC—for not operating according to the agreement. In 2025, they 360-no-scoped the CFTC in federal court, and the "Cadillac of prediction markets" is back.

Anyway, players in this "event contract" space are all submitting various letters and letters to the CFTC, requesting the CFTC not to take action against them for failing to meet regular reporting requirements. So far, the CFTC seems to agree, citing "limited applicability of traditional swap reporting rules to exchange-traded event contracts". There are other issues, like the classification of Kalshi and Robinhood, but overall, there's much discussion ahead on how to regulate, tax, and manage the reporting requirements for these "new" entities.