Author: Azuma

Original Title: Why Must Banks Kill Stablecoin Yields?

With Coinbase's temporary "betrayal" and the postponement of the Senate Banking Committee's review, the Cryptocurrency Market Structure Act (CLARITY) has once again fallen into a phase of stagnation.

-

Odaily Note: For previous developments, refer to "The Biggest Variable in the Post-Crypto Market: Can the CLARITY Act Pass the Senate?" and "CLARITY Review Suddenly Postponed: Why Is the Industry So Divided?".

Based on current market debates, the biggest point of contention surrounding CLARITY has focused on "yield-bearing stablecoins." Specifically, last year's GENIUS Act, to gain support from the banking industry, explicitly prohibited yield-bearing stablecoins. However, the Act only stipulated that stablecoin issuers cannot pay holders "any form of interest or yield," but did not restrict third parties from providing yields or rewards. The banking industry is very dissatisfied with this "workaround" and is attempting to overturn it in CLARITY, banning all types of yield-bearing pathways. This has drawn strong opposition from some cryptocurrency groups, represented by Coinbase.

Why are banks so opposed to yield-bearing stablecoins, insisting on blocking all yield pathways? The goal of this article is to answer this question in detail by dissecting the profit models of large U.S. commercial banks.

Bank Deposit Outflows? Pure Nonsense

In statements opposing yield-bearing stablecoins, the most common reason cited by banking representatives is "concern that stablecoins will cause bank deposit outflows." — Bank of America CEO Brian Moynihan said in a conference call last Wednesday: "Up to $6 trillion in deposits (about 30% to 35% of all U.S. commercial bank deposits) could migrate to stablecoins, thereby restricting banks' ability to lend to the overall U.S. economy... Yield-bearing stablecoins could accelerate deposit outflows."

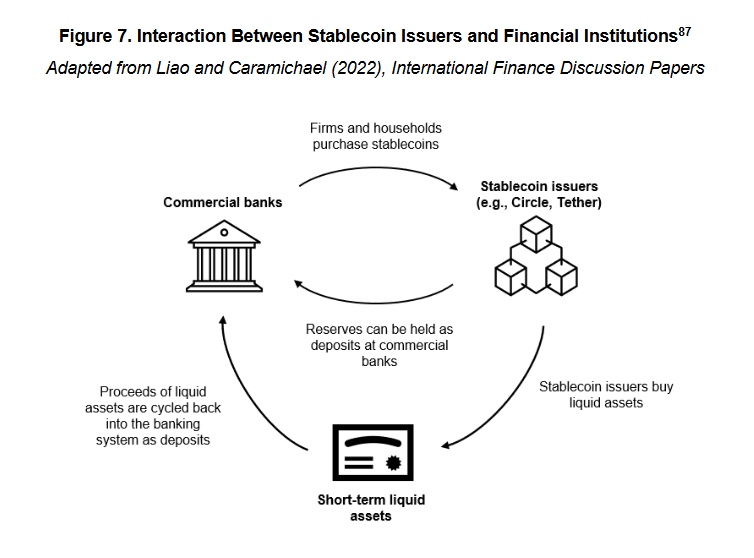

However, anyone with a basic understanding of how stablecoins operate can see that this statement is highly deceptive and misleading. Because when $1 flows into a stablecoin system like USDC, that $1 does not disappear into thin air. Instead, it is placed in the reserve treasury of stablecoin issuers like Circle and ultimately flows back into the banking system in the form of cash deposits or other short-term liquid assets (such as Treasury bonds).

-

Odaily Note: Stablecoins backed by crypto assets, futures hedging, algorithmic mechanisms, etc., are not considered here. Firstly, because such stablecoins account for a small proportion; secondly, because these stablecoins do not fall under the discussion scope of compliant stablecoins under the U.S. regulatory framework — last year's GENIUS Act clearly defined reserve requirements for compliant stablecoins, limiting reserve assets to cash, short-term Treasury bonds, or central bank deposits, which must be segregated from operational funds.

So the facts are clear: stablecoins do not cause bank deposit outflows because the funds always flow back to banks and can be used for credit intermediation. This is determined by the business model of stablecoins and has little to do with whether they yield interest or not.

