Author: Goldman Sachs

Compiled by: Deep Tide TechFlow

- Following last year's strong growth, Goldman Sachs Research predicts that global stock markets are poised to continue climbing in 2026, with an expected return of 11% over the next 12 months (including dividends, in USD terms).

- Although last year's stock market rally has left valuations at historically high levels, corporate earnings and economic growth worldwide are expected to continue supporting the markets.

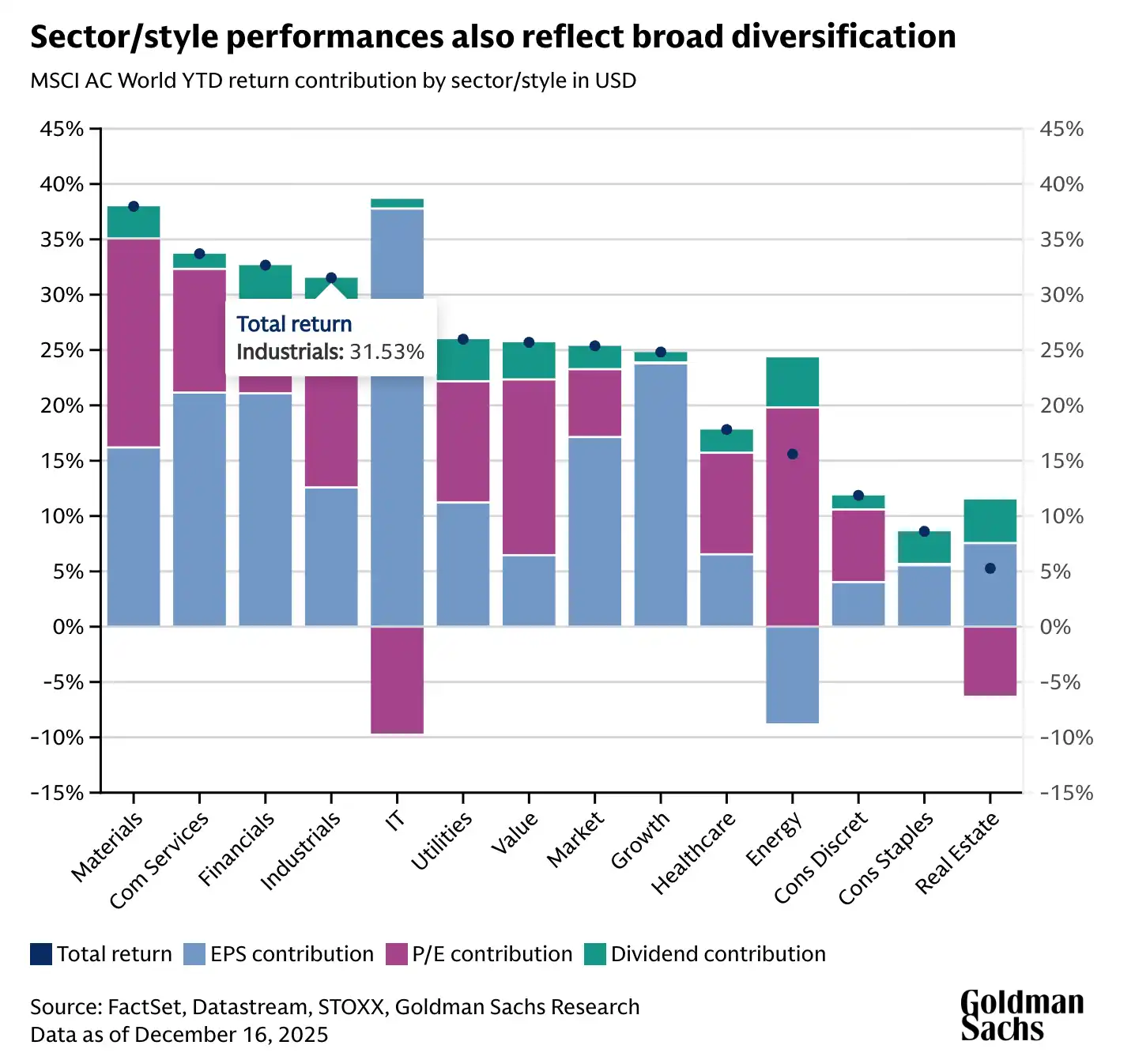

- Last year, investors benefited significantly from cross-regional diversification, a trend that is likely to continue. Additionally, diversifying across investment styles and sectors is expected to further enhance returns.

