As the Federal Reserve surprisingly turned significantly hawkish and mainstream Wall Street institutions successively withdrew their easing expectations, Citigroup has insisted on a contrarian view, believing that rate cuts within the year are still highly probable, with its baseline scenario locking in a resumption of the easing cycle in October.

At the June FOMC meeting, 9 out of 18 Fed officials projected rate hikes this year in their dot plots, far exceeding market and analyst expectations. In the post-meeting statement, Chair Walsh formally removed the "easing bias" language and refused to provide any forward guidance. Impacted by this shock, the swap market swiftly brought forward expectations for the first rate hike from March 2027 to October this year. The market is currently pricing in about 37 basis points of hikes for the remainder of the year, with the 2-year Treasury yield posting its largest single-day gain since March after the meeting.

Faced with this hawkish shock, Wall Street institutions have changed their stances one after another. In its latest research report, Deutsche Bank officially withdrew its easing forecast, now expecting the Fed to hike rates by 50 basis points cumulatively in September and December, pushing the rate to 4.1%, and warning that action could come as early as July. Goldman Sachs Vice Chairman and former Dallas Fed President Rob Kaplan warned that if inflation data remains stubborn, the Fed could restart rate hikes as early as autumn, most likely in a series of 2 to 3 consecutive actions.

In contrast, the team led by Andrew Hollenhorst at Citigroup has maintained its baseline forecast that starkly differs from the market: the next move will be a rate cut, not a hike. The baseline scenario is a 25 basis point cut in October, followed by another 25 basis point cut each in December and January 2027. Citi's core arguments are as follows: a sharp drop in oil prices is removing the main upside risk to inflation; the trend of rising initial jobless claims is replicating the seasonal weakening patterns seen in 2024 and 2025; and among various inflation indicators, core PCE is increasingly appearing as an "outlier," with its strength reflecting more the impact of stock price gains rather than broad consumer price pressures.

Citi's First Logic: Falling Oil Prices Are Removing Inflation Upside Risk

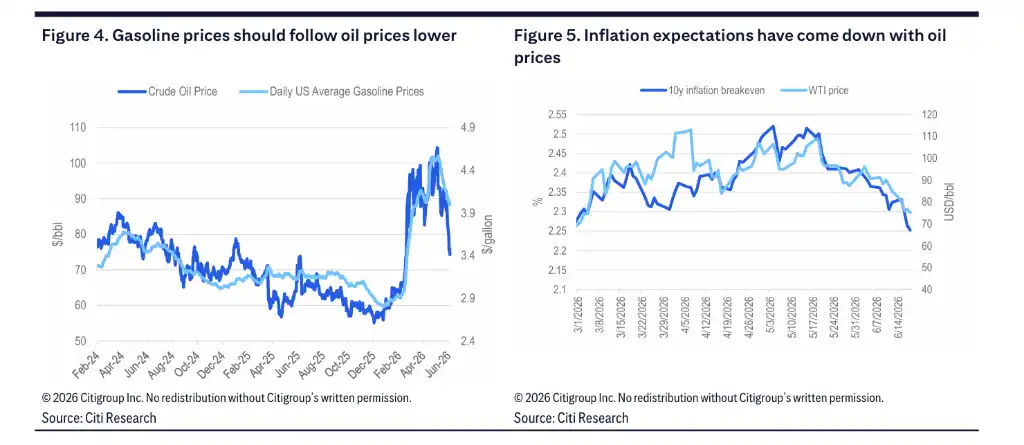

The first core argument underpinning Citi's insistence on rate cut forecasts stems from the rapid decline in oil prices. The bank believes that lower oil prices will lead to a decrease in gasoline prices, thereby removing a major source of the previous inflationary uptick. Market-based inflation expectations have already fallen in sync with oil prices, with the 10-year inflation breakeven rate dropping to levels seen before the outbreak of conflict.

Citi suggests that if Fed officials had more time to digest this latest change in energy prices, the hawkish tone of this FOMC meeting would have been significantly milder. The bank argues that as the effect of lower oil prices gradually manifests in the data, inflation figures in the coming months will trend towards moderation, helping to push more Fed officials towards a more dovish stance before September and create conditions for rate cuts before the year-end.

Citi's Second Logic: Labor Market Weakness Signals Replicate Past Seasonal Patterns

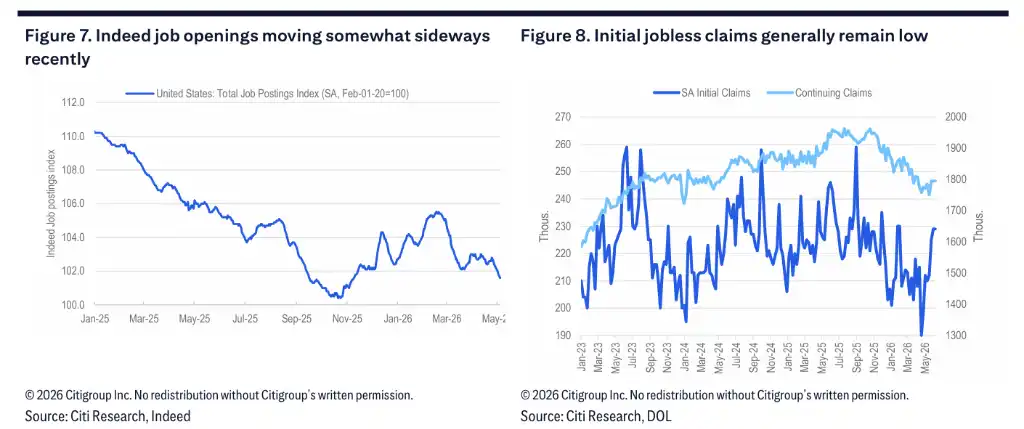

Citi's second core argument focuses on early signs of weakness emerging in the labor market.