The real key issue lies in the change in deposit structure after the funds flow back.

The Cash Cow of American Banks

Before analyzing this change, we need to briefly introduce how large U.S. banks make money from interest.

Van Buren Capital General Partner Scott Johnsson cited a paper from the University of California, Los Angeles, stating that since the 2008 financial crisis damaged the banking industry's credibility, U.S. commercial banks have diverged into two distinct forms in their deposit-taking business — high-interest banks and low-interest banks.

High-interest banks and low-interest banks are not formal regulatory classifications but common terms in market discourse — manifested in the fact that the deposit interest spread between high-interest banks and low-interest banks has reached more than 350 basis points (3.5%).

Why is there such a significant interest spread for the same deposit? The reason is that high-interest banks are mostly digital banks or banks whose business structure focuses on wealth management and capital market businesses (e.g., Capital One). They rely on high interest rates to attract deposits to support their credit or investment businesses. Conversely, low-interest banks are mainly national large commercial banks that hold the real power in the banking industry, such as Bank of America, JPMorgan Chase, and Wells Fargo. They have a vast retail client base and payment networks, allowing them to maintain extremely low deposit costs through customer stickiness, brand effect, and branch convenience, without needing to compete for deposits with high interest rates.

From the perspective of deposit structure, high-interest banks generally focus on non-transactional deposits, i.e., deposits主要用于储蓄或获取利息回报的存款 — such funds are more sensitive to interest rates and are more costly for banks; low-interest banks generally focus on transactional deposits, i.e., deposits主要用于支付、转账、结算的存款 — the characteristics of such funds are high stickiness, frequent流动性, and very low interest rates, making them the most valuable liabilities for banks.

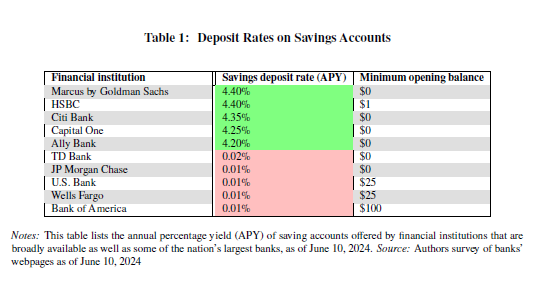

Latest data from the Federal Deposit Insurance Corporation (FDIC) shows that as of mid-December 2025, the average annual interest rate for U.S. savings accounts was only 0.39%.

Note, this is the data after including the impact of high-interest banks. Since mainstream U.S. banks predominantly follow the low-interest model, the actual interest they pay depositors is far lower than this level — Galaxy founder and CEO Mike Novogratz直言 stated in an interview with CNBC that large banks pay depositors almost no interest (about 1 – 11 basis points), while the同期 Federal Reserve benchmark rate was between 3.50% and 3.75%. This spread brings huge profits.

