Original | Odaily Planet Daily (@OdailyChina)

Author | Azuma (@azuma_eth)

Polymarket suddenly found itself in a fee controversy.

Last night, multiple community users discovered that they were charged abnormally high fees when trading on Polymarket, resulting in significantly reduced actual shares received or profits compared to before.

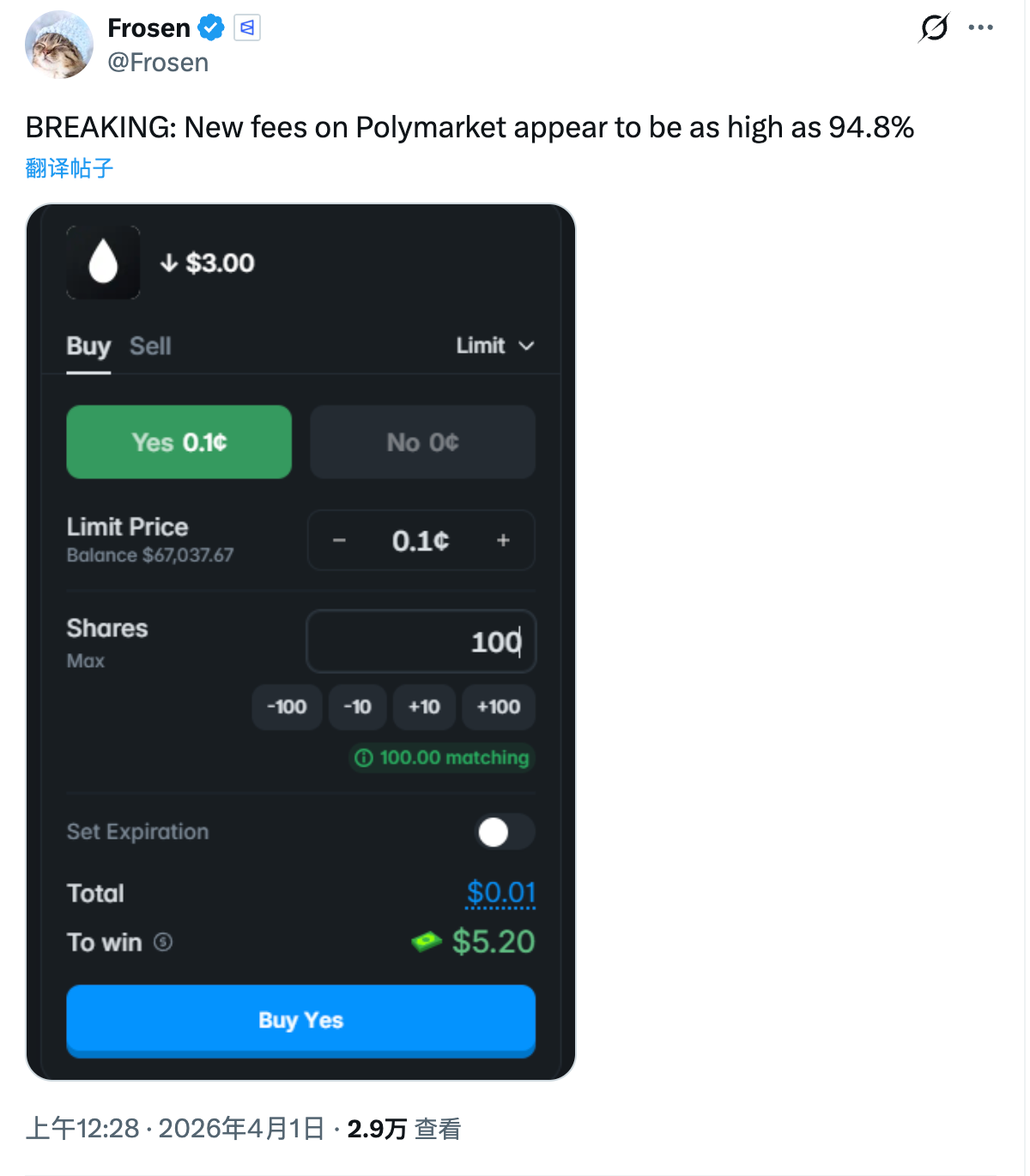

An overseas user, Frosen(@frosen), even posted a screenshot showing that when trying to place an order for 100 shares at a price of 0.1 cent in an "Economy" market, the potential winning profit displayed on the Polymarket frontend was only $5.2 (normally it should be $100) — corresponding to an outrageous fee rate of 94.8%!