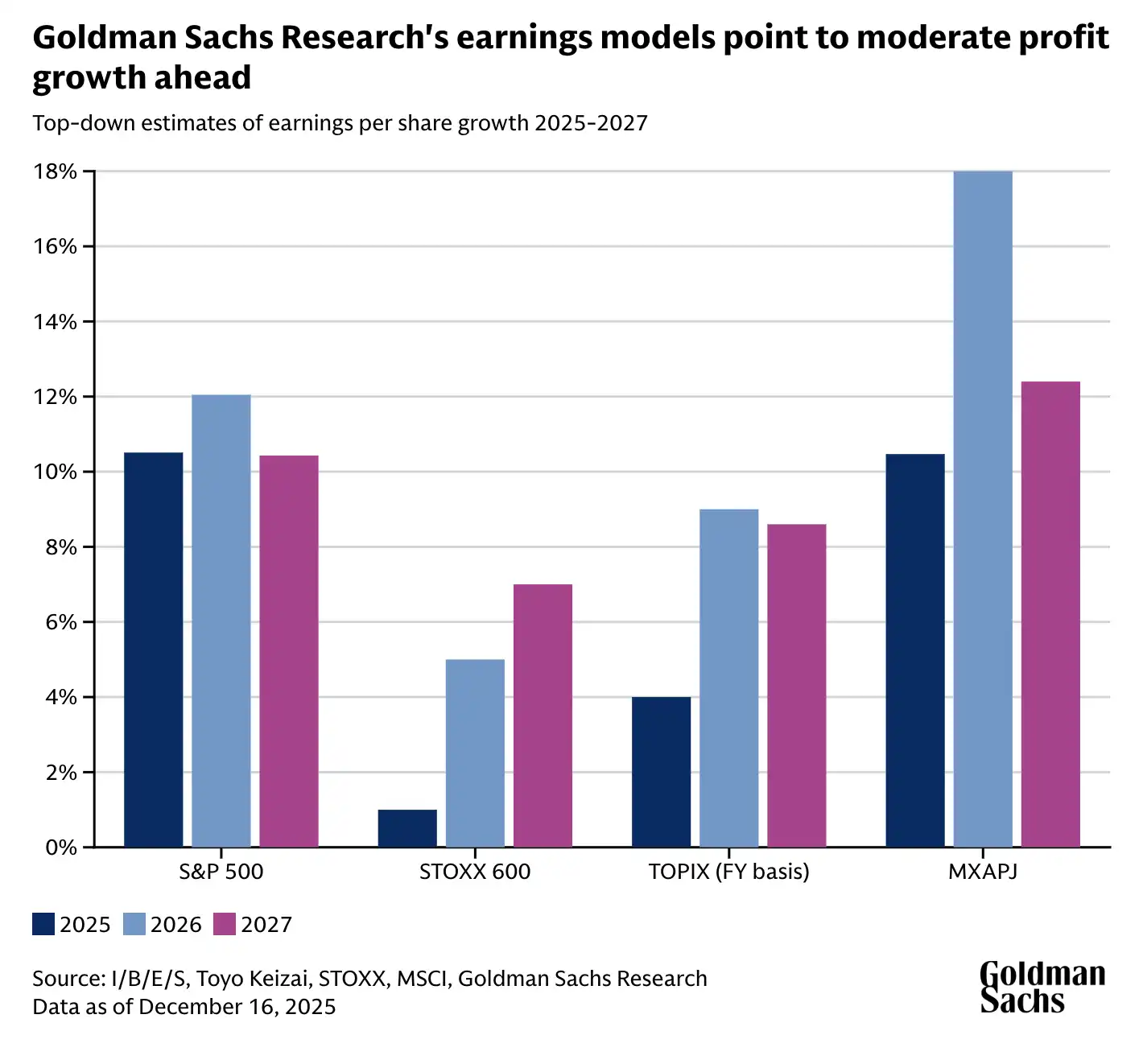

According to Goldman Sachs Research, the global bull market is likely to persist this year, driven by growth in corporate earnings and continued economic expansion. However, the gains in the stock market are expected to be more modest than the significant rally seen in 2025. In 2026, the global economy is anticipated to maintain its expansion across regions, with the US Federal Reserve expected to continue with moderate easing policies.

