Author: momo, ChainCatcher

The decentralized perpetual futures (Perp DEX) market is currently in a new phase of reshuffling. Following Hyperliquid, protocols like Aster and Lighter have successively entered the market, breaking the old landscape. This indicates that competition is far from over before the infrastructure matures.

Against this backdrop, the newcomer Honeypot Finance provides a case study. It recently completed a new funding round at a $35 million valuation, receiving support from well-known institutions like Mask Network.

Unlike mainstream solutions, Honeypot's differentiation lies in its "full-stack" approach, which combines AMM and order book models. It goes beyond optimizing the trading experience, attempting to integrate token issuance, liquidity management, and derivatives trading into a synergistic system. The trading volume of its perpetual contracts has exceeded $20 million since launch.

This article will analyze Honeypot's product and mechanisms, exploring whether its full-stack integration model can build a sustainable, practical advantage in the current competition.

From Meme Launchpad to Full-Stack Perp DEX

Before entering the Perp DEX space, Honeypot's core focus was the Meme Launchpad. Through its star product Pot2Pump, the team directly addressed and attempted to solve the core pain points of the Memecoin economy at the time: how to capture and retain real, long-term value for the protocol during the狂热but short issuance cycles, rather than just one-off traffic.

Pot2Pump revolutionarily transformed early participants into native liquidity providers (LPs) from the token's inception, allowing the liquidity pool and the token to be born simultaneously. This design changed the恶性循环of early "scientist" arbitrage and rapidly depleting liquidity for Memecoins, turning high volatility into sustainable fee income for LPs.

Through Pot2Pump, Honeypot successfully validated an important model: in asset classes like Memecoins, characterized by high volatility and strong博弈, ingenious mechanism design can guide liquidity behavior, converting market hype into a stable stream of收益that can be shared by the protocol and the community.

However, Honeypot also quickly realized that Memecoins were more of an entry point for liquidity experiments, not the final form. The long-term viability of the protocol depends on whether capital can continuously trade, price, and be liquidated within the system.

Based on this judgment, the team expanded its perspective from单一发行to a complete structure encompassing market making, trading, and risk management, with perpetual contracts being the natural choice. Compared to spot trading or one-off发行, a Perp DEX can sustainably carry trading demand, generate stable fees, and transform volatility into manageable risk exposure.

Honeypot Finance's Differentiation and Innovation

When Honeypot Finance entered the perpetual contracts arena, it faced two mainstream paradigms, each with its own flaws.

On one side is the order book model reliant on market makers. It excels in efficiency during calm markets, but once volatility spikes, liquidity can evaporate instantly, leading to price gaps and users being liquidated under adverse conditions.

On the other side is the AMM model, exemplified by GMX. It uses oracle pricing to avoid information lag but makes liquidity providers the direct counterparty to all traders. In trending markets, these fund providers suffer continuous losses, often resulting in capital fleeing the protocol just when it needs support the most.

A deeper issue lies in the imbalance of risk and fairness: To ensure system stability, some protocols employ automatic deleveraging mechanisms (ADL), sacrificing some profitable traders' gains to cover losses in extreme situations, which raises widespread fairness concerns. Simultaneously, pooling all capital together without distinction hinders the entry of capital with different risk appetites, particularly large, conservative funds.

1. Building Full-Stack Liquidity: Order Book and AMM Working in Tandem

Addressing these structural issues, Honeypot did not choose to patch the old paradigms but proposed an integrated approach. Its core is building a "full-stack" perpetual DEX where the order book and AMM work协同, automatically adapting to different market conditions.