What's going on? Is Polymarket that desperate for money? According to official disclosures from Polymarket and community investigations, Odaily found that the direct cause of this unexpected situation is that Polymarket modified the platform's fee formula last night.

In short, Polymarket changed the formula versions three times last night:

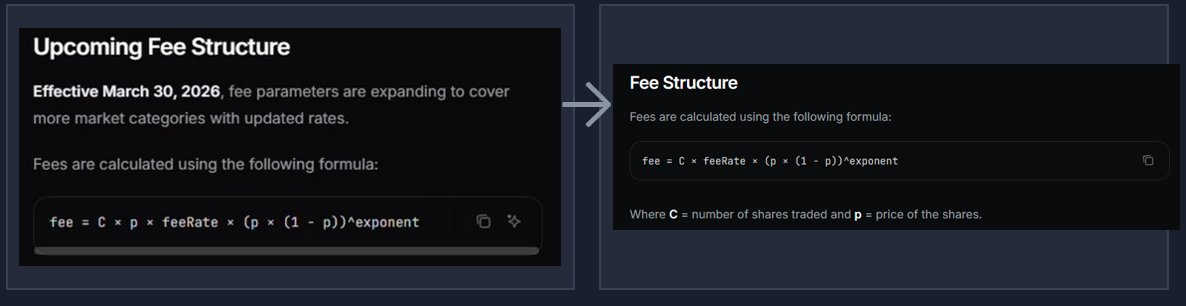

- First, the "Old Formula": fee = C × p × feeRate × (p × (1 - p))^exponent;

- Then the first change, the formula that caused the unexpected situation (referred to as the "Anomalous Formula"): fee = C × feeRate × (p × (1 - p))^exponent;

