In San Francisco, a tech couple with a combined annual income exceeding $360,000 spent three months viewing 30 apartments but couldn't secure a one-bedroom for under $5,000 a month. With OpenAI and Anthropic on the verge of their IPOs, AI-fueled wealth is redefining the city's cost of living. A six-figure salary has become the new "not enough."

Katrine Razniak, 27, joined LinkedIn in 2022 as a recruiting coordinator with a $70,000 salary.

After moving to the software company Rippling, her salary increased to $180,000, where she leads a team of account managers.

Her partner, Adam Woodbury, 39, is a software engineer earning $185,000 annually.

Their combined income is over $360,000.

In the vast majority of American cities, this would be a ticket to upper-middle-class life.

In San Francisco in 2026, this ticket can't even secure a decent apartment.

This spring, the couple began their apartment hunt.

Their target wasn't outrageous: a one-bedroom apartment for under $5,000 per month. Over three months, they viewed around 30 units. All were over budget, or the competition was too fierce. For one apartment listed at $5,200, the sign-up sheet was filled with 30 names within an hour of the open house.

Eventually, they gave up.

Razniak says, "I don't feel completely hopeless, but I feel like I can't continue to live in San Francisco."

Woodbury adds, "At a certain point, we both slowly realized that staying here no longer made sense."

According to U.S. Census Bureau data, Woodbury's income roughly places him in the top 20% of household incomes nationwide.

His own perception, however, is different: "I feel like I'm not qualified to live here anymore, because I don't work at an AI company."

This statement accurately describes what's happening in San Francisco in 2026: AI companies are rapidly squeezing the quality of life for workers in other industries (including even other internet companies).

What $180,000 a Year Actually Means in Monthly Take-Home Pay

$180,000 is roughly 1.2 million RMB.

This seven-figure number has impact, but it's far from as comfortable as it sounds and definitely does not equate to $15,000 deposited into a bank account every month.

In Silicon Valley's tech circles, the salary figure almost always refers to Total Compensation, or the "total package."

An $180,000 annual salary is likely structured like this: Base Salary makes up about 75%-80%, roughly $135,000 to $145,000. The remainder is pieced together from equity incentives (RSUs or options), a sign-on bonus, and performance bonuses.

For a pre-IPO company like Rippling, the equity portion is paper wealth, not something you can live on.

A sign-on bonus is typically a one-time payment; spread over a year, it might add only a few hundred dollars per month.

The only part you can actually spend monthly is the base salary.

So, how much is the take-home pay from the base salary?

For a base salary of $140,000, the pre-tax monthly income is about $11,667.

Then comes the familiar pain for California workers: taxes.

Effective federal income tax rate is about 15%-16%, effective California state tax rate is about 6%-7%, Social Security and Medicare (FICA) are a fixed 7.65%, plus California's unique State Disability Insurance (SDI) at 1.3%. Combined, these deductions amount to roughly $4,100 to $4,500 per month.

If you factor in 401(k) retirement contributions (a typical 5%-6%) and the employee's share of health insurance, the actual monthly take-home pay is probably between $6,500 and $7,500.

Taking a median value: monthly take-home pay is $7,000.

Next, rent.

San Francisco's current average apartment rent is $3,827 per month, having surpassed New York City to become the most expensive in the U.S.

The actual transaction price for a one-bedroom typically ranges from $4,500 to $5,200.

Razniak searched for three months and couldn't find anything under $5,000.

$7,000 minus $4,500 leaves $2,500.

This $2,500 must cover utilities (41% more expensive than the national average), transportation (43% more), groceries (19% more), phone bills, and an occasional meal out with friends.

Calculated out, a $180,000 salary leaves roughly $1,500 to $2,500 per month in truly discretionary income.

Converted to RMB, that's about 10,000 to 18,000 RMB in disposable monthly income.

This is the real feel of a "six-figure salary" in San Francisco.

Razniak once said she thought that once she reached a $200,000 salary, she could basically stop worrying about money.

The reality is that last year, she and her friends stopped going to restaurants altogether, opting instead to cook at home, gather, and watch reality TV together.

What really makes this figure sting is the comparison group.

According to data from Levels.fyi (updated in June), the median total compensation at OpenAI is $640,000 company-wide, with the median for software engineers exceeding $800,000.

For L5-level engineers, multiple sources cite data points between $840,000 and $1.15 million.

Anthropic's company-wide median is about $420,000, with the median for software engineers around $750,000.

The base salaries of mid-to-senior engineers at these two companies already exceed Razniak's entire total compensation package.

Razniak earns a good salary, but she lives among people who earn much, much more.

Who's Driving Prices Sky-High?

San Francisco's cost of living has always been high, but the surge since 2024 has a clear driver—AI wealth creation.

OpenAI and Anthropic, both headquartered in San Francisco, have a combined valuation nearing $1 trillion and are preparing for IPOs.