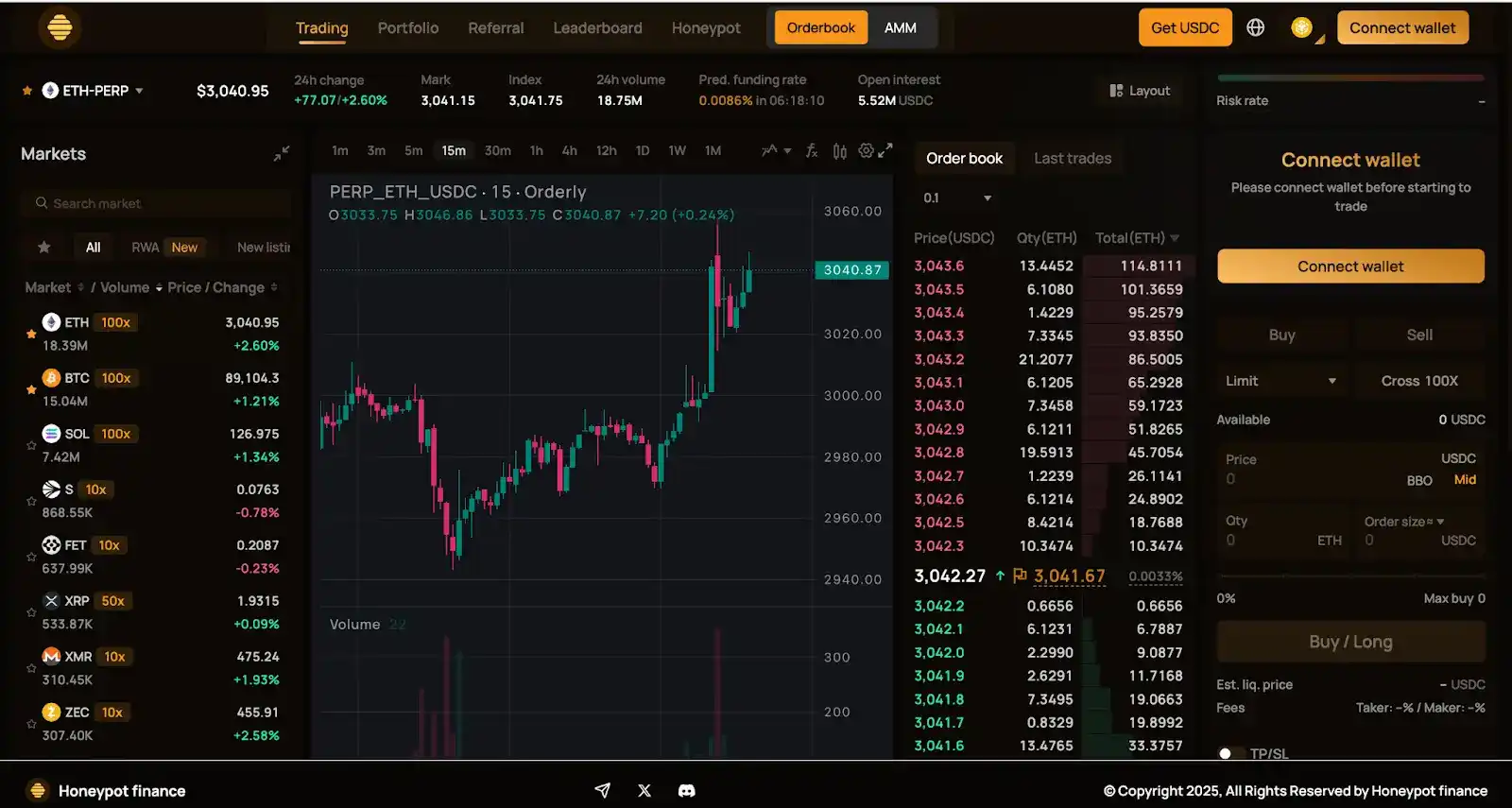

Order Book Handles Efficiency and Depth: By integrating a high-performance on-chain order book through a partnership with Orderly Network, Honeypot provides traders with a near-centralized exchange experience—low slippage, high speed—during stable market conditions, meeting the needs of高频and professional traders.

AMM Provides Resilience and Guarantee: Honeypot's self-developed AMM mechanism centers around a dynamic price band built around the oracle price. When the market experiences剧烈波动or black swan events, and order book liquidity dries up, the AMM acts as the final layer of executable guarantee, ensuring trades can be executed at any time.

The system automatically selects the optimal execution path (order book or AMM) for user trades based on market volatility and order book depth. Users get the best experience without manual intervention. This truly achieves "efficient trading in calm times, predictable execution in storms."

2. Implementing Structured Risk Control: Tiered Vaults and Fair Liquidation Process

In the core area of risk management, Honeypot's thinking is equally profound.

They started with the capital structure, introducing a tiered vault system.

This allows conservative capital seeking stable returns (like potential institutional capital) to enter the "Senior Vault," enjoying priority in fee distribution and being the last to bear losses, achieving risk isolation. Crypto-native players can voluntarily choose to enter the "Junior Vault," becoming the first line of defense to absorb losses in exchange for higher potential returns. This design transforms risk from a "passive, mixed burden" into an "active, clearly priced choice."

On this foundation, they redesigned the liquidation process, creating a "waterfall" sequence with multiple buffers.