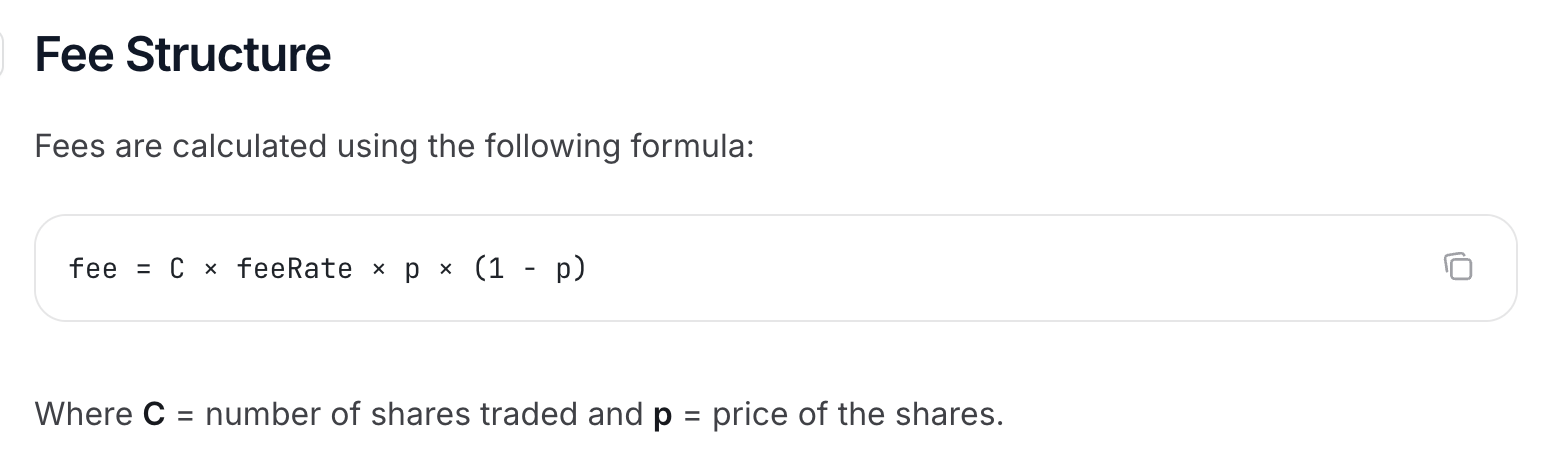

- After realizing the issue, Polymarket made a correction, resulting in the current version's "New Formula": fee = C × feeRate × p × (1 - p);

- It's important to note that in all three formulas, C refers to the number of shares traded, p refers to the price of the shares traded, and feeRate and exponent are variables.

Deconstructing the Anomalous Formula: How Did the Outrageous 94.8% Fee Rate Happen?

You don't need to worry too much about the mathematical details. By comparing the "Old Formula" and the "Anomalous Formula," you can simply see that the latter only removed a " × p" (this is the multiplication symbol, not a lowercase X) compared to the former, meaning it ultimately multiplied by the share price one less time.

Since the price of all shares on Polymarket is always less than $1, this would inevitably cause the overall fee to increase. The lower the share price, the more pronounced the increase in the fee due to one less multiplication — when the share price is close to 0, it could lead to very absurd fee rates.

As for how outrageous this fee could become, it also depends on the variable ^exponent, which exists in both the old and anomalous formulas. ^exponent directly translates to "raised to the power of exponent"; this variable is mainly used to control the steepness of the fee curve.