Analysis from private market research firm Sacra shows that just these two companies, plus Elon Musk's newly public SpaceX, could create more than 20 new billionaires among current and former employees.

San Francisco's chief economist, Ted Egan, points to a scale issue.

When Uber went public in 2019 with an $82 billion valuation, it was already a capital event that impacted the city's housing prices.

Today, OpenAI and Anthropic's valuations are over 10 times that of Uber's at its IPO.

How specific is this?

OpenAI currently has about 7,850 employees, with an average equity incentive of approximately $1.5 million per employee in 2025—seven times (adjusted for inflation) the average per employee at Google before its IPO.

When this equity turns into real money through IPOs, this wealth will pour into San Francisco's real estate, consumer, and rental markets.

Mayor Daniel Lurie mentioned in a statement that the city is working to reduce costs through improved childcare, family housing zoning plans, and better public transit. However, he did not specifically address the plight of the six-figure income group.

To policymakers, someone earning $180,000 a year isn't considered vulnerable. But when such people start leaving in batches, the city also loses the mid-level technical talent it relies on to function.

Looking at the data, money is flooding in.

San Francisco's average annual salary rose from $153,359 in 2020 to $196,365 in 2025, a 28% increase.

But this is an average. An average inflated by the super-high salaries at AI companies, which for other tech workers feels more like an irony.

A City at a Boiling Point

Housing is the most obvious pain point.

According to a Redfin report, San Francisco's median home price broke $1.7 million in April, while the national median is around $450,000.

CoStar data shows San Francisco's average apartment rent reached $3,827 per month, and in recent months, it has overtaken New York City to become the highest in the nation.

Nigel Hughes, a senior researcher at CoStar, used the term "pressure cooker": "and it's heating up very fast."

In San Francisco's most sought-after neighborhoods—Marina District, Pacific Heights, South of Market—the apartment vacancy rate has dropped to about 3%. In 2020, that number was 13%. Meanwhile, new housing construction has nearly stalled.

With supply stagnant and demand exploding, prices can only go in one direction.