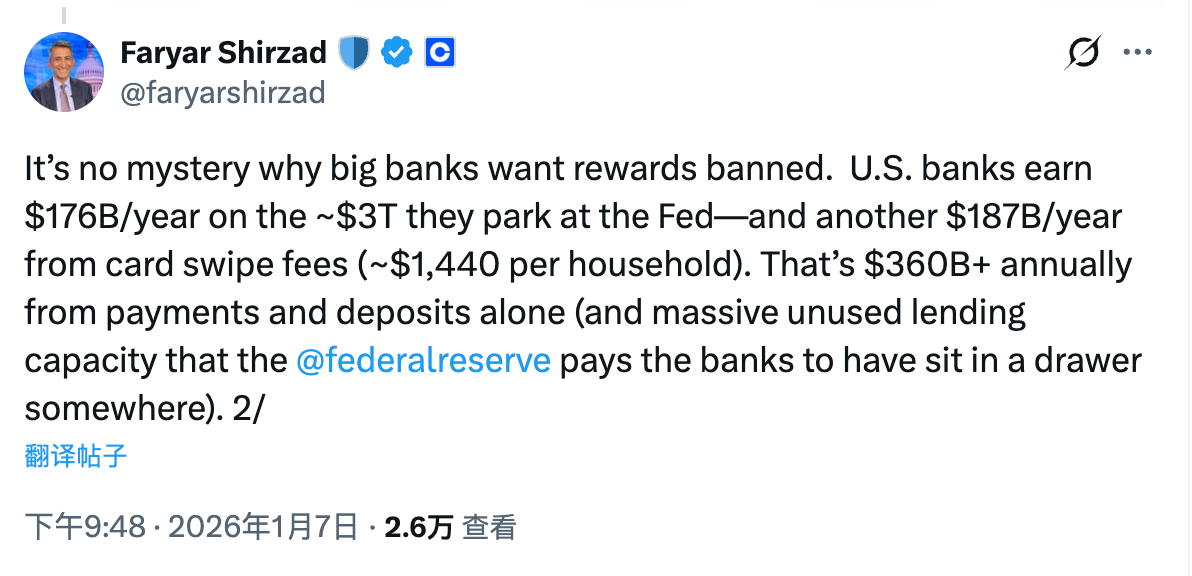

Coinbase Chief Compliance Officer Faryar Shirzad calculated a clearer account — U.S. banks can profit $176 billion annually from approximately $3 trillion in funds deposited with the Federal Reserve. Additionally, they earn $187 billion annually from transaction fees charged to depositors. Just the deposit spread and payment transaction环节 generate over $360 billion in revenue annually.

The Real Change: Deposit Structure and Profit Distribution

Back to the topic, what changes will the stablecoin system bring to the bank deposit structure? How will yield-bearing stablecoins助推 this trend? The logic is actually quite simple. What are the use cases for stablecoins? The answers无非是支付、转账、结算......等等, doesn't this sound familiar!

As mentioned earlier, these functions are the core utilities of transactional deposits, which are both the main deposit type for large banks and their most valuable liabilities. Therefore, the banking industry's real concern about stablecoins is — stablecoins, as a new transaction medium, can directly compete with transactional deposits in terms of use cases.

If stablecoins did not have yield-bearing functionality, it might be manageable. Considering the usage barriers and the slight interest advantage of bank deposits (a mosquito's leg is still meat), the actual threat stablecoins pose to this core stronghold of large banks is not significant. But once stablecoins are given the feasibility of yielding interest, driven by the interest spread, more and more funds might shift from transactional deposits to stablecoins. Although these funds will still ultimately flow back into the banking system, stablecoin issuers,出于利润考虑, will inevitably invest most of the reserve funds into non-transactional deposits, only needing to retain a certain proportion of cash reserves to handle daily redemptions. This is the so-called change in deposit structure — the funds remain in the banking system, but bank costs will increase significantly (the interest spread is compressed), and revenue from transaction fees will also shrink substantially.

At this point, the essence of the problem is very clear. The reason banks are疯狂 opposing yield-bearing stablecoins has never been about "whether the total amount of deposits within the banking system will decrease," but about the potential change in deposit structure and the resulting profit redistribution issue.

In the era without stablecoins, and especially without yield-bearing stablecoins, large U.S. commercial banks firmly controlled this source of "zero-cost or even negative-cost" funding — transactional deposits. They could earn risk-free profits through the spread between deposit rates and benchmark rates, and also continuously charge fees for basic financial services like payments, settlement, and clearing, thereby building an extremely solid闭环 that几乎不需要与储户分享收益.

The emergence of stablecoins essentially dismantles this闭环. On the one hand, stablecoins highly compete with transactional deposits functionally, covering core scenarios like payments, transfers, and settlement; on the other hand, yield-bearing stablecoins further introduce the variable of yield, making transactional funds, which were originally not sensitive to interest rates,开始具备了重新定价的可能.

In this process, funds do not leave the banking system, but banks may lose control over the profits from these funds — liabilities that were almost zero-cost are forced to transform into liabilities that require paying market-based yields; payment fees that were previously独占 by banks也开始被分流 to stablecoin issuers, wallets, and protocol layers.

This is the change that the banking industry truly cannot accept. Understanding this, it is not difficult to understand why yield-bearing stablecoins have become the most intense and最难妥协的争议焦点 in the CLARITY approval process.

Twitter:https://twitter.com/BitpushNewsCN

Bitpush TG Discussion Group:https://t.me/BitPushCommunity

Bitpush TG Subscription: https://t.me/bitpush