When a position approaches liquidation, the system doesn't immediately liquidate it entirely. Instead, it sequentially attempts "Partial Liquidation," markets the position through a "Micro-Auction" for市场化处理, and has the Junior Vault absorb the loss. Following this, the Insurance Fund intervenes as a protocol-level buffer to cover extreme tail-risk events; only if all the above mechanisms are insufficient to stabilize the system is the minimally impactful and fully auditable ADL (Automatic Deleveraging) enabled as a last resort. This transparent design, which pushes punitive measures to the very end, aims to truly fulfill its promise of "procedural fairness."

Market feedback suggests this systemic design, from the foundational liquidity layer to the risk底层, is gaining initial validation. According to industry information, its platform's total trading volume has exceeded $120 million, and the perpetual contracts trading volume has surpassed $20 million since launch.

This data strongly indicates that the appeal of its risk-tiered structure to稳健capital has translated into real capital deposits. Through this series of designs, Honeypot not only attempts to solve existing pain points but also explores building a next-generation on-chain derivatives infrastructure capable of承载more complex capital and placing greater emphasis on fairness.

Token Economics and NFT Mechanism: How is the收益Closed Loop Achieved?

Honeypot Finance doesn't just aim to improve the trading experience; it attempts to build a self-sustaining收益system. Its token and NFT designs revolve around the same core goal: enabling the real revenue generated by the protocol to be continuously recaptured, redistributed, and, in turn, support the ecosystem itself.

1. HPOT: As a Vehicle for收益Bearing and Distribution

In many DeFi protocols, tokens primarily serve激励or governance functions, with limited connection to the protocol's actual revenue. Honeypot's token, $HPOT, with a fixed total supply of 500 million, is designed as a hub connecting trading activity and value distribution.

A portion of the trading fees generated by the protocol's products, like perpetual contracts, flows into the All-in-One Vault. Managed by the treasury and participating in on-chain strategies, these fees are converted into sustainable real yield. This yield is not simply retained; it is explicitly allocated:一部分is used to buy back and burn $HPOT, creating continuous supply contraction; another portion is distributed as claimable yield to users participating in the vaults.

In this structure, $HPOT is not just a speculative asset awaiting price fluctuations but a value carrier linked to the protocol's actual operational results. Its role is closer to a "收益relay" than a one-way incentive tool.

2. NFT: Transforming Long-Term Participation into收益Weight

Honeypot's HoneyGenesis NFT is not merely an identity or membership pass; it is a收益component designed around "long-term participation."

Holders can choose to stake the NFT, accumulating收益weight over time; or they can choose to burn the NFT in exchange for a permanent, higher收益multiplier. This design essentially incentivizes users to exchange time and commitment for higher long-term returns, rather than short-term arbitrage.

Here, the NFT de-emphasizes collectibility and instead functions as a "收益weight amplifier," making the act of participation itself a quantifiable, upgradable capital investment.

In summary, Honeypot attempts to avoid an "incentive consumption" model, instead basing ecosystem growth on real usage and revenue. The最终result is not one-way subsidies but a positive feedback system operating around收益recapture and redistribution.

Conclusion:

With the token即将上线, Honeypot Finance is transitioning from a project driven by early adopters and ecosystem builders to a broader, more complex public market.

Honeypot's current practice already provides a profound case study on structure, risk, and fairness for the on-chain derivatives track. Its core value lies not in the deepening of a single function but in a series of coherent design philosophies:

First, is the compatibility and scalability of the structure. The "full-stack" model is not just a hybrid solution born to cope with market volatility; it also reserves underlying interfaces to carry longer-term, more diverse capital and trading scenarios. The tiered vault design transforms risk from "passive sharing" into "active choice," paving the way for attracting traditional, conservative capital.

Second, is the long-term orientation of the economic mechanisms. Whether it's feeding protocol revenue back to users through token buyback/burns and claimable yield, or designing NFTs as upgradable "收益positions," the goal is to build a value closed loop of "participation equals accumulation." This logic aims to reduce reliance on one-off liquidity mining incentives and explore the possibility of continuing operation based on real use cases and sustainable收益distribution after incentives taper off.

Third, is the synergistic potential of the ecosystem. Honeypot's Perp DEX is not an isolated product but a key link in its full liquidity chain from asset issuance and spot trading to derivatives hedging. This deep integration means different products can potentially form a positive cycle of capital and user behavior, building a deeper moat.

However, after the initial hype subsides, can Honeypot translate its meticulously designed structural advantages into stable capital deposits, sustained real trading demand, and healthy protocol revenue? Can it prove that its advocated "procedural fairness" and risk tiering can truly protect users and maintain system stability in extreme market conditions? This still requires market validation.