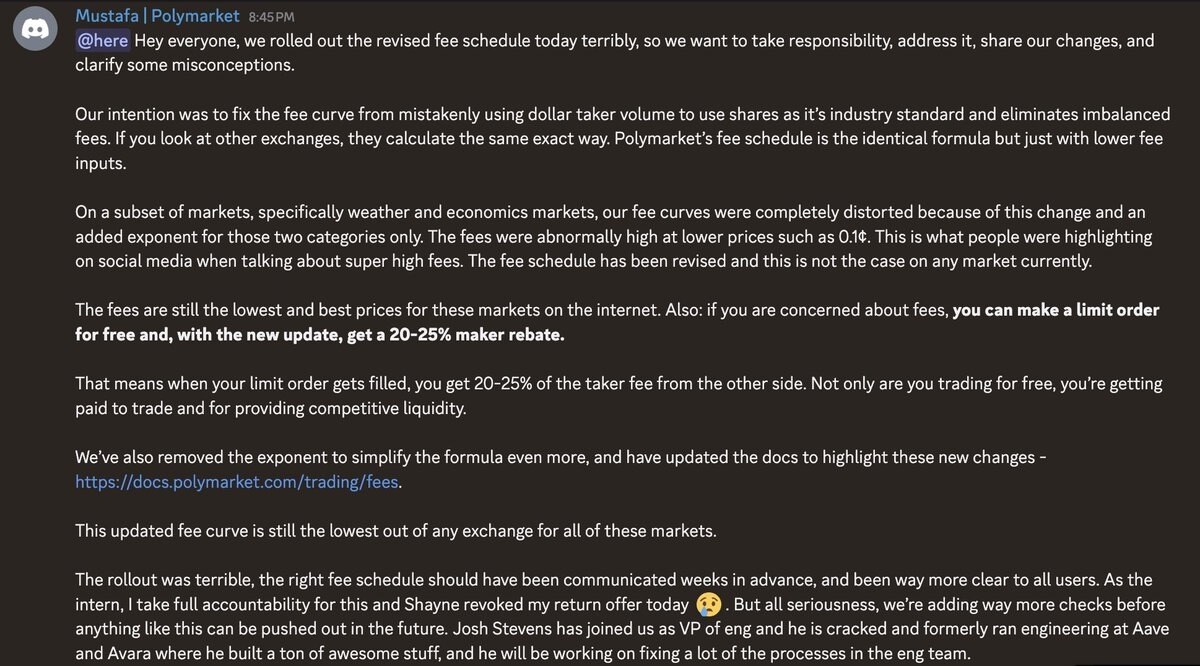

According to Mustafa, an official from Polymarket, the anomalous formula last night only introduced the exponent in the "Weather" and "Economy" market categories (other markets could ignore this variable by setting the parameter to 1). Furthermore, according to disclosures by overseas KOL Quant Chad(@Autonomous_Chad), the exponent parameter set for these two major markets at the time was 0.5.