"In the current macroeconomic context, even with high valuations, a significant stock market correction or bear market in the absence of a recession would be unusual," wrote Peter Oppenheimer, Chief Global Equity Strategist at Goldman Sachs Research, in his report titled "Global Equity Strategy 2026 Outlook: Tech Tonic—a Broadening Bull Market".

Diversification was a core theme emphasized by Goldman Sachs Research last year. In 2025, for the first time in many years, investors who diversified across regions were rewarded. Goldman Sachs analysts expect this trend to continue in 2026 and expand to include diversification across investment factors such as growth and value, as well as across various sectors. (Investment factors refer to asset characteristics such as size, value, or momentum that typically influence risk and return.)

What is the Outlook for Global Stock Markets in 2026?

Despite the strong performance of stock markets in 2025, outperforming commodities and bonds, the rally was not without its challenges. At the beginning of the year, stocks performed poorly, with the S&P 500 experiencing a nearly 20% correction from mid-February to April before rebounding.

Peter Oppenheimer, Chief Global Equity Strategist at Goldman Sachs Research, noted that the robust rally in global equities has left valuations at historically high levels across all regions, including the US, Japan, Europe, and emerging markets.

"Therefore, we believe returns in 2026 are more likely to be driven by fundamental earnings growth rather than further multiple expansion," Oppenheimer said. According to Goldman Sachs analysts' forecasts as of January 6, 2026, global share prices (weighted by regional market capitalization) are expected to rise 9% over the next 12 months, delivering an 11% return in USD terms (including dividends). He added, "The majority of the return comes from earnings."

Furthermore, according to another Goldman Sachs forecast, commodity indices are also expected to rise this year, with gains in precious metals once again offsetting declines in energy prices, a trend similar to 2025.

Oppenheimer's team also examined the typical progression of market cycles: the despair phase during bear markets; the short-lived hope phase during market rebounds; the longer growth phase where returns are driven by earnings growth; and finally, the optimistic phase where investor confidence increases and even becomes complacent.

Their analysis suggests that stocks are currently in the optimistic phase of a cycle that began with the bear market during the COVID-19 pandemic in 2020. "This late-cycle optimistic phase is often accompanied by rising valuations, suggesting there may be some upside risk to our core forecast," Oppenheimer's team wrote.

Should Investors Diversify Their Stock Portfolios in 2026?

In 2025, geographical diversification provided significant benefits to investors, which is not common. US stock market performance lagged behind other major markets for the first time in nearly 15 years. Due to a weaker US dollar, returns from European, Chinese, and Asian stock markets were nearly double the total return of the S&P 500.

Returns in the US market were primarily driven by earnings growth, especially from large technology companies. However, outside the US, the balance between earnings improvement and valuation expansion was more even. Last year, the growth-adjusted valuation gap between US stocks and the rest of the world narrowed.

"Even though absolute valuations in the US remain high, we expect these growth-adjusted valuation ratios to continue converging in 2026," Oppenheimer's team wrote.

Oppenheimer noted that diversification is still expected to provide better risk-adjusted returns in 2026. He advises investors to seek broad geographical opportunities, including increased focus on emerging markets. Simultaneously, investors should balance between growth and value stocks and pay attention to different sectors. Furthermore, there is potential for lower correlation between stocks, providing good opportunities for stock selection.

"As stock correlations decline and potentially remain low, we are also paying more attention to enhancing alpha," wrote Peter Oppenheimer, Chief Global Equity Strategist at Goldman Sachs Research. Alpha measures an asset's performance relative to a broader market index.

Oppenheimer added that non-tech sectors might perform strongly this year, and investors could profit from stocks benefiting from tech companies' capital expenditures. Moreover, as new AI capabilities are gradually realized, market attention may increasingly focus on companies outside the tech sector that benefit from AI development.

Are AI Stocks in a Bubble?

Overall, market focus on artificial intelligence "remains fervent," Goldman Sachs analysts noted. However, this does not mean a bubble exists in the AI field. "The dominance of the tech sector in the market was not triggered by the rise of AI," Oppenheimer wrote. "This trend began after the financial crisis and has been supported by its exceptional earnings growth."

Despite the soaring stock prices of large tech companies, current valuation levels have not reached the extremes seen in previous bubble periods. For example, comparing the valuation gap between the five largest companies by market cap in the S&P 500 and the other 495 stocks shows this gap is much smaller than in previous cycles, such as the peak of the tech bubble in 2000.