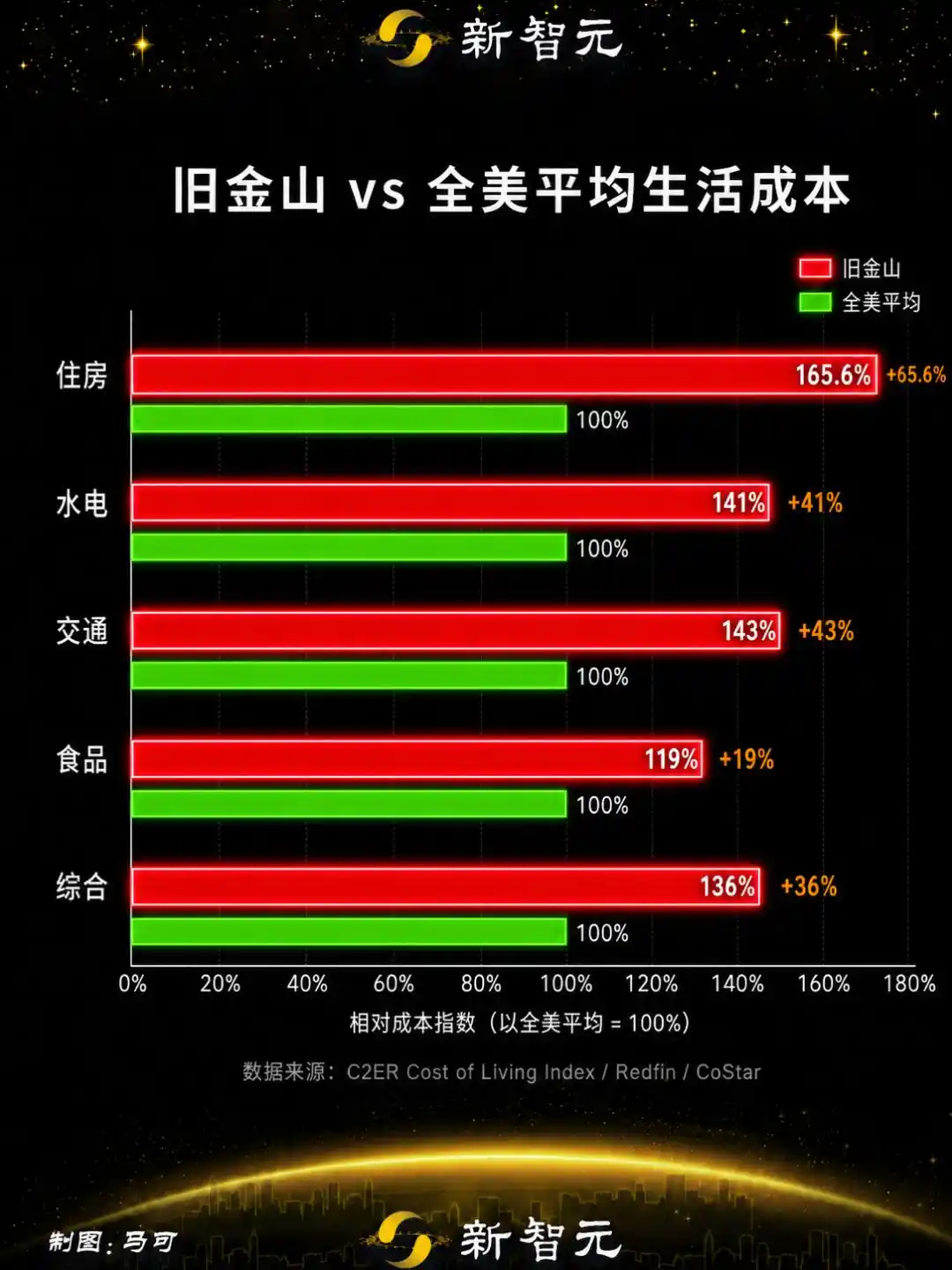

According to the Cost of Living Index released by the Council for Community and Economic Research (C2ER), San Francisco's overall cost of living is 65.6% higher than the national average.

Breaking it down: utilities are about 41% more expensive, transportation about 43% more, and groceries about 19% more.

These numbers themselves are abstract; the more tangible feeling comes from daily life.

Razniak says her monthly budget is about $1,000 higher than in previous years, yet her quality of life has hardly changed.

She describes this state as a low-grade, persistent money anxiety—not the urgency of living paycheck-to-paycheck, but far from the ease she thought this salary level should bring.

Earning Six Figures: Respectable but Strapped

Razniak's experience is not an isolated case.

Woodbury recently moved to Carnelian Bay on the shores of Lake Tahoe, where the cost of living is lower.

Look familiar? Lake Tahoe is the default wallpaper for macOS 26

Razniak stayed behind in an apartment in San Francisco's Haight-Ashbury neighborhood, sharing it with two roommates; she pays $1,650 monthly. They are maintaining a long-distance relationship.

A team leader earning $180,000 living in a shared apartment. This is hardly news in San Francisco anymore.

The squeezing effect of housing is accelerating.

In June, 25-year-old Varsha Madapoosi rented a four-bedroom, one-bathroom house in the Lower Pacific Heights neighborhood. She posted about two vacant rooms for rent in a private Facebook group, asking about $1,200 and $1,500 per month, respectively.

She attached a Google Form open for only 24 hours and received 88 applications.

In July of last year, a similar post in the same group received 28 responses over four days. Madapoosi says, "I have never seen this kind of reaction."

Jolie Gan, 23, moved to San Francisco in January, having just completed a Fulbright scholarship project at MIT.

She now works two jobs simultaneously: a role at the venture capital firm a16z and writing for a tech and science publication called Core Memory. Her combined annual salary is about $250,000, and she has no student loans.

It sounds like she should be doing well.

But she and her roommate moved three times in two months. Once because a so-called "two-bedroom" wasn't actually a two-bedroom, another time because the apartment had black mold and rodents.

Gan says that with a $250,000 income, she can hold on, even save for retirement.

But she sees friends earning under $200,000 whose incomes are being devoured almost entirely by rent, utilities, and food.

Razniak's feeling is more concrete—she once thought $200,000 was the dividing line, the number at which she could stop worrying about money.

Instead, she found that state of not thinking about money is simply unattainable in San Francisco.

She's not living paycheck-to-paycheck, nor is she in financial hardship. It's a state of being stuck in the middle, a low-grade vigilance about money she thought she had long left behind.

Stay or Go?

Gan chooses to stay.

Her reasons have little to do with salary—career opportunities, the city's energy, the social network she built over a few months.

"While the housing situation is truly absurd and indeed getting more expensive, I feel these intangible things are still worth it for me."

She plans to stay for at least a few more years.

Razniak and Woodbury have started looking at Seattle.

Razniak imagines a life there that she can't imagine affording in San Francisco, even though their combined income would be quite substantial in almost any other American city.

She says:

"We want a house, we want a garage, we want storage space. Here, it feels like those things are out of reach."

There's no right or wrong in these two choices.

But they point to the same reality: when an industry's wealth creation is fast enough to reshape a city's cost of living threshold, the very meaning of a "high salary" is being rewritten.

$180,000 is still a high income.

But in San Francisco, in 2026, on the eve of AI creating a new wave of billionaires, it doesn't buy a sense of security.

This isn't just San Francisco's story. Every wave of technology-driven wealth creation replays a similar squeeze in a number of cities.

The difference is that this time, the scale and speed of AI wealth creation far exceed any previous wave.

In a world where OpenAI employees have an average equity incentive of $1.5 million, a software engineer earning $180,000 has shifted from being a "winner" to one of the "squeezed out."

References:

https://www.nytimes.com/2026/06/29/technology/san-francisco-tech-salaries.html

This article is from the WeChat public account "新智元," author: ASI启示录