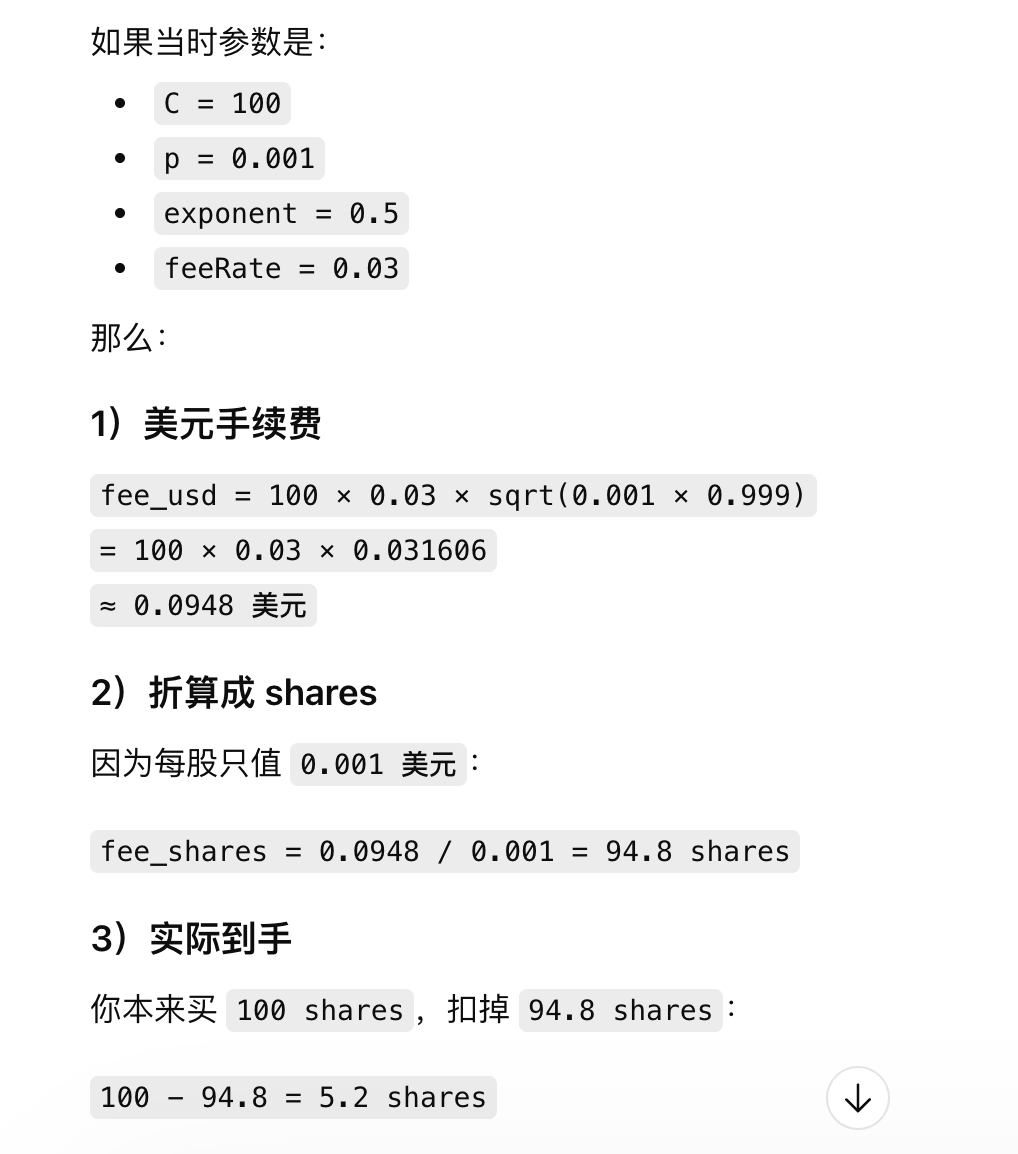

Now, back to Frosen's case, plug the corresponding numbers into the anomalous formula: fee = C × feeRate × (p × (1 - p))^exponent. It is known that C equals 100, meaning Frosen wanted to order 100 shares; p equals 0.001, i.e., $0.001 (0.1 cent); exponent equals 0.5, meaning perform an exponentiation operation on (p × (1 - p)); the final fee rate is 94.8%.

Throwing this directly to AI allows us to inversely deduce that the feeRate level at the time was 0.03, and also reconstruct the detailed formula calculation Polymarket performed for this order.

Simply put, based on the anomalous formula, Polymarket calculated that the fee for this order should be $0.0948. Since Polymarket deducts fees for buy orders by directly deducting the corresponding value in shares, and the share price at the time was only $0.001, it meant deducting 94.8 shares. Therefore, Frosen ultimately received only 5.2 shares, and even if the prediction was correct, the potential profit would only be $5.2.

Polymarket's Remedial Measures

Shortly after the abnormal fee issue emerged, Polymarket quickly responded by changing the formula to the current version: fee = C × feeRate × p × (1 - p). Compared to the anomalous formula, the new formula removed the "^exponent" — essentially, it increased the exponent parameter in the anomalous formula fee = C × feeRate × (p × (1 - p))^exponent from 0.5 to 1.

In the anomalous formula, the effect of ^exponent was to perform an exponentiation operation on the data set p × (1-p). In the actual operational context of Polymarket, the theoretical result range of p × (1 - p) is between "0.000999 - 0.25" — the closer p is to 0.5 (share price closer to $0.5), the closer this data set is to 0.25; the closer p is to 0 or 1 (share price closer to $0 or $1, with extremes at $0.001 and $0.999), the closer this data set is to 0.000999.

Within the range of "0.000999 - 0.25", regardless of the value taken, when the exponent parameter is increased from 0.5 to 1, it directly reduces the final fee result in the formula operation, i.e., lowers the overall fee.

More importantly, this reduction has a more pronounced inhibitory effect on the abnormally high fee rates near extreme low prices — when p × (1-p)=0.000999, the fee under the new formula is only about 3.16% of the fee under the anomalous formula, equivalent to a reduction of about 96.84%; whereas when p × (1-p)=0.25, the fee under the new formula is 50% of that under the anomalous formula.

As shown in Polymarket's official documentation, after the new formula was implemented, the fee rate at extremes in the "Weather" and "Economy" market categories has now been reduced to 5%.

How Can Retail Users Avoid Fees?

I know most users can't be bothered to look at the formulas above but are still concerned about Polymarket's current fee issues.

Regarding this, Mustafa mentioned in the official Discord: "If you are worried about fees, you can place limit orders for free, and after this new update, you can also get a 20%-25% maker rebate — this means that when your limit order is filled, you will receive 20%-25% of the taker fee paid by the counterparty. So not only are you trading for free, but you can even get paid by trading and providing competitive liquidity."

So change your habits. Try to avoid taking orders directly. Switch to using limit orders more often. You can also try using Polymarket's Split function more to indirectly build a position by placing a reverse limit order to sell the other side of shares.