Both initial and continuing jobless claims have shown an upward trend for several consecutive weeks. Citi notes that this pattern also appeared in both 2024 and 2025, subsequently leading to a series of weaker monthly employment reports and rising unemployment rates. A rising unemployment rate is a key driver behind Citi's expectation for Fed rate cuts this year. The bank expects initial jobless claims for the week of June 20 to remain around 224,000, with continuing claims rising slightly to 1.813 million, and the 4-week moving average to continue climbing. While the absolute levels are still not high, if the rising trend persists, it would align with the view of a gradually weakening labor market.

Regarding the overall economy, Citi's tracking forecast for Q2 GDP growth is 2.5%. On the consumption front, the May retail sales control group data showed a 0.7% month-over-month increase, indicating ongoing resilience. However, growth in real disposable income has slowed to nearly zero, and the savings rate remains low, suggesting that risks of a slowdown in spending growth are accumulating.

Citi's Third Logic: Core PCE is an 'Outlier,' The Inflation Picture is Not Unified

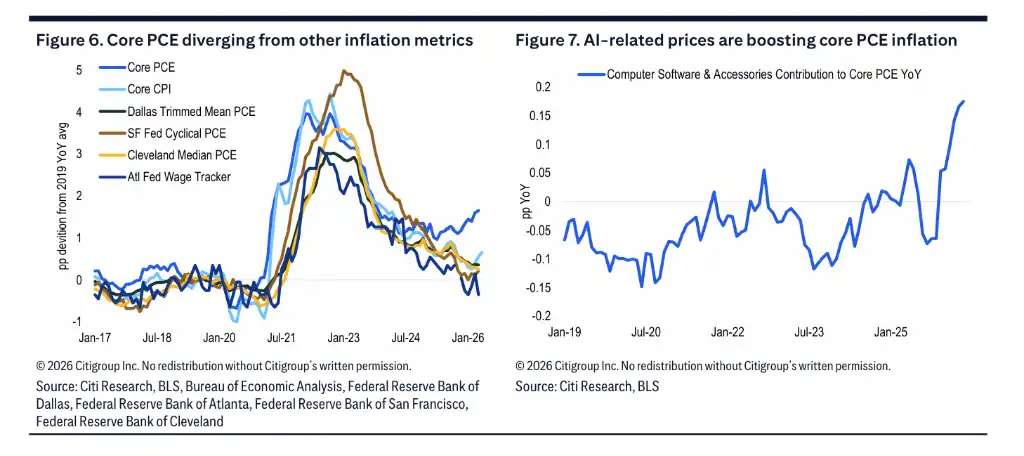

The third pillar of Citi's contrarian stance lies in questioning the core PCE data itself.

The May core CPI month-over-month reading was only 0.21%, showing moderation. However, Citi expects the upcoming May core PCE month-over-month reading to be as high as 0.37%, indicating a significant divergence between the two. Citi believes the current strength of core PCE has specific reasons: this measure is highly influenced by AI-related prices and is directly boosted by stock market gains—May PPI data showed a 4.8% month-over-month surge in portfolio management fees, mainly reflecting the rebound in stock prices from early April lows to early May highs, rather than genuine price pressures on the consumer side.

Looking at cross-sectional comparisons, the Dallas Fed's Trimmed Mean PCE, the San Francisco Fed's Cyclical Core PCE, the Cleveland Fed's Median PCE, and core CPI all show more moderate inflation trends than core PCE. Citi argues that core PCE is increasingly becoming an "outlier" among various inflation indicators, rather than a reliable signal of broad consumer price pressures.

Citi expects that as AI-related prices level off in the second half of the year, the gap between core PCE and core CPI will gradually narrow, and the overall inflation trend will become more supportive of policy easing. Under its forecast path, the year-over-year growth rate of core PCE is expected to gradually decline from the current level around 3.3% to the 2.1%-2.2% range around mid-2027.

Wall Street 'Capitulation': Deutsche Bank Forecasts Two Hikes, Goldman Sachs Warns of Serial Tightening

However, faced with Walsh's hawkish shock, Wall Street institutions have been changing their positions. Deutsche Bank's Chief US Economist Matthew Luzzetti's team clarified in a research report that the main reasons for their earlier delay in raising forecasts were two major uncertainties: the high degree of economic uncertainty stemming from the Iran situation, and the lack of clarity regarding new Fed Chair Walsh's monetary policy reaction function. The outcome of the June FOMC meeting resolved both these concerns at once.

Deutsche Bank significantly raised its inflation forecasts, lifting its expectations for year-end 2026 and 2027 core PCE to 3.2% and 2.5%, respectively. It updated its baseline forecast to: the Fed will hike rates twice in September and December, totaling 50 basis points, raising the rate to 4.1%; thereafter, it will remain on hold throughout 2027, only starting to cut rates in the first half of 2028. Deutsche Bank also warned of hawkish risks: if Chair Walsh has publicly committed to "fixing" the price stability issue and the Committee does not act promptly, its credibility could be tested—this implies a rate hike could come as early as July, and if the goal is to fully undo the easing effect generated by last year's consecutive rate cuts, the total hike for the year might need to be expanded to 75 basis points.

Goldman Sachs Vice Chairman Rob Kaplan explicitly stated that if inflation data fails to cool from now until September, a rate hike in autumn would be a "wise move." He particularly emphasized that the Fed's policy adjustments rarely occur as isolated, single actions; rate changes typically unfold in a series of 2 to 3 moves: "If they act in September, you need to be prepared, there could be one or two more hikes." Kaplan's warning, based on historical experience from navigating multiple monetary policy cycles, serves as a wake-up call for the market.